Best Missouri SR-22 Insurance in 2026 (Top 10 Companies Ranked)

The best Missouri SR-22 insurance are from Nationwide, State Farm, and Geico, with minimum coverage starting at $18 per month. Nationwide offers an "On Your Side Review" to help SR-22 filers optimize coverage and discounts.

State Farm provides local agent expertise on Missouri requirements. Geico's DriveEasy program allows SR-22 filers to earn discounts through safe driving. High-risk drivers can lower costs at these insurers by switching car insurance companies to save money.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 20% | A+ | Affordable Rates | Nationwide | |

| #2 | 17% | B | Reliable Service | State Farm | |

| #3 | 25% | A++ | Broad Discounts | Geico | |

| #4 | 10% | A++ | Military Benefits | USAA | |

| #5 | 10% | A+ | Usage Flexibility | Progressive | |

| #6 | 25% | A | Customer Loyalty | American Family | |

| #7 | 13% | A++ | Consistent Savings | Travelers | |

| #8 | 25% | A | Diverse Coverage | Liberty Mutual | |

| #9 | 20% | A | Custom Options | Farmers | |

| #10 | 25% | A+ | Comprehensive Plans | Allstate |

In this article, we explore Missouri's SR-22 insurance essentials, rates and discounts. See if you’re getting the best deal on car insurance by entering your ZIP code above.

What You Should Know

- Nationwide provides an annual "On Your Side Review" to optimize coverage

- State Farm offers the Steer Clear program for young drivers to earn discounts

- Geico's DriveEasy program allows Missouri SR-22 filers to earn discounts

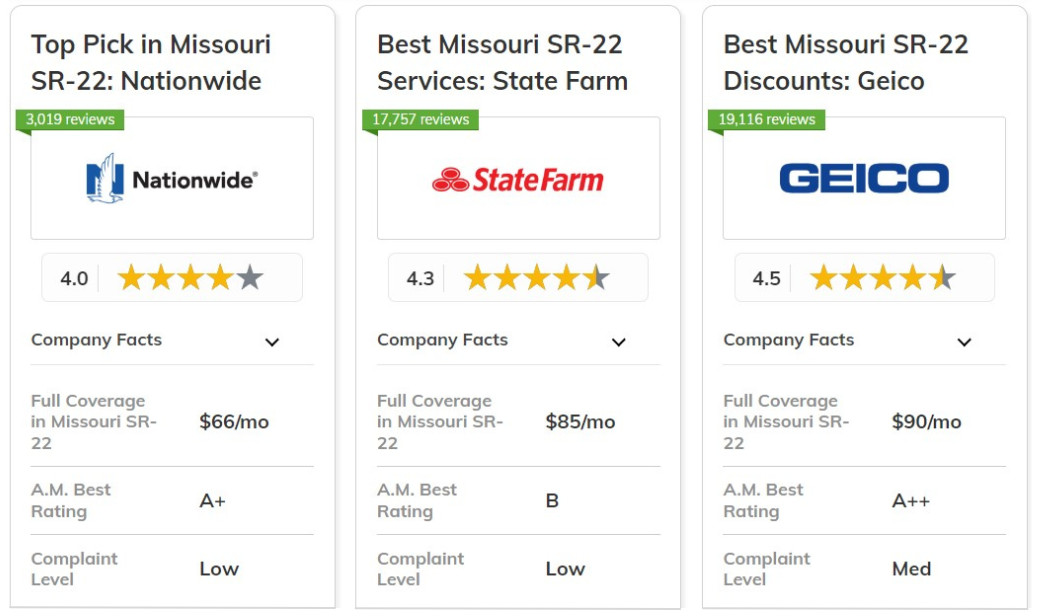

#1 – Nationwide: Top Overall Pick

Pros

- Budget-Friendly Premiums: Nationwide offers cost-effective SR-22 insurance rates in Missouri at $23/month for minimum coverage.

