Best Oregon SR-22 Insurance in 2026 (See the Top 10 Companies Here!)

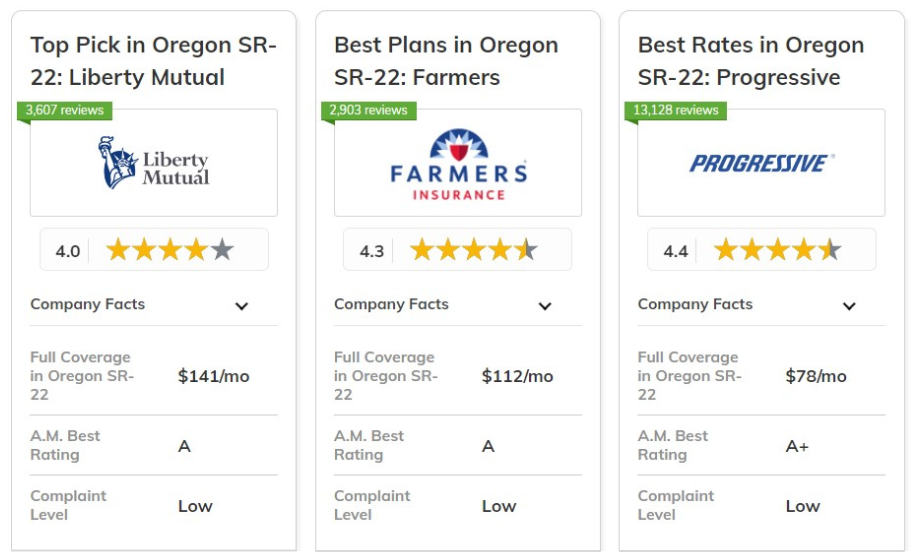

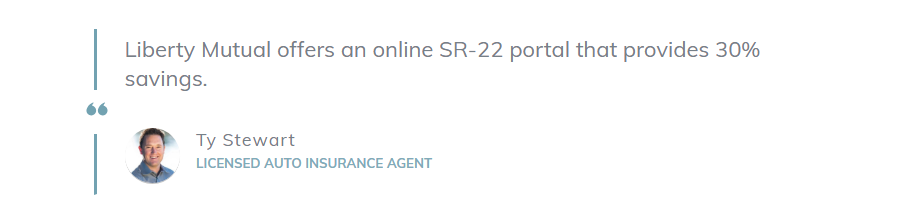

Liberty Mutual, Farmers, and Progressive offer the best Oregon SR-22 insurance. Liberty Mutual offers an online SR-22 portal that provides 30% savings.

Farmers has agents specially trained in SR-22 regulations of Oregon, while Progressive's Name Your Price feature assists drivers in getting low coverage costs starting as low as $30 per month.

| Company | Rank | UBI Savings | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 30% | A | Comprehensive Coverage | Liberty Mutual | |

| #2 | 15% | A | Customizable Plans | Farmers | |

| #3 | 30% | A+ | Competitive Rates | Progressive | |

| #4 | 40% | A+ | Reliable Service | Nationwide | |

| #5 | 20% | A | Affordable Options | American Family | |

| #6 | 25% | A++ | Competitive Rates | Geico | |

| #7 | 40% | A+ | Strong Reputation | Allstate | |

| #8 | 20% | A++ | Flexible Policies | Travelers | |

| #9 | 30% | A++ | Military Focused | USAA | |

| #10 | 30% | B | Customer Satisfaction | State Farm |

Oregon requires SR-22 insurance for violations like DUIs or driving without insurance, typically increasing costs by 61.5% for three years. (Learn More: How Long Does a DUI Stay on Your Record?)

Our free quote comparison tool allows you to shop for quotes from the top providers near you by entering your ZIP code above.

What You Should Know

- Liberty Mutual offers the best overall SR-22 insurance in Oregon

- When you search for cheap SR22 insurance in Oregon, consider the discounts available

- USAA provides the lowest rates for SR-22 insurance in Oregon at just $30 per month

#1 – Liberty Mutual: Top Overall Pick

Pros

- Online SR-22 Portal: Easy SR-22 filing in Oregon by using Liberty's online portal. Read more abouut this platform in our car insurance review of Liberty Mutual.

