Best Tennessee SR-22 Insurance in 2026 (Your Guide to the Top 10 Companies)

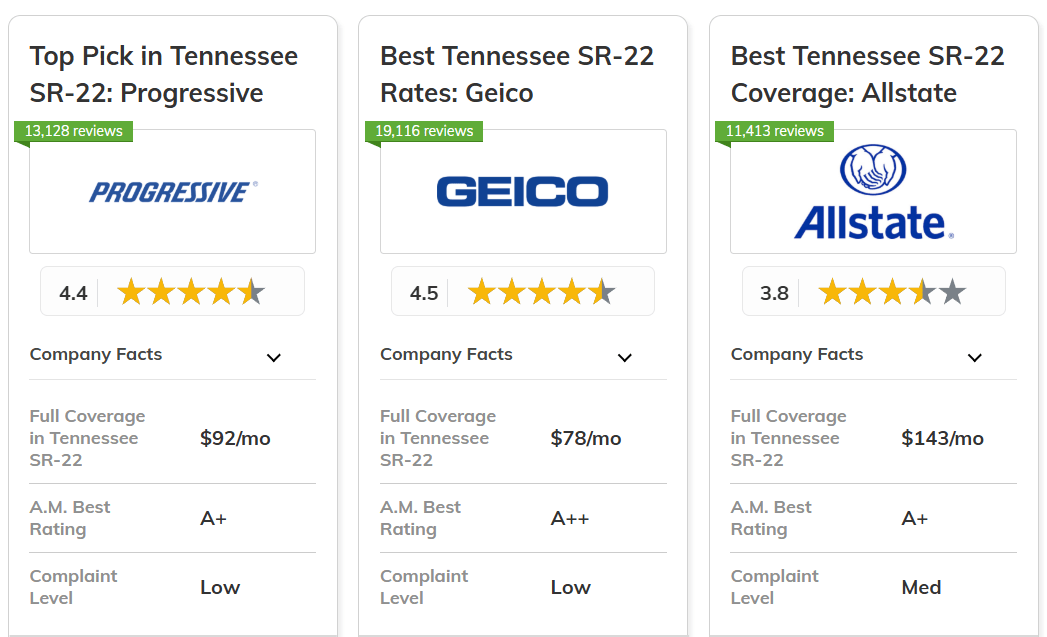

The best Tennessee SR-22 insurance providers are Progressive, Geico, and Allstate, offering tailored benefits for high-risk drivers with rates starting at $18.

Progressive is best for reliable SR-22 filing and many coverage choices. Geico offers good value with low prices and a simple claims process. Allstate stands out because it has flexible policies, letting drivers customize their SR-22 insurance in Tennessee.

| Company | Rank | UBI Savings | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 30% | A+ | Flexible Pricing | Progressive | |

| #2 | 25% | A++ | Competitive Rates | Geico | |

| #3 | 40% | A+ | Comprehensive Coverage | Allstate | |

| #4 | 30% | B | Nationwide Accessibility | State Farm | |

| #5 | 40% | A+ | Strong Reputation | Nationwide | |

| #6 | 20% | A | Personalized Service | American Family | |

| #7 | 15% | A | Customizable Plans | Farmers | |

| #8 | 30% | A | Tailored Options | Liberty Mutual | |

| #9 | 20% | A++ | Extensive Network | Travelers | |

| #10 | 30% | A++ | Military Focused | USAA |

These providers make handling SR-22 requirements simpler and ensure your coverage meets Tennessee’s rules.

Wondering if another provider has lower rates? Find out by entering your ZIP code into our free quote comparison tool.

What You Should Know

- Progressive leads with reliable SR-22 filing in Tennessee

- Tennessee SR-22 insurance meets high-risk drivers' specific needs

- SR-22 options ensure coverage aligns with Tennessee’s standards

#1 – Progressive: Top Overall Pick

Pros

- Affordable Plans: Progressive keeps Tennessee SR-22 insurance costs low, perfect for budget-conscious drivers.

- Flexible Coverage: Lots of add-ons to customize SR-22 for Tennessee’s needs.