- On Your Side Review: Annual policy review helps Missouri SR-22 filers optimize their coverage and discounts.

- SmartMiles Program: Pay-per-mile option for low-mileage Missouri drivers needing SR-22 coverage. Learn more about this program in our Nationwide car insurance review.

Cons

- Coverage Gaps: Specialized coverages are unavailable for Missouri SR-22 policyholders.

- Average Customer Service: Missouri SR-22 filers experience longer wait times for support compared to other insurers.

#2 – State Farm: Best for Reliable Service

Pros

- Local Agent Expertise: State Farm's local network of agents is a great benefit for Missouri SR-22 filers.

- Steer Clear Program: Young Missouri drivers earn discounts by completing this safe driving program. (Read More: State Farm Car Insurance Review)

- Banking Services Integration: Missouri law allows State Farm policyholders to link insurance payments to State Farm banking products for potential benefits.

Cons

- Traditional Approach: State Farm's conventional methods don't appeal to tech-savvy Missouri SR-22 filers.

- Limited Risk Acceptance: Drivers with severe violations struggle to obtain SR-22 coverage with State Farm in Missouri.

#3 – Geico: Best for Broad Discounts

Pros

- DriveEasy Program: Geico tracks safe driving habits of its Missouri SR-22 filers through the app and applies a discount.

- Prime Time Contract: Guaranteed renewability for Missouri drivers over 50 meeting certain criteria.

- Efficient Claims Process: Geico has streamlined how Missouri policyholders can file a car insurance claim.

Cons

- Limited Physical Offices: Missouri SR22 filers have trouble finding local Geico agents for in-person assistance.

- Basic Policies: Geico's basic list of coverage isn't as exclusive as some of the other insurers in Missouri.

#4 – USAA: Best for Military Benefits

Pros

- Military-Focused Perks: Offers unique benefits like vehicle storage discounts for deployed Missouri service members.

- SafePilot Program: Missouri SR-22 filers earn up to 30% off for safe driving habits. Learn more about this program in our USAA car insurance review.

- Accident Forgiveness: First at-fault accident forgiveness for qualifying Missouri policyholders.

Cons

- Strict Membership Criteria: Only available to military members, veterans, and their families in Missouri.

- Limited Product Offerings: Specialized insurance products are unavailable for Missouri SR-22 filers.

#5 – Progressive: Best for Usage Flexibility

Pros

- Name Your Price Tool: Helps Missouri SR22 filers get the most for their money and the right kind of coverage. (Learn More: Progressive Car Insurance Review)

- Snapshot Rewards: Immediate discount for Missouri drivers who sign up for this usage-based program.

- Pet Injury Coverage: Included with collision coverage for Missouri policyholders at no extra charge.

Cons

- Rate Fluctuations: Missouri SR-22 insurance rates with Progressive increase more after violations compared to competitors.

- Average Customer Satisfaction: Progressive has had mixed customer service experiences, according to Missouri policyholders.

#6 – American Family: Best for Customer Loyalty

Pros

- DreamSecure Senior Term Life: As mentioned in our review of American Family car insurance they offer life insurance options for Missouri SR-22 filers over 50.

- MyAmFam App: Provides easy policy management and digital ID cards for Missouri policyholders.

- Diminishing Deductible: Missouri drivers earn credits towards their deductible for each year of safe driving.

Cons

- Regional Limitations: Coverage is unavailable in certain parts of Missouri.

- Higher Rates: SR-22 insurance premiums in Missouri are higher than competing providers.

#7 – Travelers: Best for Consistent Savings

Pros

- IntelliDrive Program: Missouri SR-22 filers save based on driving behavior monitored through a smartphone app.

- Affinity Group Discounts: Special rates for Missouri SR-22 policyholders affiliated with partner organizations. (Read More: Travelers Car Insurance Review)

- Responsible Driver Plan: Offers accident and minor violation forgiveness for eligible Missouri drivers.