- Risk-Specific Discounts: Offers unique discounts designed for high-risk drivers in Oregon.

- Accident Forgiveness: Prevents further rate increases for Oregon SR-22 filers due to their accident forgiveness program.

Cons

- Premium Costs: Initial premiums are high for SR-22 insurance in Oregon compared to other competitors.

- Mixed Reviews: They have usually mixed reviews about their customer service experience, this can be challenging for drivers in Oregon.

#2 – Farmers: Best for Customizable Plans

Pros

- Specialized Agents: It trains its agents on how to manage SR-22 requirements in Oregon.

- Signal App: It's a unique app from Farmers that monitors Oregon SR-22 drivers. Learn more in our Farmers car insurance review.

- Flexible Payment Plans: Provides different methods to pay for Oregon drivers who need an SR22.

Cons

- High-Risk Pricing: An SR-22 will drive up the rates for drivers in Oregon.

- Claims Timeline: SR-22 policyholders in Oregon may find themselves in a long and painful claim process.

#3 – Progressive: Best for Competitive Rates

Pros

- Name Your Price Tool: Allows Oregon drivers to find SR-22 coverage that fits their budget constraints.

- Snapshot Program: They provide insurance that is useful for SR-22 filers in Oregon. Read more in our Progressive car insurance review.

- 24/7 Support: Offers round-the-clock customer service for Oregon drivers needing SR-22 insurance.

Cons

- Coverage Limitations: SR-22 policies in Oregon may not be covered for some sort of specialized coverage.

- Potential Rate Increases: Premiums may rise more steeply after incidents for SR-22 filers in Oregon.

#4 – Nationwide: Best for Reliable Service

Pros

- Quick Filing: Rapid SR-22 filing services for Oregon drivers needing immediate proof of insurance. See how quick they are in our Nationwide car insurance review.

- Vanishing Deductible: Provides a unique program that could benefit Oregon SR-22 filers over time.

- On Your Side Review: Annual policy review to ensure Oregon drivers have appropriate SR-22 coverage.

Cons

- Limited Local Presence: Fewer physical offices in Oregon compared to some competitors.

- Complex Policies: SR-22 policy terms may be more difficult to understand for some Oregon drivers.

#5 – American Family: Best for Affordable Options

Pros

- Educational Resources: Detailed information about Oregon SR-22 requirements.

- KnowYourDrive Program: Offers a telematics program that could help Oregon SR-22 filers improve their driving habits.

- Diminishing Deductible: Features a program that could reduce out-of-pocket costs for Oregon SR-22 policyholders over time.

Cons

- Limited Availability: According to our American Family insurance reviews, they have limited availability in Oregon for SR-22 filing.

- Higher Base Rates: Initial premiums for SR-22 policies may be higher than some competitors in Oregon.

#6 – Geico: Best for Competitive Rates

Pros

- Digital SR-22 Tools: Provides sophisticated web and application resources for operating SR-22 policies in Oregon.

- Automated Reminders: Notification system to monitor when it is time to renew an SR-22 form in Oregon.

- Multi-Policy Bundling: Provides possible Oregon SR-22 filers with multiple policy discounts on the same auto insurance policy.

Cons

- Limited Personalization: There are fewer choices of customization of SR-22 policies within Oregon, read more in our Geico car insurance review.

- Restricted Agent Access: Limited in-person support for Oregon drivers preferring face-to-face SR-22 assistance.

#7 – Allstate: Best for Strong Reputation

Pros

- Dedicated SR-22 Team: Hires professionals who are concerned with the right SR-22 compliance for Oregon drivers.

- Drivewise Program: Offers a unique telematics program that could help Oregon SR-22 filers earn discounts.

- Claim Satisfaction Guarantee: Offer an assurance for satisfactory claim settlements important to Oregon SR-22 policyholders.

Cons

- Higher Premiums: It might be costly than the normal Oregon insurance policy rates for SR-22 policy. (Read More: Allstate Car Insurance Review)

- Limited Online Services: Some SR-22 related tasks may require agent assistance rather than online self-service in Oregon.

