Best Ohio SR-22 Insurance in 2026 (Find the Top 10 Companies Here)

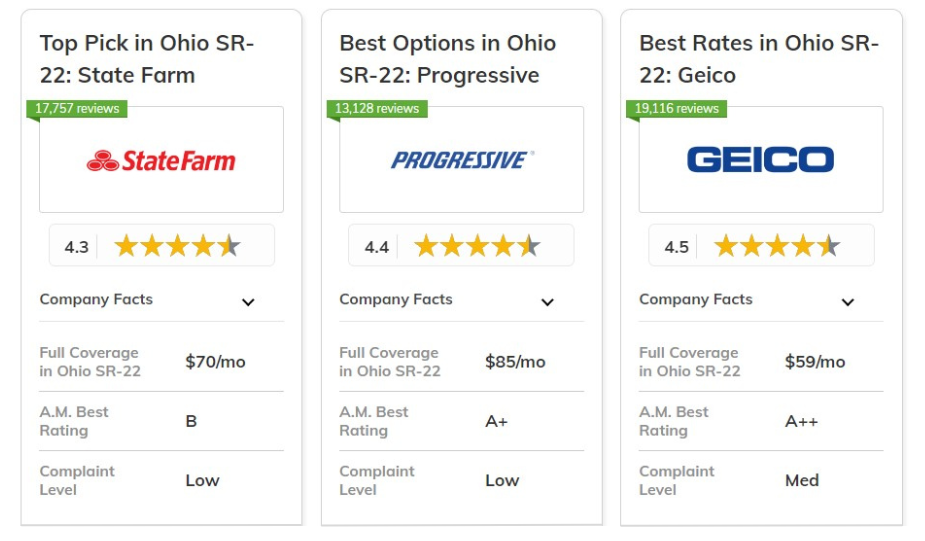

The best Ohio SR-22 insurance providers are State Farm, Progressive, and Geico, with State Farm offering the top pick overall at just $27 per month.

State Farm stands out for its reliable service and excellent customer support, ensuring peace of mind for drivers needing SR-22 coverage and access to comprehensive resources.

| Company | Rank | UBI Savings | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 30% | B | Reliable Service | State Farm | |

| #2 | 30% | A+ | Flexible Options | Progressive | |

| #3 | 25% | A++ | Affordable Rates | Geico | |

| #4 | 30% | A++ | Military Support | USAA | |

| #5 | 40% | A+ | Comprehensive Coverage | Nationwide | |

| #6 | 20% | A | Personalized Care | American Family | |

| #7 | 20% | A++ | Innovative Discounts | Travelers | |

| #8 | 30% | A | Customizable Policies | Liberty Mutual | |

| #9 | 40% | A+ | Extensive Resources | Allstate | |

| #10 | 15% | A | Trusted Experience | Farmers |

Meanwhile, Geico is known for its affordable rates, providing budget-friendly and highly competitive insurance solutions for SR-22 coverage in Ohio to all drivers.

Start comparing affordable insurance options by entering your ZIP code above into our free quote comparison tool today.

What You Should Know

- State Farm is the top pick for the best Ohio SR-22 insurance at just $27 per month

- Its reliable service provides peace of mind for drivers needing SR-22 coverage

- Customers value the affordability and flexibility of State Farm’s SR-22 insurance options

On this page:

#1 – State Farm: Top Overall Pick

Pros

- Reliable Customer Service: State Farm is known for its extensive network of agents, providing personalized service and support for policyholders.

- Strong Financial Stability:Our analysis of State Farm insurance customer reviews reveals that with a high financial rating, State Farm ensures it can meet its policyholder obligations effectively, making it one of the best Ohio SR-22 insurance options for reliable coverage.

- User-Friendly Mobile App: State Farm offers a well-designed mobile app, allowing customers to manage their policies easily and file claims on the go.

Cons

- Limited Online Options: While they offer great in-person service, their online tools may not be as user-friendly or comprehensive as some competitors.

- Higher Premiums: Depending on individual risk factors, State Farm may have higher premiums compared to other providers.

#2 – Progressive: Best for Flexible Options

Pros

- Flexible Coverage Options: Progressive offers a wide range of customizable coverage options to suit various driver needs.

- Snapshot Program: Their innovative usage-based insurance program rewards safe driving habits with potential discounts.

- 24/7 Claims Support: The findings from our Progressive insurance customer reviews demonstrate that Progressive provides around-the-clock claims assistance, ensuring help is available whenever needed, positioning itself as one of the best Ohio SR-22 insurance options for drivers.