- Good Driver Discounts: Based on our Progressive review you can earn up to 30% off with safe driving on Tennessee SR-22 policies.

Cons

- Rates Vary: Prices can shift depending on personal factors for SR-22 in Tennessee.

- Limited Discounts: Not all savings options apply to Tennessee SR-22 coverage.

#2 – Geico: Best for Competitive Rates

Pros

- Low SR-22 Rates: Geico’s Tennessee SR-22 insurance is budget-friendly, especially for high-risk drivers.

- Driver Savings: Earn up to 25% off with Geico’s telematics program for Tennessee SR-22.

- Top Financial Rating: Geico’s A++ rating means solid financial backing for SR-22 coverage.

Cons

- Fewer Custom Options: SR-22 plans in Tennessee might not be as customizable.

- Savings Potential: Tennessee SR-22 may not be eligible for all reductions. Find out tips we learned after filing a car insurance claim.

#3 – Allstate: Best for Comprehensive Coverage

Pros

- Wide SR-22 Options: Allstate’s Tennessee SR-22 plans cover a range of needs for high-risk drivers.

- Accident Forgiveness: Helps SR-22 drivers in Tennessee avoid rate increases after one accident.

- High UBI Discounts: Save up to 40% on SR-22 coverage with safe driving in Tennessee. See details in our Allstate review.

Cons

- Higher Premiums: SR-22 rates in Tennessee can be pricey, even with discounts.

- Forgiveness Limits: Accident forgiveness may not apply to every SR-22 driver in Tennessee.

#4 – State Farm: Best for Nationwide Accessibility

Pros

- Widely Available: If you drive a lot and need auto insurance, you may get State Farm's SR-22 policy anywhere in the United States.

- Reasonable Rates: According to our State Farm review, the company provides SR-22 insurance at a low price for drivers in Tennessee.

- Dependable Service Provider: Renown for trustworthiness in SR-22 support and service.

Cons

- Rate Restrictions: Fewer discount options compared to other states for SR-22.

- Lower Rating: B rating may not be good for some SR-22 Tennessee policyholders.

#5 – Nationwide: Best for Strong Reputation

Pros

- Solid Financial Standing: Nationwide’s A+ rating brings stability to Tennessee SR-22 policies.

- Wide Coverage Options: Tennessee SR-22 plans meet a range of needs. Discover insights in our Nationwide review.

- Big Driver Savings: Safe drivers in Tennessee can save up to 40% on SR-22 insurance.

Cons

- Higher SR-22 Costs: SR-22 policies in Tennessee can be a bit more expensive.

- Claims Process: SR-22 claims might involve extra paperwork.

#6 – American Family: Best for Personalized Service

Pros

- Custom Policies: American Family lets you tweak your Tennessee SR-22 coverage to fit your needs.

- Great Customer Service: Personalized support for Tennessee SR-22, especially helpful for unique situations.

- A Rating: Financially secure with an A rating for Tennessee SR-22 plans. Delve into our American Family review for more info.

Cons

- Discounts Limited: Tennessee SR-22 coverage has fewer savings options.

- Not Available Everywhere: SR-22 coverage may not be accessible in all Tennessee areas.

#7 – Farmers: Best for Customizable Plans

Pros

- Highly Customizable: Farmers’ Tennessee SR-22 policies can be tailored to fit personal needs.

- Reliable Financials: With an A rating, Farmers provides trusted SR-22 support. View our Farmers review to learn more.

- Telematics Discounts: Safe drivers in Tennessee can save up to 15% on SR-22 plans.

Cons

- Higher SR-22 Rates: SR-22 insurance in Tennessee might be a bit pricier.

- Limited Locations: Fewer spots in Tennessee for in-person SR-22 help.

#8 – Liberty Mutual: Best for Tailored Options

Pros

- Adjustable Coverage: Liberty Mutual’s Tennessee SR-22 insurance can be shaped to match different risk levels.

- Driver Discounts: Safe drivers in Tennessee can save up to 30% on SR-22 policies.

- A Rating: Financially secure for Tennessee SR-22 needs. Discover our Liberty Mutual review for additional information.

Cons

- Rates Can Vary: SR-22 costs fluctuate based on risk factors in Tennessee.

