Best and Cheapest Homeowners Insurance in 2026

SEE FULL RANKINGS IN YOUR STATE

NATIONAL RANKINGS

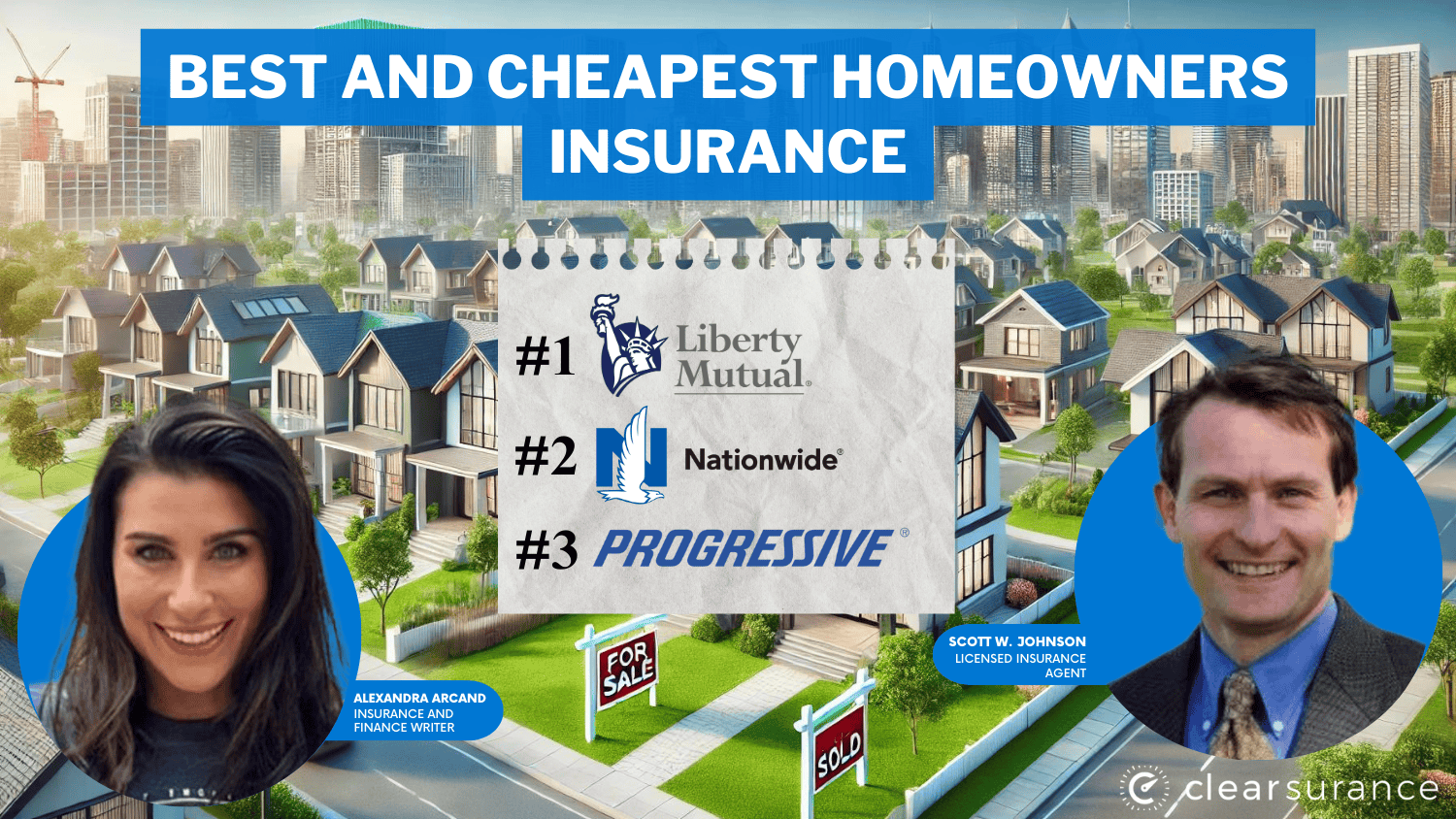

The top choices for the best and most affordable homeowners insurance are Liberty Mutual, Nationwide, and Progressive, with rates starting at $103 per month.