Cons

- Mixed Customer Service Ratings: While many appreciate Progressive's service, some customers report less satisfaction with claims handling.

- Complex Pricing Structure: The variety of options and add-ons can make it confusing for some customers to find the best rate.

#3 – Geico: Best for Affordable Rates

Pros

- Affordability: Geico is widely recognized for its competitive rates, making it a popular choice for budget-conscious drivers.

- User-Friendly Online Experience: Their website and mobile app are intuitive, allowing customers to easily manage policies and file claims.

- Extensive Discounts: Geico offers a variety of discounts, including those for good drivers and military personnel, making it easier to save on premiums.

Cons

- Limited Local Agent Access: Geico primarily operates online, which may not be ideal for those who prefer face-to-face interaction with agents.

- Customer Service Variability: While some customers report inconsistent experiences with customer service representatives, Progressive still stands out among the best Ohio SR-22 insurance options. You may explore our comparison article on "Progressive vs. Geico: Which car insurance company do customers say is better?"

#4 – USAA: Best for Military Support

Pros

- Exclusive Member Benefits: According to our USAA customer ratings, USAA provides tailored insurance products and discounts exclusively for military members and their families, ensuring they receive competitive coverage options that cater to their unique needs.

- Exceptional Customer Satisfaction: Known for high ratings in customer service, USAA is often praised for its responsive and helpful support team.

- Competitive Rates: USAA typically offers lower premiums than many competitors, making it a cost-effective choice for eligible members.

Cons

Membership Eligibility Restrictions: Only active and former military personnel and their families can access USAA, limiting its customer base. Fewer Coverage Options: Compared to larger insurers, USAA may offer a more limited selection of coverage types and add-ons.

#5 – Nationwide: Best for Comprehensive Coverage

Pros

- Comprehensive Coverage Options: Nationwide offers a wide array of insurance products, allowing customers to bundle for additional savings.

- Strong Financial Ratings: Our assessment of Nationwide customer reviews illustrates that with solid financial stability, Nationwide can effectively meet its policyholder obligations, securing its spot as one of the best Ohio SR-22 insurance options for reliable coverage.

- Innovative Tools: Nationwide provides helpful online tools and resources to assist customers in managing their policies and claims.

Cons

- Higher Average Rates: Nationwide's premiums can be on the higher side, which may not appeal to all budget-conscious consumers.

- Variable Customer Service Experiences: Some customers report inconsistent experiences with claims handling and support.

#6 – American Family: Best for Personalized Care

Pros

- Customized Policies: American Family provides options to tailor policies based on individual needs and preferences.

- Strong Commitment to Community: The company actively engages in community initiatives, enhancing its reputation as a socially responsible insurer.

- Extensive Discount Options: Our examination of American Family Insurance customer ratings shows that American Family offers numerous discounts, helping customers save on their premiums and securing its place as one of the best Ohio SR-22 insurance options.

Cons

- Limited Availability: American Family may not operate in all states, restricting access for some potential customers.

- Higher Premiums for High-Risk Drivers: Drivers with a less-than-perfect record may face steeper premiums compared to other companies.

#7 – Travelers: Best for Innovative Discounts

Pros

- Wide Range of Discounts: Travelers offers various discounts, allowing drivers to save based on their unique circumstances.

- Comprehensive Coverage Options: Our Travelers Companies, Inc. customer reviews indicate that Travelers provides robust coverage options to meet diverse driver needs, positioning itself as one of the best Ohio SR-22 insurance options for comprehensive protection..

- Strong Claims Support: Travelers has a reputation for providing efficient claims processing and support, helping customers through the claims journey.

Cons

- Customer Service Variability: Experiences with customer service can vary, leading to mixed reviews from policyholders.

- Complex Policy Terms: Some customers find Travelers' policy terms and conditions difficult to navigate and understand.

#8 – Liberty Mutual: Best for Customizable Policies

Pros

- Extensive Coverage Options: Liberty Mutual offers a broad range of coverage options, including specialized policies for various needs.

- Unique Discounts: The company provides various discounts, such as for new car safety features, helping drivers save money.

- Personalized Support: Our Liberty Mutual insurance customer reviews highlight that Liberty Mutual’s agents offer personalized guidance to help customers choose the best coverage for their needs, securing its place as one of the best Ohio SR-22 insurance options.

Cons

- Higher Premiums: Liberty Mutual is often associated with higher rates, which may not be ideal for cost-conscious customers.