- Fewer Local Agents: In-person SR-22 help might be sparse in some Tennessee areas.

#9 – Travelers: Best for Extensive Network

Pros

- Nationwide Access: Travelers’ Tennessee SR-22 insurance is widely available across the country, great for multi-state needs.

- Top A++ Rating: Financially solid SR-22 insurance you can rely on. Discover more about offerings in our Travelers review.

- Driver Savings: Tennessee SR-22 drivers can save up to 20% with safe driving.

Cons

- Higher Costs: SR-22 rates in Tennessee can be a bit steeper than average.

- Fewer Custom Options: SR-22 policies may not be as tailored to Tennessee.

#10 – USAA: Best for Military Focused

Pros

- Military Benefits: USAA’s Tennessee SR-22 insurance is specifically for military families.

- High Rating: A++ rating provides reliable coverage for Tennessee SR-22. Access comprehensive insights into our USAA review.

- Affordable Rates: Competitive rates for Tennessee SR-22 insurance for military members.

Cons

- Military-Only Access: Only available to military-affiliated families needing Tennessee SR-22.

- Limited Discounts: Fewer SR-22 discounts compared to non-military providers.

Comparing SR-22 Coverage Rates Across Tennessee Providers

The monthly cost of SR-22 insurance in Tennessee might vary greatly depending on your chosen company. Therefore, awareness of the possibilities for primary and complete coverage is beneficial. Comparing prices in this manner will help you find the most excellent offer that suits your needs and price range.

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $45 | $143 | |

| $32 | $102 | |

| $26 | $86 | |

| $24 | $78 | |

| $33 | $184 | |

| $37 | $118 | |

| $29 | $92 | |

| $22 | $72 | |

| $27 | $88 | |

| $18 | $58 |

State Farm and USAA offer some of the lowest monthly rates, with minimum coverage starting as low as $22 and $18, while USAA also has a great deal on full coverage at just $58. Geico, Farmers, and Progressive also keep things affordable for Tennessee drivers needing SR-22 coverage.

| Insurance Company | Available Discount |

|---|---|

| Loyalty, Early Bird, Defensive Driving | |

| Homeowner, Safe Driver, Good Student | |

| Multi-vehicle, Defensive Driving, Good Student | |

| Military, Anti-theft, Multi-policy | |

| Multi-policy, Paperless Billing, SmartRide | |

| Multi-policy, Safe Driver, Pay-in-Full | |

| Accident-Free, Good Driver, Vehicle Safety | |

| Hybrid Vehicle, Continuous Insurance, New Car | |

| Military Service, Safe Driver, Loyalty | |

| Military Service, Safe Driver,Loyalty, Early Bird |

State Farm and USAA have meager monthly rates, with comprehensive insurance coverage costing as little as $22 from State Farm and $18 from USAA. USAA also offers a great rate at just $58 for full coverage. Other companies like Geico, Farmers, and Progressive also provide reasonable prices for Tennessee drivers who need SR-22 insurance.

Tennessee Drivers and SR-22 Filing Needs

If you need to file an SR-22 form in Tennessee, it means you’ve committed a driving violation and have been required by the state or court to file it. The SR-22 form confirms you meet Tennessee's minimum insurance requirements, allowing you to drive legally. Knowing the best insurance options in Tennessee is key.

You’ve likely heard the term SR-22 insurance if you’re required to file an SR22 in Tennessee. While SR-22 insurance isn't a specific variant of auto insurance coverage, it does affect what you'll pay and what type of coverage you'll need. It becomes your financial responsibility to file an SR-22 and maintain the level of coverage required.

You'll need to know your minimum limits, as the SR-22 serves as proof that you've met your state’s requirements. In Tennessee, SR-22 insurance after a DUI conviction costs an average of 89% more than car insurance for standard drivers. Needing SR-22 insurance means you are a high-risk or non-standard driver.

In Tennessee, SR-22 insurance is required for a period of three to five years. Throughout this time, you must maintain your auto policy without any lapse in coverage. Your car insurance rates will be increased throughout the duration of your SR-22 filing period.