Cons

- Complex Policies: Missouri SR-22 filers find Travelers' coverage options and terms difficult to understand.

- Limited Local Presence: Fewer physical locations in Missouri for in-person SR-22 assistance.

#8 – Liberty Mutual: Best for Diverse Coverage

Pros

- RightTrack Program: Missouri SR-22 filers save through this usage-based insurance option. As mentioned in our car insurance review of Liberty Mutual.

- Teacher and Military Discounts: Special rates for Missouri educators and service members needing SR-22 coverage.

- 12-Month Rate Guarantee: Offers rate protection for Missouri SR-22 policyholders for a full year.

Cons

- Above-Average Premiums: Liberty Mutual's SR-22 insurance in Missouri is pricier than many competitors.

- Inconsistent Customer Service: Missouri policyholders report varying experiences with claims handling and support.

#9 – Farmers: Best for Custom Options

Pros

- Signal Program: Missouri SR-22 filers earn discounts based on safe driving habits tracked through Farmers' app.

- Rideshare Coverage: Specialized protection for Missouri SR-22 filers who also drive for rideshare companies.

- Incident Forgiveness: In our Farmers car insurance review they forgive one at-fault accident for every three years of safe driving for Missouri policyholders.

Cons

- Higher Than Average Rates: Farmers SR22 insurance in Missouri costs more than other competitors.

- Complicated Quote Process: Missouri SR-22 filers find obtaining accurate quotes from Farmers time-consuming.

#10 – Allstate: Best for Comprehensive Plans

Pros

- Drivewise Program: Missouri SR-22 filers earn cash back for safe driving through Allstate's telematics option.

- Claim Satisfaction Guarantee: Allstate offers a guarantee for Missouri SR-22 policyholders' satisfaction with claims handling.

- Deductible Rewards: Learn how Missouri drivers can reduce their deductible by $100 for each year of safe driving, up to $500 in our Allstate car insurance review.

Cons

- Expensive Premiums: Allstate's SR-22 insurance in Missouri is often more costly than many competitors.

- Limited Discounts: Missouri SR22 filers have fewer cost-saving opportunities with Allstate than other insurers.

Missouri SR-22 Insurance Cost

In Missouri, car insurance with an SR-22 is costly. It’s not the filing fees that drive up the price. It’s the insurance premiums that rise after a driving citation leads to the need for the SR-22.

The increase in cost varies with the number and seriousness of your violations in Missouri. Compare monthly rates from Missouri's top providers in the table:

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $52 | $148 | |

| $37 | $106 | |

| $48 | $135 | |

| $32 | $90 | |

| $46 | $129 | |

| $23 | $66 | |

| $35 | $98 | |

| $30 | $85 | |

| $40 | $114 | |

| $18 | $50 |

The table reveals SR-22 insurance rates in Missouri. USAA has the lowest rates, but it is only for military families. Look beyond just the price when selecting your insurance provider and what kind of car insurance you really need . Always compare several quotes.

Missouri SR-22 Essentials

Every driver must have insurance in Missouri. If you don’t carry the minimum, you risk losing your license. The law demands certain liability coverages from all drivers. Here's Missouri requirements:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident

- $10,000 property damage per accident

Missouri requires SR-22 insurance for drivers with serious traffic violations or repeated offenses. This filing proves you maintain minimum liability coverage. Here are the main reasons you might need SR-22 insurance:

- DUI or DWI conviction.

- Driving without insurance or with a suspended license.

- Multiple traffic violations or at-fault accidents.

- Reckless driving or causing a fatal/injury accident.

- Failure to pay fines or refusing a breathalyzer test.

Remember, SR-22 filings are temporary, and with responsible driving, you can work towards standard insurance rates in the future. Read our article titled "penalty for driving without car insurance" for more information.

Finding Missouri SR-22 Discounts

SR-22 insurance in Missouri can be expensive. Still, many insurance companies provide discounts to ease the burden of costs. One common discount is for good students, who earn lower rates for their academic efforts. Let’s look at the different discounts offered by leading SR-22 insurance providers in Missouri.