Liberty Mutual shines with its comprehensive coverage and competitive pricing. Nationwide provides a wide range of coverage options, while Progressive stands out for its flexible discounts.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 25% | A | Strong Reputation | Liberty Mutual | |

| #2 | 20% | A+ | Broad Coverage | Nationwide | |

| #3 | 10% | A+ | Flexible Discounts | Progressive | |

| #4 | 15% | A | Affordable Rates | Safeco | |

| #5 | 17% | B | Financial Stability | State Farm | |

| #6 | 25% | A+ | Comprehensive Protection | Allstate | |

| #7 | 20% | A | Reliable Service | Farmers | |

| #8 | 25% | A++ | Budget Friendly | Geico | |

| #9 | 13% | A++ | Excellent Benefits | Travelers | |

| #10 | 10% | A++ | Military Focused | USAA |

These companies provide affordable, reliable protection tailored to homeowners' needs. By comparing their rates and features, you can secure the best coverage at the lowest price for your home.

Find the cheapest home insurance today by entering your ZIP code above into our free comparison tool.

What You Should Know

- Find the best and cheapest homeowners insurance, starting at $103/month

- Liberty Mutual is the top provider, offering comprehensive coverage and competitive rates

- Compare these top providers to secure the best homeowners insurance rates for your needs

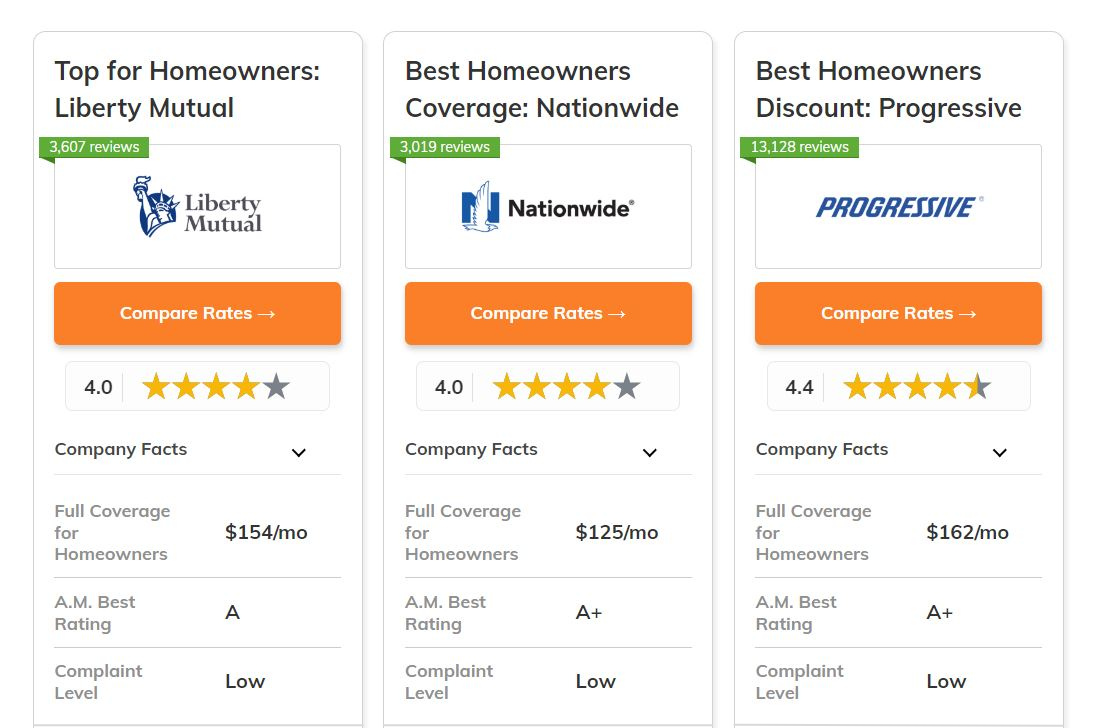

#1 – Liberty Mutual: Top Overall Pick

Pros

- Comprehensive Coverage: Liberty Mutual specializes in comprehensive homeowners insurance options that provide vital protection for your home.