#8 – Travelers: Best for Flexible Policies

Pros

- Customizable Policies: Offers highly flexible policy terms to meet various SR-22 needs in Oregon.

- IntelliDrive Program: Provides a smartphone app to potentially lower rates for safe Oregon SR-22 drivers.

- Accident Forgiveness: Includes an accident forgiveness option that could benefit Oregon SR-22 filers.

Cons

- Eligibility Restrictions: Stricter eligibility criteria for SR-22 policies in Oregon, learn their restrictions in our Travelers car insurance review.

- Complex Quotes: Getting a quote for SR-22 insurance in Oregon may take lot of time as compared to other providers.

#9 – USAA: Best for Military Focused

Pros

- Military Expertise: Specializes in serving military members and their families needing SR-22 in Oregon.

- Competitive Rates: Qualified Oregon military members have cheaper quotations for SR-22 insurance. Learn more about their prices in our USAA car insurance review.

- SR-22 Removal Assistance: Provides guidance on removing SR-22 filing requirement for Oregon drivers when eligible.

Cons

- Limited Eligibility: Only available to military members and their families in Oregon.

- Fewer Local Offices: Little physical availability in Oregon for face-to-face SR-22 support.

#10 – State Farm: Best for Customer Satisfaction

Pros

- Extended Support: Offers programs designed for long-term SR-22 filers in Oregon.

- Drive Safe & Save: Offers a usage-based insurance plan which may be of advantage to Oregon SR-22 motorists.

- Local Agent Network: Plenty of local agents in Oregon for individualistic SR-22 help. See their offerings in our State Farm car insurance review.

Cons

- Rate Variability: Oregon SR-22 insurance rates may also differ than normal insurance rates.

- Limited Online Tools: Some SR-22 related services may require agent interaction rather than online self-service in Oregon.

Best Oregon Coverage Rates

Purchasing low cost SR22 insurance can be quite difficult in Oregon. Knowing how to switch car insurance companies to get better SR-22 coverage can help you ease in purchasing SR-22 insurance.

This table shows monthly premiums for minimum and full coverage by top car insurance companies, and easiest ways to get cheap insurance with SR22. For SR22 Oregon no car insurance or regular SR22 car insurance: USAA and State Farm give you some of the best deals.

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $78 | $153 | |

| $54 | $106 | |

| $57 | $112 | |

| $47 | $93 | |

| $71 | $141 | |

| $56 | $111 | |

| $39 | $78 | |

| $38 | $75 | |

| $49 | $97 | |

| $30 | $58 |

Use this guide to begin your search for SR22 car insurance quotes in regions including, but not limited to Eugene or Ashland, Oregon. Do not forget about the cost/quality while searching for the company that will offer you the SR22 car insurance.

Oregon SR-22 Insurance Saving Strategies

Dealing with SR22 insurance in Oregon is not easy. Yet, knowing about the discounts can ease the burden on your wallet. If you’re looking for cheap SR22 insurance or comparing car insurance quotes in Oregon, this table offers useful information on where to save.

Keep in mind, the cost of SR-22 insurance in Oregon might be steeper than regular plans, but those discounts can lessen the blow to your premiums.

| Insurance Company | Available Discount |

|---|---|

| Multi-Policy, Good Student, Safe Driver, Anti-Theft, Defensive Driving, Loyalty, Low Mileage, Early Bird, Steer Into Savings® | |

| Multi-Policy, Safe Driver, Good Student, Homeowner, Signal® (Usage-Based), Alternative-Fuel Vehicle, Anti-Theft | |

| Multi-Vehicle, Multi-Policy, Good Driver, Good Student, Defensive Driving, Military, Federal Employee, Emergency Deployment | |

| Multi-Policy, Military, Early Shopper, Good Student, Safe Vehicle, Paperless, Online Purchase, Right Track® (Usage-Based) | |

| Multi-Policy, Defensive Driving, Anti-Theft, Paperless, Smart Ride® (Usage-Based), Accident-Free, Good Student, Affinity Member | |