- Mixed Customer Reviews: Some customers report dissatisfaction with claims processes and overall service quality.

#9 – Allstate: Best for Extensive Resources

Pros

- Well-Rounded Coverage: Allstate offers a comprehensive suite of insurance products, allowing for convenient bundling.

- Strong Financial Stability: Based on our Allstate customer reviews, Allstate’s solid financial rating ensures reliability in meeting policyholder claims, making it one of the best Ohio SR-22 insurance options for drivers seeking dependable coverage.

- Unique Programs: Allstate provides unique programs, such as the “Drivewise” program, which rewards safe driving habits with discounts.

Cons

- Higher Rates for Some Drivers: Allstate may charge higher premiums, particularly for drivers with less-than-ideal records.

- Inconsistent Customer Service: Some customers report varying levels of satisfaction with customer support and claims handling.

#10 – Farmers: Best for Trusted Experience

Pros

- Comprehensive Policy Options: The results of our Farmers insurance customer reviews suggest that Farmers offers a variety of coverage options, including specialty policies to meet unique driver needs, making it one of the best Ohio SR-22 insurance options for tailored protection.

- Strong Customer Service Reputation: Farmers is known for its responsive customer service and helpful agents who provide personalized support.

- Numerous Discount Opportunities: Farmers provides a wide range of discounts, including safe driver and multi-policy discounts, helping drivers save.

Cons

- Higher Premiums: Farmers may charge higher rates compared to other providers, especially for high-risk drivers.

- Limited Online Tools: While Farmers provides quality customer service, their online tools and digital services may not be as robust as competitors.

Budget-Friendly Ohio SR-22 Insurance: Compare Leading Provider Rates

If you’re searching for the best Ohio SR-22 insurance, providers such as State Farm, Progressive, and Geico offer attractive rates. With monthly premiums starting around $27, affordable options are available to fulfill Ohio’s SR-22 requirements.

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $46 | $120 | |

| $24 | $62 | |

| $37 | $96 | |

| $23 | $59 | |

| $41 | $106 | |

| $44 | $114 | |

| $33 | $85 | |

| $27 | $70 | |

| $25 | $63 | |

| $16 | $41 |

Securing the right SR-22 insurance in Ohio can be straightforward and stress-free. Compare rates from these leading providers to find budget-friendly coverage that meets state regulations while keeping you safe on the road.

Top Providers for the Best Ohio SR-22 Insurance

Securing the best Ohio SR-22 insurance requires finding providers that excel in affordability, experience, and flexibility. Below are the key features that top insurance companies offer for SR-22 coverage in Ohio.

- Expert Filing: Top providers are skilled in handling SR-22 filings, ensuring fast and accurate submission to the Ohio BMV.

- Competitive Rates: Leading companies offer affordable SR-22 insurance rates, even for high-risk drivers, helping to manage premium costs.

- Flexible Payments: The best Ohio SR-22 insurers provide flexible payment plans to accommodate different financial situations and make maintaining coverage easier.

By focusing on expert filing, competitive rates, and flexible payments, you can find the best Ohio SR-22 insurance provider that meets your needs and budget.

These factors will help you comply with state requirements without overpaying for coverage.

Requirements for the Best Ohio SR-22 Insurance Coverage

Understanding the best Ohio SR-22 insurance involves knowing the requirements set by the state and insurers. Below are the essential criteria to meet for SR-22 coverage in Ohio.

- Proof of Insurance: Drivers must provide proof of insurance to obtain an SR-22, demonstrating that they meet the state’s minimum liability requirements.

- Clean Driving Record: Maintaining a clean driving record is essential, as insurers may consider your history when determining eligibility and rates for Ohio SR-22 insurance. To gain further insights, consult our comprehensive guide titled "What Is Considered a Clean Driving Record?"

- State Compliance: It’s crucial to comply with Ohio’s specific SR-22 requirements, including timely renewals and updates, to avoid penalties.

By understanding the requirements for the best Ohio SR-22 insurance coverage, including comprehensive coverage, you can ensure that you remain compliant and protected.

Meeting these criteria will help you maintain your driving privileges and avoid potential legal issues.