- Low Monthly Prices: Liberty Mutual offers reasonable prices for homeowners insurance, beginning at $121/month. Read our Liberty Mutual review to learn more.

- Bundling Discounts: Liberty Mutual homeowners insurance provides a bundling discount of up to 25%, resulting in significant savings when paired with other products.

Cons

- Claim Response Time: Some customers have noted that the claims response time for Liberty Mutual homeowners insurance can be slower than competitors.

- Higher Premiums for High-Coverage Plans: Despite competitive minimum coverage rates, full-coverage policies may have higher premiums.

#2 – Nationwide: Best for Broad Coverage

Pros

- Broad Coverage Options: Nationwide offers a wide range of homeowners insurance coverage options that can be customized to meet specific needs.

- Cost-Effective Minimum Coverage Rates: Starting at $103 per month, Nationwide provides some of the most competitive rates for homeowners insurance coverage.

- Bundling Benefits: Nationwide offers a 20% discount for bundling homeowners insurance with other policies, which can lead to significant cost savings. For a comprehensive list, refer our Nationwide review.

Cons

- Limited Online Tools: Nationwide's homeowners insurance lacks specific advanced online tools for policy management compared to other insurance providers.

- Higher Deductibles: Some Nationwide homeowners insurance policies may come with higher deductibles, potentially impacting initial costs.

#3 – Progressive: Best for Flexible Discountsl

Pros

- Flexible Discounts: Progressive offers unique discount structures for homeowners insurance, providing flexibility for customers to save in multiple ways.

- Competitive Rates: Progressive homeowners insurance starts at $127/month, offering good value for cost-conscious homeowners.

- Discount on Bundles: Progressive offers a 10% discount on homeowners insurance when bundled with auto or other policies which covered in our Progressive review.

Cons

- Claims Satisfaction: Some customers have reported lower satisfaction with Progressive’s homeowners insurance claims handling process.

- Fewer Customization Options: Progressive’s homeowners insurance policies may lack the customization features found with other insurers.

#4 – Safeco: Best for Affordable Rates

Pros

- Affordable Rates: Safeco stands out for its affordable homeowners insurance rates, with starting rates as low as $108/month.

- Discounts on Bundling: Safeco homeowners insurance offers up to a 15% discount for bundling multiple policies, providing added savings.

- Good Basic Coverage: Safeco’s basic homeowners insurance coverage meets essential needs without inflated costs (Read more: Safeco Review).

Cons

- Limited Availability: Safeco homeowners insurance is not available in all states, restricting options for some customers.

- Lower Claim Satisfaction: Customers have reported mixed reviews on the claims handling experience with Safeco homeowners insurance.

#5 – State Farm: Best for Financial Stability

Pros

- Financial Stability: State Farm homeowners insurance is backed by strong financial stability, offering peace of mind to policyholders. Discover our State Farm review for a full list.

- Affordable Minimum Coverage: State Farm offers competitive rates starting at $113/month for minimum homeowners insurance coverage.

- Bundling Benefits: State Farm provides a bundling discount of 17% on homeowners insurance, allowing customers to save by combining policies.

Cons

- Limited Coverage Flexibility: State Farm homeowners insurance policies may not offer as much customization as competitors.

- Higher Rates for Full Coverage: While minimum coverage is affordable, State Farm’s full coverage homeowners insurance rates may be higher.

#6 – Allstate: Best for Comprehensive Protection

Pros

- Comprehensive Coverage: Allstate offers comprehensive homeowners insurance coverage, ensuring protection for various risks.

- Low Monthly Rates: Allstate homeowners insurance rates start at $133/month, balancing affordability with quality. Explore more in our Allstate review.

- Great Bundling Discounts: Allstate offers up to 25% discount when bundling homeowners insurance with auto or life insurance.

Cons

- High Premiums in Certain Areas: Allstate homeowners insurance rates may be higher for homes in disaster-prone areas.