| Multi-Policy, Homeowner, Good Student, Continuous Insurance, Online Quote, Paperless, Pay in Full, Snapshot® (Usage-Based) | |

| Multi-Policy, Safe Vehicle, Good Driving, Good Student, Accident-Free, Defensive Driving, Passive Restraint, Anti-Theft | |

| Multi-Policy, Safe Driver, Good Student, Homeowner, New Car, Multi-Car, Hybrid/electric Vehicle, Intelli Drive® (Usage-Based) | |

| Multi-Policy, Military, Good Student, Defensive Driving, Driver Training, New Vehicle, Safe Driver, Vehicle Storage Discount for Deployed Personnel | |

| Multi-Policy, Homeowner, Good Student, Continuous Insurance, Online Quote, Paperless, Pay in Full |

When you search for cheap SR22 insurance in Oregon, consider the discounts available. For regular car insurance in Oregon or the lowest SR22 rates, better be aware for the prices that differ widely among providers.

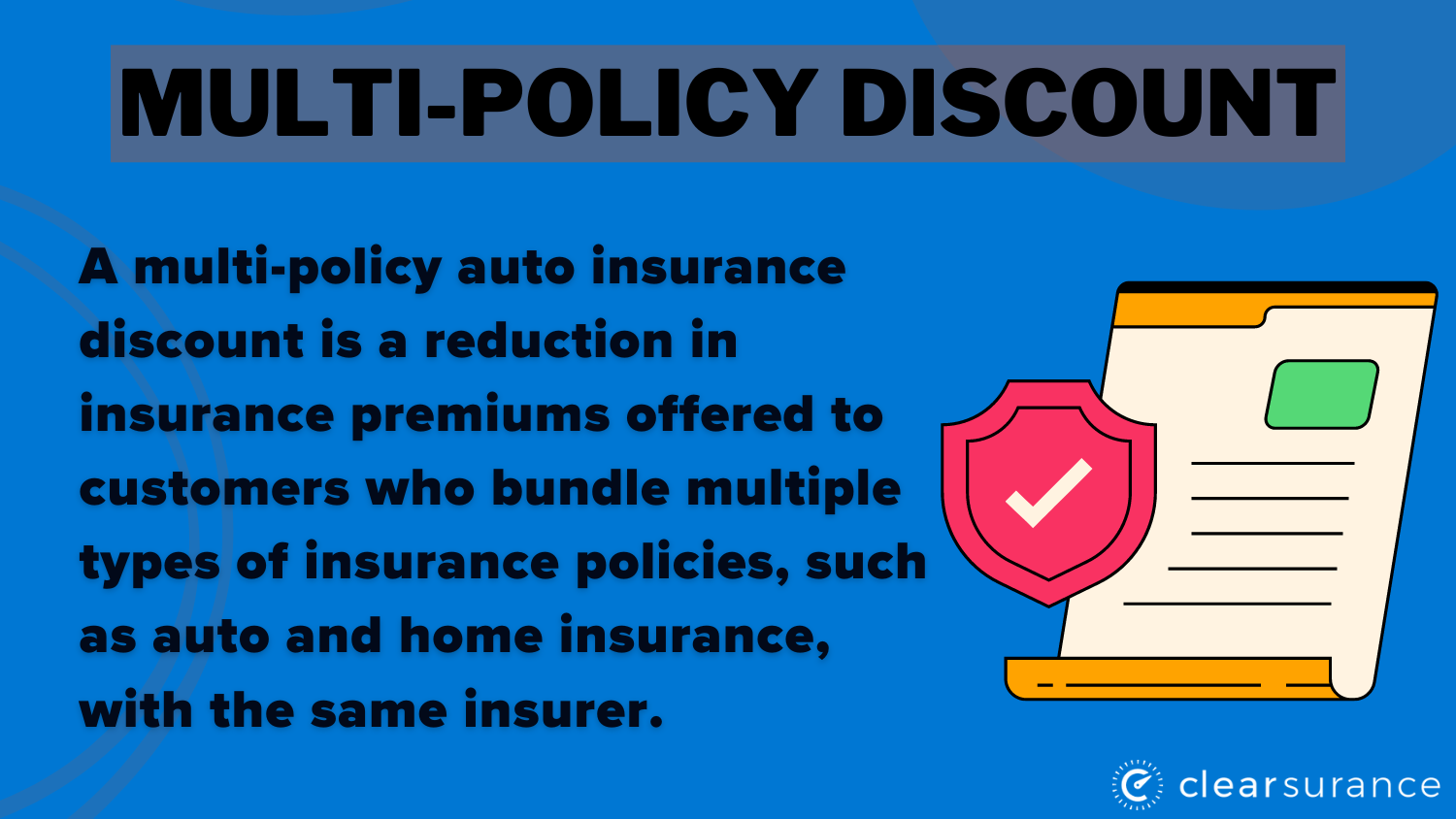

Common discount you can get from the top providers is the multi-policy discount. Explore your options, see the top ways customers have saved money on car insurance rates and compare quotes to achieve the best mix of coverage and cost for your SR22 insurance in Oregon.

Oregon SR-22 Insurance: Requirements, and Filing Process

In Oregon, if you’ve had certain run-ins with the law—like a DUI or driving without insurance—you need SR-22 insurance. So, what is SR-22 insurance in Oregon? It’s not a separate policy, but rather a form your insurance company files with the DMV, showing you have the minimum coverage.

This requirement usually raises your insurance costs by about 61.5%, lasting for three years. Make sure you find the cheapest SR-22 insurance in Oregon to reduce your insurance costs.

The minimum coverage includes $25,000 for bodily injury per person, $50,000 per accident, $20,000 for property damage, $15,000 for personal injury protection, and coverage for uninsured motorists.

To get it, you should reach out to an insurer that handles SR-22s in Oregon. Keep your coverage steady to avoid fines and losing your license. Enter your ZIP code below into our free comparison tool to see how much car insurance costs in your area.

Frequently Asked Questions

How much is SR-22 insurance in Oregon?