If you maintain your SR-22 insurance for your required filing period and keep a clean driving record, you won’t need to file the form any longer after your period is up. This could result in your coverage and car insurance rates decreasing, depending on your violation. DUIs may stay on your record for much longer.

With a license suspension due to your conviction, you’ll need SR-22 insurance in order to get your license reinstated after your suspension period is complete.

If your SR-22 insurance policy is canceled at any point, by you or your car insurance company, or if you have a lapse in coverage during your filing period, your Tennessee driver’s license may be suspended.

When you're putting together the list of things you need to be aware of, such as your minimum coverage requirements and what average cost you're able to spend, you may discover your current policy isn't doing you any favors. If you need to compare insurance companies, we offer an online, free tool that can help you.

Tennessee SR-22 Minimum Insurance Requirements

There's generally some amount of financial responsibility that comes with having an SR-22 on your record. Your insurance costs will increase, but you will also need to follow the minimum requirements as well. If you’re required to have SR-22 insurance in Tennessee, you’ll be required to have at least the following coverage:

- $25,000 for Bodily Injury or Death per Person

- $50,000 for Bodily Injury or Death per Accident

- $15,000 for Property Damage Coverage per Accident

Naturally, with auto insurance policies from the best car insurance companies, there are more coverage options available, but these represent the required SR-22 amount.

Understanding SR-22 Eligibility in Tennessee

In Tennessee, SR-22 insurance is required in a few scenarios in order for you to get your license reinstated. SR-22s are required after you’ve committed certain violations with the law. You may even be required to have an SR-22 if you’ve had a series of small violations within a short span of time. You could need SR-22 insurance for the following reasons:

- Conviction for Driving Under the Influence (DUI or DWI)

- Driving Without Car Insurance

- Driving With a Revoked or Suspended License

- Numerous At-Fault Accidents

- Reckless or Dangerous Driving

Some of these may result in jail time, which most people want to avoid at all cost. If your license was suspended and you’re required to have SR-22 insurance in Tennessee because of your accident history or any other one of these violations, you must file an SR-22 after your suspension period is over in order to drive.

SR-22 Insurance Rates Overview in Tennessee

SR-22 insurance increases rates because insurers think these drivers are high-risk. The cost is different for each company and state. Many things affect how much SR-22 insurance costs, like your age, whether you are male or female, where you live, your credit score, what kind of car you drive, whether you are married or not, and more factors. Knowing how to buy car insurance effectively can help you navigate these costs.

When drivers are convicted of DUI, they often need SR-22 insurance. In Tennessee, the average cost for car insurance after one DUI is around $160 each month. This amount is 89% higher than what drivers with no violations usually pay. The cost is different with each insurance company. Below is a table showing the average rates for drivers in Tennessee who have a DUI from major providers.

| Insurance Company | Monthly Rates |

|---|---|

| $75 | |

| $96 | |

| $99 | |

| $110 | |

| $116 | |

| $131 | |

| $150 | |

| $158 | |

| $173 | |

| $179 | |

| $216 | |

| $230 | |

| $384 |

These prices are for a 35-year-old single person driving a 2015 Toyota Highlander LE with full coverage (100/300/50 limits), a $500 deductible, and one DUI on their record. The rates shown here should only be used to compare; personal high-risk insurance costs in Tennessee will vary. Rate data is provided by Quadrant Information Services.

Even though SR-22 insurance policies cost a lot, if you keep up with your car insurance and keep the SR-22 form for the whole required time without any driving issues, your costs might eventually reduce.

Steps to Obtain SR-22 Insurance in Tennessee

You must contact your auto insurance provider in Tennessee to obtain SR-22 coverage. There is no way to get an SR-22 on your own; the state of Tennessee's Department of Commerce and Insurance has to approve insurance providers to do so. You can have your insurance provider submit it if they provide SR-22 coverage; if you still need to find another insurer that does.

Even if your company provides SR-22 insurance, it’s worth exploring options for the best car insurance in Tennessee. Because SR-22 insurance significantly affects your rates in Tennessee, and costs vary by provider, comparing rates may help you find a better deal.