- Mixed Claim Experiences: Some customers need more claims satisfaction with Allstate homeowners insurance.

#7 – Farmers: Best for Reliable Service

Pros

- Excellent Customer Support: Farmers is well-known for outstanding home insurance customer service.

- Competitive Starting Rates: Farmers offers house insurance for $122 per month, making it affordable to many. For more information, see our Farmers review.

- Discounts for Bundling: Policyholders can save 20% on house insurance by bundling plans with Farmers.

Cons

- Limited Options: Some clients may notice that Farmers has fewer house insurance options than competing companies.

- Higher Custom Coverage Costs: Farmers' personalized home insurance plans may have higher premiums than those offered by competing insurers.

#8 – Geico: Best for Budget-Friendly

Pros

- Affordable Minimum Coverage: Geico offers budget-friendly homeowners insurance rates, starting at $109/month.

- Bundling Benefits: With up to 25% savings, Geico homeowners insurance provides substantial discounts when bundled with other policies (Learn more: 32 Genius Ways to Save Money).

- Easy-to-Use Online Tools: Geico excels in offering user-friendly online tools for homeowners insurance policy management.

Cons

- Limited Customer Support: Geico homeowners insurance may offer limited customer service options for complex claims.

- Not as Customizable: Geico’s homeowners insurance policies may not offer as much customization as some competitors.

#9 – Travelers: Best for Excellent Benefits

Pros

- Comprehensive Benefits: Travelers homeowners insurance offers a wide range of benefits to meet a variety of coverage needs.

- Competitive Minimum Rates: Travelers' homeowner's insurance starts at $120 per month, making it affordable for a wide spectrum of homeowners. Check out our Travelers review.

- Savings Through Bundling: Travelers provides a 13% discount when clients bundle homeowners insurance with other policies, allowing them to save money.

Cons

- Limited Discount Options: Travelers' homeowners insurance may provide fewer discount options than other companies.

- Potential Premium Hikes: Some Travelers homeowners insurance consumers have reported incremental hikes in their premiums.

#10 – USAA: Best for Military-Focused

Pros

- Tailored for Military Families: USAA homeowners insurance is tailored specifically for military members and their families, offering unique benefits.

- Low Minimum Coverage Rates: USAA provides competitive homeowners insurance rates starting at $104/month. Delve into our USAA review.

- Strong Financial Backing: USAA is backed by strong financial stability, ensuring reliability for homeowners insurance.

Cons

- Restricted Eligibility: USAA homeowners insurance is only available to military members and their families.

- Limited Coverage for Non-Military: Non-military customers cannot access USAA’s homeowners insurance benefits.

Understanding the Best Homeowners Insurance Rates for a $200K Home

When searching for the best homeowners insurance company—and aiming to avoid less favorable options—it's essential to find one that offers the best homeowners insurance rates. While many factors influence the cost of a policy, we can't predict the exact rates you'll pay without a formal quote. Below is a comparison of monthly rates for both minimum and full coverage to help guide your decision:

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $133 | $170 | |

| $122 | $150 | |

| $109 | $145 | |

| $121 | $154 | |

| $103 | $125 | |

| $127 | $162 | |

| $108 | $135 | |

| $113 | $140 | |

| $120 | $148 | |

| $104 | $130 |

However, we have provided the average homeowners insurance rates for a $200K home from seven of the largest companies in the United States. Nationwide has the best homeowners insurance rates, on average for a $200,000 home, out of a group of eight of the largest home insurance companies in the country.

Monthly home insurance from Nationwide costs an average of $82 per month, followed by Allstate at $91 per month. This is for $200,000 in dwelling coverage to rebuild your home in the event of a total loss. Refer to the table below for the monthly rates on a $200,000 home from seven different companies.

| Rank | Company | Rates |

|---|---|---|

| #1 | $82 | |

| #2 | $91 | |

| #3 | $98 | |

| #4 | $99 | |

| #5 | $102 | |

| #6 | $125 | |

| #7 | $135 |

The rates for each of these companies are based on a $200,000 dwelling with the following coverage limits: $100,000 personal property, $20,000 loss of use, $20,000 other structures, $300,000 liability and $5,000 medical. The policy has a $1,000 deductible.