SR-22 insurance in Oregon typically increases insurance costs by about 61.5% compared to regular insurance rates. The cheapest option is USAA at $30 per month for minimum coverage and $58 for full coverage.

What is SR-22 insurance Oregon?

SR-22 insurance in Oregon is not a separate policy, but a form filed by your insurance company with the DMV to prove you have the minimum required coverage after certain violations.

Who needs SR-22 insurance in Oregon?

Drivers who have had certain violations like DUIs or driving without insurance are required to have SR-22 insurance in Oregon. You may also get penalty for driving without car insurance so watch out for that.

How much is an SR-22 in Oregon?

The cost of an SR-22 in Oregon varies by company. For minimum coverage, it ranges from $30 (USAA) to $78 (Allstate) per month. For full coverage, it ranges from $58 (USAA) to $153 (Allstate) per month.

How long do I need to carry SR-22 insurance in Oregon?

The SR-22 requirement in Oregon typically lasts for three years. Stop overpaying for car insurance.Our free comparison tool allows you to shop for quotes from the top providers near you by entering your ZIP code below.

Can I get SR-22 insurance if I don't own a car in Oregon?

Yes, you can get SR-22 insurance even if you don't own a car in Oregon. This is often referred to as "non-owner SR-22 insurance" or "SR-22 insurance with no car." (Read More: Cheap Non-Owner Car Insurance)

What happens if my SR-22 insurance lapses in Oregon?

If your SR-22 insurance lapses in Oregon, your insurance company is required to notify the DMV. This could result in the suspension of your driving privileges, fines, and potentially having to restart the SR-22 filing period.

Are there alternatives to SR-22 insurance in Oregon?

SR-22 is a specific requirement for certain high-risk drivers, and there may not be direct alternatives if it's mandated by the state.

Read More: Cheap Car Insurance Companies for High-Risk Drivers

How does SR-22 insurance affect my regular auto insurance rates in Oregon?

SR-22 insurance typically increases your regular auto insurance rates in Oregon.

Can I file for SR-22 insurance myself in Oregon, or do I need an insurance company to do it?

You need an insurance company to file the SR-22 form on your behalf in Oregon.

See how much you’ll pay for car insurance by entering your ZIP code below into our free comparison tool.