Do you look for Tennessee SR-22 insurance companies with at least 25 reviews? To find the top-rated ones, you just sort by rating. After determining which businesses have received the highest customer ratings, you can use other people's experiences to inform your judgments. Companies can be viewed, and you can choose which ones you want estimates from.

To see what customers say about the company, click on its name in the table. This will take you to the company's profile page, where you can find more information and reviews from other people.

Alternative Options to SR-22 Insurance in Tennessee

If you don’t want to get SR-22 insurance in Tennessee, the alternative option is to wait out the three to five year filing period. This involves surrendering your driving privileges for the entire period to avoid the need for SR-22 insurance or the ability to file a car insurance claim.

This means that you need to weigh having SR-22 coverage against not being able to drive.

SR-22 Filing Fees in Tennessee

You may need to pay a fee to file the SR-22 in Tennessee to reinstate car insurance for drivers with a suspended license. If that’s the case, you’ll have to pay a reinstatement fee. The fee can be paid online, by mail or in person at select Reinstatement Centers. If you owe more than $200 in reinstatement fees, you may be eligible for a payment installment plan.

If you’re convicted of a DUI, your license will be suspended for one year if it’s your first offense, and much longer if you’re a repeat offender. According to the Tennessee Department of Safety and Homeland Security (DOS), a single DUI conviction can cost you $5,000 or more for fees and fines.

Factors Influencing Car Insurance Rates

Comparing car insurance quotes can be frustrating, especially when trying to understand rate calculations and ways to get cheap car insurance. While there's no set formula, many factors affect your car insurance rate. Among the factors that car insurers consider are:

- Your Driving Record

- How Much You Drive

- Location

- Age

- Gender

One of the biggest misunderstandings about insurance rates is thinking that only your driving history matters. The accident history of drivers in your area also affects how much you pay. For example, even if you have not had any accidents for two years, your insurance costs could still increase if there have been many accidents nearby lately. Why is that the case?

Insurance companies spread risk across all policyholders to ensure funds are available for claims, unlike when only drivers with accidents face rate hikes. Drivers with expensive claims may struggle with rate hikes based on payouts alone, so insurers slightly increase rates for all, with higher raises for at-fault drivers.

Determining the Right Amount of Car Insurance

You do not want to be underinsured or without insurance when you face a claim after a car accident or other damage to your vehicle. At the same time, paying for more coverage than necessary makes no sense. So, the issue is raised: How much coverage do you need for your auto insurance?

Even while it may be annoying, the answer is that it depends. For instance, a new leased car typically requires collision, comprehensive, and bodily injury liability coverage, while an older, low-value car may not. Additionally, 12 no-fault states mandate personal injury protection (PIP) for drivers.

So, when deciding what car insurance coverage and limits to buy, you must research. It would help if you spoke with an insurance agent or contacted your insurance company to understand the best choices for your situation.

Tips to Maximize Car Insurance Savings

We all want the best coverage at a reasonable cost. You can reduce your auto insurance rate in a few ways but always strive for quality to save a little money.

Here are five ways you may be able to lower your car insurance rates:

- Bundle Your Car Insurance With Other Policies

- Consider Raising Your Deductibles

- Pay Your Car Insurance Policy in Full

- Try Usage-Based Car Insurance

- Monitor Price Changes to Your Policy

Smart tactics can help you find affordable insurance without sacrificing quality.

Clearsurance’s Approach to Company Ratings

Are you curious about how Clearsurance figures out the scores for insurance companies? Our unique algorithm looks at many pieces of information from our community, which comprises honest insurance customers. They give us various inputs like:

- Cost

- Customer Service

- Overall Experience

- Claim Service

- Purchasing Experience

Clearsurance’s ratings give you a straightforward look at how insurance companies stack up based on honest customer feedback on cost, service, and claims. Getting honest insights and finding the best fit for your needs is easy. (Read More: Clearsurance’s Customers’ Choice Top Ranked Insurance Companies).

Accessing Additional Insurance Information

Whether you’re buying your insurance direct or going through an agent, understanding the different car insurance coverage options is a must. Do you know what is covered by comprehensive coverage? Are you familiar with uninsured motorist coverage? Do you know how a deductible works?