The house used for the profile was constructed in 2004 and the individual had a good insurance score. The rates displayed should only be used for comparative purposes as individual rates will differ. Rate data is provided by Quadrant Information Services.

Browse for full details in our guide "How Home Improvement Projects Affects Your Insurance."

Best Homeowners Insurance Rates for a $400K Home

Homeowners insurance rates depend heavily on the value of your home. As you'll see in the table below, the average homeowners insurance rates for a $400K home are significantly higher than the average rates for a $200K home. The replacement costs have doubled for dwelling coverage, and the common threats remain about the same.

For a $400,000 home, State Farm offers the best homeowners insurance rates on average at $1,864 per year. USAA, Nationwide and Allstate all have similar national average homeowners insurance rates. Of course, insurance costs for the same house can vary widely based on your state and zip code. Your annual premium may also change if you've filed a recent claim. See the table below for monthly rates for a $400K home across seven companies.

| Rank | Company | Rates |

|---|---|---|

| #1 | $155 | |

| #2 | $156 | |

| #3 | $157 | |

| #4 | $161 | |

| #5 | $176 | |

| #6 | $190 | |

| #7 | $242 |

The rates for each of these companies are based on a $400,000 dwelling with the following coverage limits: $200,000 personal property, $40,000 loss of use, $40,000 other structures, $300,000 liability and $5,000 medical. The policy has a $1,000 deductible. The house used for the profile was constructed in 2004 and the individual had a good insurance score. The rates displayed should only be used for comparative purposes as individual rates will differ. Rate data is provided by Quadrant Information Services.

The Cost of Homeowners Insurance

The cost of homeowners insurance depends on many factors including where you live, your claims history, and how much your home is worth. In the table below, we’ve listed average homeowners insurance rates in all 50 states and Washington, D.C., for a $200,000 home and a $400,000 home. Of course, rates can vary even within the same city or state. so t

While these average homeowners insurance rates can provide a helpful baseline, home insurance rates can vary significantly depending on where you live in the state and which company you purchase insurance from. Dive into our guide "5 Things to Know About Home Insurance."

Take a $200,000 home in Florida, for instance. A home along the coast is likely going to cost significantly more to insure than a home in the center of the state because of the higher risk of hurricanes and damage along the coast. The table below shows the respective monthly rates for $200,000 and $400,000 coverage amounts, providing a clearer comparison of insurance costs.

| State | $200,000 | $400,000 |

|---|---|---|

| Alabama | $126 | $243 |

| Alaska | $72 | $127 |

| Arizona | $90 | $140 |

| Arkansas | $152 | $237 |

| California | $57 | $105 |

| Colorado | $180 | $278 |

| Connecticut | $92 | $166 |

| Delaware | $55 | $99 |

| Florida | $120 | $244 |

| Georgia | $99 | $160 |

These rates are an average of the five largest homeowners insurance companies in the state and they will vary based on the coverages you have, where you live in the state and other factors. Given how much rates can vary by person, it’s always important to get formal quotes. Rate data is provided by Quadrant Information Services.

Claim Service of Homeowners Insurance Companies

While we all hope to never need to file a homeowners insurance claim, in the event you do, you want peace of mind that it'll be handled efficiently and properly. But without having had a claim with a company before, how can you know which are best at servicing claims? That's where our reviews and ratings can help.

The table below shows the compiled homeowners claims ratings and monthly rates for the top 10 companies with at least 100 reviews from homeowners who have filed a claim with the company.

| Company | Rating | Rates |

|---|---|---|

| 4.71 | 326 | |

| 4.36 | 112 | |

| 4.25 | 152 | |

| 4.2 | 1006 | |

| 4.17 | 220 | |

| 4.15 | 180 | |

| 4.03 | 126 | |

| 4.01 | 213 | |

| 4.01 | 188 | |

| 3.99 | 675 |

Among these companies, USAA has the highest claims service rating at 4.71 out of 5, followed by Erie Insurance with a rating of 4.36 out of 5.