Unlock Savings on Ohio SR-22 Insurance

This table showcases the discounts available from top Ohio SR-22 insurance providers. Each company offers various discounts, including multi-policy, safe driver, and low mileage, enabling high-risk drivers to reduce their SR-22 insurance costs.

| Insurance Company | Available Discount |

|---|---|

| Auto & Home Bundle, Loyalty, Defensive Driver, Safe Driver | |

| Signal Program, Good Student, Home & Auto Bundle, Anti-Theft | |

| Multi-Policy, Good Driver, Seat Belt Use, Military, Good Student | |

| RightTrack, Multi-Car, Early Shopper, Online Purchase | |

| SmartRide, Multi-Policy, Accident-Free, Paperless | |

| Safe Driver, Multi-Car, Homeowner, Paperless, Pay in Full | |

| Safe Driver, Multi-Policy, Vehicle Safety, Good Student | |

| Multi-Policy, Hybrid/Electric Vehicle, Good Payer, Continuous Coverage | |

| Safe Driver, Bundling, Military, Defensive Driving | |

| Multi-Policy, Hybrid/Electric Vehicle, Good Payer |

Taking advantage of these discounts is an effective strategy for saving on Ohio SR-22 insurance. Compare the options from these leading providers to find the best deals and fulfill your SR-22 requirements affordably.

Ohio SR-22 Insurance Rates Breakdown

If you need to file an SR-22 in Ohio, expect your car insurance rates to increase significantly. Being required to have an SR-22 classifies you as a high-risk or non-standard driver, which typically results in the highest insurance rates.

However, costs can vary by company and depend on factors like age, gender, location, credit score, vehicle type, and marital status.

A common reason for needing SR-22 insurance is a DUI conviction (OVI in Ohio). On average, drivers with one OVI conviction in Ohio pay about $1,381 annually for car insurance—63% more than drivers with clean records.

However, rates can vary significantly based on the insurance company. The table below shows average rates for Ohio drivers with one OVI conviction from some of the largest companies in the state.

| Company | Car insurance rate |

|---|---|

| American Family | $638 |

| USAA* | $922 |

| Geico | $1,070 |

| Farmers | $1,080 |

| Erie | $1,210 |

| State Farm | $1,348 |

| Safeco | $1,371 |

| Nationwide | $1,525 |

| Auto-Owners | $1,595 |

| Progressive | $1,677 |

| Cincinnati Insurance Company | $1,731 |

| Allstate | $1,781 |

*USAA is only available to active and former military members and their families.

*These rates are based on a 35-year-old single adult with one driver and one vehicle on a policy. The car used was a 2015 Toyota Highlander LEs. Full coverage was used with 100/300/50 limits and a $500 collision and comprehensive deductible.

The driver had 1 DUI on their record. The rates displayed should only be used for comparative purposes as individual rates for high-risk insurance in Alabama will differ. Rate data is provided by Quadrant Information Services.*

No matter how much coverage you need, you can find the lowest rates by entering your ZIP code into our free comparison tool below.

Frequently Asked Questions

How much does SR-22 insurance cost in Ohio per month?

SR-22 insurance in Ohio typically costs between $50 and $150 per month, depending on factors like your driving history and insurance provider.

Does SR-22 cover any car I drive in Ohio?

Yes, SR-22 insurance covers any vehicle you drive in Ohio, provided the policy meets the state's minimum liability coverage requirements.

What is the penalty for driving without insurance in Ohio?

The penalty for driving without insurance in Ohio can include fines, suspension of your driver’s license, vehicle impoundment, and the requirement to file SR-22 insurance.

What happens if my SR-22 lapses in Ohio?

If your SR-22 lapses in Ohio, your license may be suspended, and you could face fines or other penalties until you reinstate the SR-22 filing.

How long is SR-22 required in Ohio?

In Ohio, SR-22 insurance is typically required for three to five years, depending on the offense and court rulings.

How do I get SR-22 insurance in Ohio?

To get SR-22 insurance in Ohio, you must contact your auto insurance company and request they file the SR-22 form with the Ohio Bureau of Motor Vehicles (BMV) on your behalf.

Do I need an SR-22 to reinstate my license in Ohio?

Yes, if your license was suspended due to certain violations, you will need SR-22 insurance to reinstate your license in Ohio.

How do I check my SR-22 status in Ohio?

You can check your SR-22 status by contacting the Ohio BMV or your insurance company to verify whether your SR-22 is still active and valid.

Why is Ohio auto insurance so cheap?

Ohio auto insurance is generally cheaper due to lower accident rates, mild weather conditions, and fewer uninsured drivers compared to other states.

To delve deeper, refer to our in-depth report titled "5 Steps to Take After a Car Accident."

What is the best company for SR-22 insurance in Ohio?

The best company for SR-22 insurance in Ohio depends on your specific needs, but popular options include Geico, State Farm, and Progressive, known for affordable rates and strong