We want to make sure you’re equipped with a proper knowledge of car insurance, so check out our practical guide to understanding car insurance. Looking for more educational information about car insurance? Check out our blog for more information and topics related to car insurance.

We also have a free tool that will let you compare quotes from different companies. The insurance industry is vast, so having tools and reference guides to help you will make the process a little smoother.

Frequently Asked Questions

What is SR-22 insurance in TN?

SR-22 insurance in TN is proof of financial responsibility required by the state for high-risk drivers to ensure they meet Tennessee's minimum liability coverage requirements.

What is the cheapest SR-22 insurance in TN?

The cheapest SR-22 insurance in TN starts at $18 per month, depending on the provider and your driving record.

What is the non-owner of SR-22 insurance in TN?

Non-owner SR-22 insurance in Tennessee covers drivers who don't own a vehicle but must file an SR-22 to comply with Tennessee's financial responsibility laws. Choosing the best Tennessee SR-22 insurance ensures you get affordable rates and reliable coverage, even if you don't own a car.

How long do I have to keep SR-22 insurance in Tennessee?

You must keep SR-22 insurance in Tennessee for 3 to 5 years, depending on your violation and court requirements.

What is an SR-22 auto insurance policy in Nashville, TN?

An SR-22 auto insurance policy in Nashville, TN, ensures compliance with Tennessee state laws for drivers who require SR-22 filing after violations.

What is The General SR-22 insurance?

The General SR-22 insurance provides affordable policies and quick SR-22 filings for high-risk drivers requiring proof of financial responsibility, as highlighted in The General auto insurance reviews for its efficiency and cost-effectiveness.

How do I get SR-22 insurance in Memphis?

To get SR-22 insurance in Memphis, contact a licensed provider that offers SR-22 filing and meets Tennessee's insurance requirements.

Where can I find SR-22 insurance in Kingsport?

You can find SR-22 insurance in Kingsport through local or nationwide providers offering affordable SR-22 policies for drivers in Kingsport.

Where is the best place to get SR-22 insurance?

The best place to get SR-22 insurance depends on your needs. Companies like Progressive, Geico, and State Farm are top choices in Tennessee, recognized as one of the Top U.S. States with the highest car insurance claim satisfaction rates.

How do I check my SR-22 status in Tennessee?

You can check your SR-22 status in Tennessee by contacting the Tennessee Department of Safety or your insurance provider for updates.

Where do I send my SR-22 in Tennessee?

If you have insurance in Tennessee, your provider will send the SR-22 paperwork to the state's DHS.

Can I get cheap coverage insurance with SR-22?

Yes, some providers, such as Progressive, offer cheap full coverage insurance with SR-22, starting at rates as low as $18 per month, which can help offset why your car insurance rates increased after filing an SR-22.

How can I get an SR-22 insurance quote?

Contact providers like Progressive, Geico, or State Farm for personalized rate estimates and an SR-22 insurance quote.

How to file SR-22 in Tennessee?

To file SR-22 in Tennessee, work with your insurance provider to submit the form to the Tennessee Department of Safety.

Does State Farm offer SR-22?

State Farm offers SR-22 insurance with competitive rates and reliable filing options for high-risk drivers.

Does the Farm Bureau offer SR-22 insurance?

Farm Bureau insurance review offers SR-22 insurance for Tennessee drivers needing proof of financial responsibility.

What insurance companies accept SR-22?

Progressive, Geico, State Farm, Allstate, and The General are insurance companies accepting SR-22.

Does Allstate offer SR-22?

Allstate provides SR-22 insurance for high-risk drivers with competitive rates and tailored coverage options.

Does Elephant insurance offer SR-22?

Elephant insurance offers SR-22 insurance, but availability and rates may vary by state and driver profile, as detailed in the Elephant auto insurance review, highlighting its tailored options for high-risk drivers.

What is Progressive insurance SR-22?

Progressive insurance SR-22 offers affordable rates, starting at $18 monthly, with quick and reliable filing for high-risk Tennessee drivers.

Are you prepared to access more affordable auto insurance? Enter your ZIP code to start.