Best Homeowners Insurance Coverage

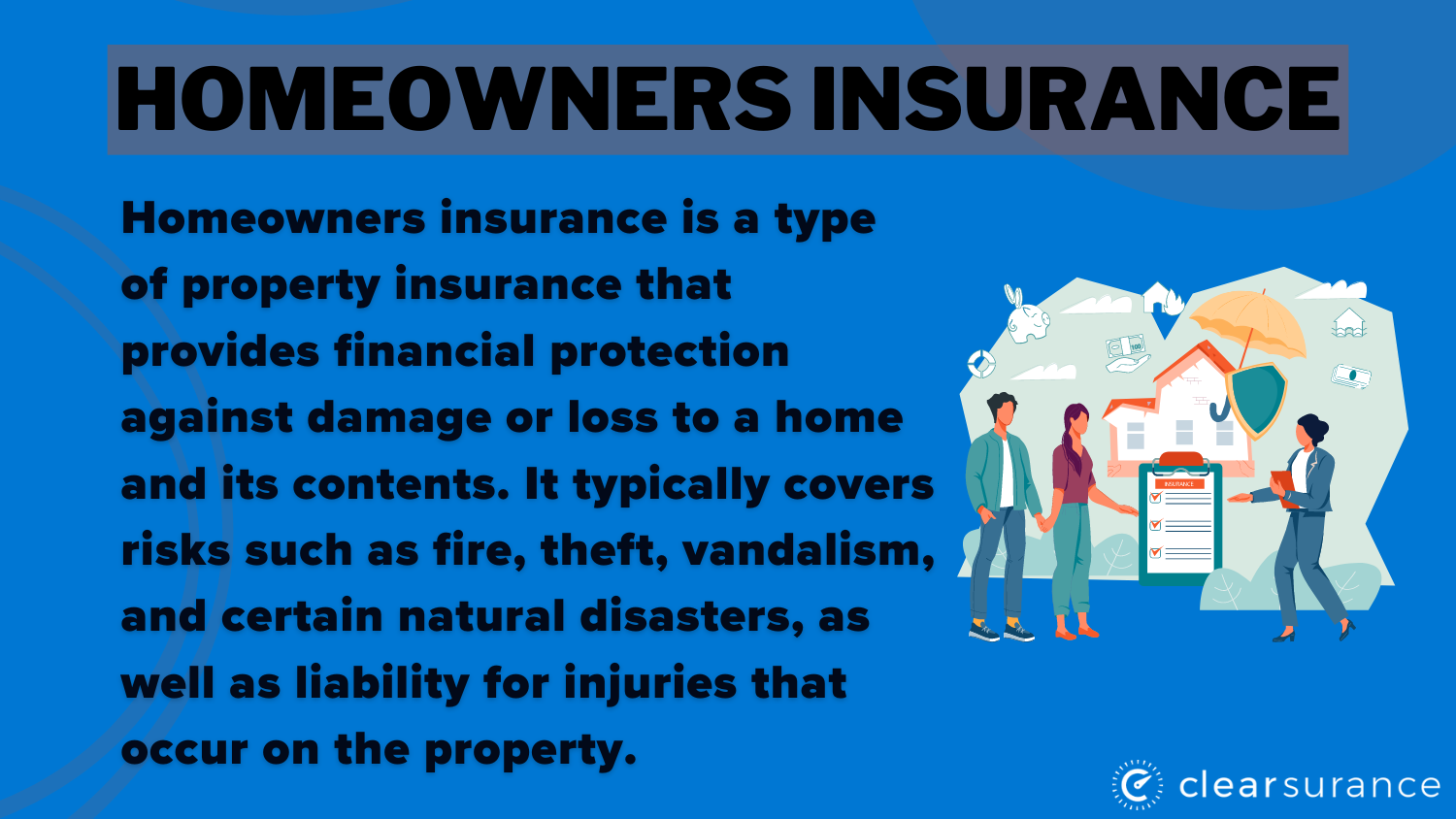

Homeowners insurance generally covers your dwelling, your personal property, other structures on your personal property and liability. Additionally, a standard homeowners insurance policy also often offers protection for loss of use and medical payments to others.

What your homeowners insurance policy covers can vary by state, company, and the type of policy you choose, making it difficult to generalize. However, most standard homeowners insurance policies typically cover 16 perils, including theft, fire, lightning, hail, windstorms, and vandalism. Other common perils include damage from aircraft or vehicles, smoke, explosions, falling objects, and volcanic eruptions.

Coverage also extends to damage from water or steam leaks, the weight of ice or snow, freezing of systems, and electrical surges. It's essential to discuss your specific coverage needs with an insurance company or agent to find the right policy for you.

You can also read about the differences between an HO-3 insurance policy and an HO-5 insurance policy. An HO-5 policy offers additional protection, but at an added cost.

The Best Homeowners Insurance That Isn't Covered

Homeowners insurance policies don't cover all perils. Home insurance typically does not cover flood damage caused by weather-related flooding. What does this mean? If your town experiences flooding during a severe storm and your basement ends up with a few inches of water and your washer and dryer are destroyed, a standard homeowners insurance policy likely won't cover that damage.

However, some water damage is covered by home insurance. For example, if a pipe bursts in your basement and destroys your washer and dryer, your homeowners policy likely will cover that as it's a named peril. Delve into our guide "Does Homeowners Insurance Cover Roof Damage?"

So outside of flood damage, what else does homeowners insurance not cover? Homeowners insurance also usually doesn't cover earthquakes, damage from neglect, power failures, sinkholes, bed bugs, termites, mold (in some cases) and war.

How can you get protection from these events? In some cases, you can purchase an additional policy to protect you from these disasters. You can buy flood insurance or earthquake insurance to cover from the disasters that aren't usually covered by homeowners insurance.

The Most Popular Homeowners Insurance Companies

State Farm is the most popular home insurance company choice among homeowners, with more than 18 percent of homeowners around the country having a policy with State Farm. Allstate and Liberty Mutual rank second and third in most popular. Below is a look at the 10 largest homeowners insurance companies in the U.S. by market share.

Remember, a large market share doesn't guarantee the best service or price. Consider all factors when choosing your homeowners insurance. Here's the table showing the market share of the top providers.

| Company | Market Share |

|---|---|

| 18.6% | |

| 8.4% | |

| 6.9% | |

| 6.0% | |

| 6.0% | |

| 3.8% | |

| 3.5% | |

| 3.2% | |

| 2.9% | |

| 1.7% |

The insurance marketplace share percentages include all companies that are owned by the group. For example, Safeco Insurance is owned by Liberty Mutual, meaning some of the 6.9 percent of market share is business done under the brand Safeco.

Additionally, Encompass Insurance and Esurance are owned by Allstate, though these companies make up a very small percentage of Allstate's total market share. Foremost is owned by Farmers Insurance. Allied and others are owned by Nationwide. Homesite is owned by American Family.

Tips to Get the Best Home Insurance

There’s no sense in paying more money on your homeowners insurance than you need to, right? So what are the top ways to lower your homeowners insurance rates with one of the best homeowners insurance companies?

Here’s a list of the top five ways you can lower your homeowners insurance rates:

- Bundle your homeowners insurance with other types of coverage insurance products, such as an auto insurance policy. Auto policies are probably the most-often bundled with homeowners insurance policies, but some insurers have other options, such as life insurance.

- Raise your homeowners insurance deductible

- Consider changing your level of coverage

- Install home safety features to your house

- If you’ve been claim-free, shop for a good deal

Speaking of shopping for a good deal, it's important to obtain insurance quotes from multiple companies. While the rates we listed above for your state and some companies provide a range of what you should be expecting, everyone has different rates. In order to get the best deal on your homeowners insurance, it pays to shop around.

How Homeowners Insurance Rates are Calculated

Ever wonder why you pay what you do for home insurance? While factors like the age of your home may be obvious, others are less apparent. Homeowners insurance companies consider things such as the required coverage, mortgage size, credit score (in some states), home size, location, condition, proximity to a fire station, claims history, deductible amount, and optional add-ons like umbrella insurance.

Zillow estimates homeowners pay about $35 per month for every $100,000 of their home’s value. Before choosing a policy, ask about exclusions, and make sure you're covered for risks like flooding or earthquakes if applicable.

With home prices rising, securing cheap home insurance coverage is important. Get started today by entering your ZIP code into our free quote tool below.

How homeowners insurance rates are calculated

Ever wonder why you pay what you do to insure your home? Some things may be obvious, like the age of your home. But other factors that contribute to the price of homeowners insurance may not be as obvious. Here’s a list of some of the things homeowners insurance companies consider when quoting you a rate:

- The level of coverage required

- The size of your mortgage

- Your credit score (in some states)

- The square footage of your home

- The geographic location of your home

- The condition of your home

- The age of your home

- The proximity of your home to a fire station

- Your previous claims record

- The amount of your deductible

- Optional add-ons like umbrella insurance

Zillow estimates that homeowners can expect to pay approximately $35 each month for every $100,000 of your home's value. The national average price of homeowners insurance in 2015 was $1,173, according to the Insurance Information Institute, but keep in mind it can vary significantly by state and coverage needs.

How to save money on your homeowners insurance

There’s no sense in paying more money on your homeowners insurance than you need to, right? So what are the top ways to save on your homeowners insurance rates?

Here’s a list of the top five ways you can lower your homeowners insurance rates:

- Bundle your homeowners insurance with other policies

- Raise your homeowners insurance deductible

- Consider changing your level of coverage

- Install home safety features to your house

- If you’ve been claim free, shop for a good deal

How we rank homeowners insurance companies

Wondering how Clearsurance determines scores for insurance companies? Our algorithm analyzes a range of inputs from our community of unbiased insurance customers, including:

- Cost

- Customer Service

- Overall Experience

- Claim service

- Purchasing experience

- Likelihood to recommend

Guide to understanding homeowners insurance

Your home is likely your most valuable asset, making it that much more important that you insure your home with a top-rated homeowners insurance company. But beyond just picking a company, it’s crucial to have the right coverage and to understand that coverage. Did you know that a standard homeowners insurance policy has six types of coverage? And did you know that there are usually 16 types of perils found in a homeowners insurance policy?

At Clearsurance, we want to make sure you have a strong understanding of your homeowners insurance coverage and what it all means. Check out our practical guide to understanding homeowners insurance to become a smarter insurance customer. And for more educational content on other homeowners insurance topics, check out our blog!

Frequently Asked Questions

What are the best and cheapest homeowners insurance companies?

The top three are Liberty Mutual, Nationwide, and Progressive, offering affordable rates and comprehensive coverage.

How much does the best homeowners insurance cost?

Rates start as low as $103/month for minimum coverage, depending on the provider and location. Make sure your home is protected by entering your ZIP code into our home insurance comparison tool below today.

What factors influence homeowners insurance rates?

Rates are determined by factors such as home value, location, coverage options, and individual risk profiles.

Can I bundle homeowners insurance with other types of insurance?

Yes, many companies offer bundling discounts when combining homeowners insurance with auto or other types of coverage. Check out our guide "Save Money on Homeowners Insurance & Prevent Claims."

What discounts are available for homeowners insurance?

Discounts are available for bundling policies, home safety improvements, and claim-free histories, among others.

Is comprehensive homeowners insurance worth the extra cost?

Comprehensive coverage provides more protection, which is beneficial if you want additional security for your home and belongings.

How can I compare homeowners insurance quotes?

You can compare quotes online by providing basic details about your home, coverage needs, and location to get personalized estimates.

What does full coverage homeowners insurance include?

Full coverage typically includes protection for the home, personal belongings, liability, and additional living expenses if the home is uninhabitable.

Browse for more details in our guide "Liability vs. Full Coverage: Car Insurance Explained."

Are homeowners insurance rates the same across all states?

No, rates vary by state due to differences in risk factors like weather, crime rates, and state regulations.

How do I choose the best homeowners insurance company?

Evaluate companies based on their coverage options, rates, customer service reviews, and available discounts to find the best fit for your needs.