As you can see, there are numerous ways to save on Missouri SR-22 insurance, even with a less-than-perfect driving record. The Good Student discount, in particular, can provide significant savings for young drivers maintaining good grades.

| Insurance Company | Available Discount |

|---|---|

| Multi-policy, Good student, Defensive driving, Auto safety equipment, Loyalty, Accident-free, Early-bird Discount | |

| Multi-policy, Safe driver, Homeowner, Bundling auto and home, Good student, Anti-theft, Alternative fuel vehicle, Signal usage-based driving Discount | |

| Multi-policy, Anti-theft, Defensive driving, Good driver, Good student, Military, Seat belt use, New vehicle, SR-22 filing Discount | |

| Multi-policy, Early shopper, Military, Hybrid vehicle, Safe driver, Homeowner, Paperless billing, Good student, Violation-free | |

| Multi-policy, Safe driver, Anti-theft, Automatic payments, Defensive driving, Good student, Accident-free, Paperless billing | |

| Multi-policy, Safe driver, Good student, Continuous insurance, Homeowner, Pay-in-full, Snapshot usage-based Discount, SR-22 Discount | |

| Multi-policy, Accident-free, Defensive driving, Safe vehicle, Good student, Vehicle safety, Anti-theft, Driver training | |

| Multi-policy, Good student, Homeowner, Safe driver, Continuous insurance, Hybrid/electric vehicle, Automatic payment, New car | |

| Multi-policy, Safe driver, Defensive driving, New vehicle, Vehicle storage, Military, Good student, Family legacy | |

| Multi-policy, Accident-free, Defensive driving, Safe vehicle, Good student, Vehicle safety, Anti-theft |

Ask your insurance provider about the discounts they offer. Think about bundling your policies or taking a defensive driving course. These steps can help reduce your costs.

It's a way to make your SR-22 insurance easier to bear while still following the law in Missouri. Our free online comparison tool below allows you to compare cheap car insurance quotes instantly — just enter your ZIP code to get started.

Frequently Asked Questions

What is SR-22 insurance in Missouri?

SR-22 is a certificate filed by your insurer proving you meet Missouri's minimum liability coverage requirements after certain traffic violations.

Read More: Does a speeding ticket affect your car insurance rates?

How do I check the status of my SR-22 in Missouri?

Contact your insurance provider or the Missouri Department of Revenue to verify your SR-22 status and ensure it's active. See if you’re getting the best deal on car insurance by entering your ZIP code below.

What are the rules for car insurance claims in Missouri?

Missouri follows a fault-based system. File claims with the at-fault driver's insurer or your own if they're uninsured.

What happens if the person at fault in an accident has no insurance in Missouri?

You can file a claim with your insurer if you have uninsured motorist coverage, or pursue legal action against the at-fault driver.

How long does Missouri require SR22 insurance?

Missouri typically requires SR-22 insurance for 2-3 years, depending on the violation. Maintain continuous coverage to avoid license suspension. (Learn More: Can I Switch Car Insurance Companies Mid-Policy?)

What are the minimum requirements for auto insurance in Missouri?

Missouri requires 25/50/25 liability coverage: $25,000 per person bodily injury, $50,000 per accident, and $25,000 property damage.

How many points is a speeding ticket in Missouri?

Speeding tickets in Missouri typically result in 3 points on your license, but can vary based on speed and location.

Do permit drivers need insurance in Missouri?

Yes, permit drivers in Missouri must be covered by auto insurance, usually under a parent or guardian's policy.

How long does an insurance company have to pay a claim in Missouri?

Missouri law requires insurers to pay claims within 30 days after receiving proof of loss, unless further investigation is needed. For more information, read our article titled "When to File a Car Insurance Claim."

What happens in Missouri if you drive without insurance?

Driving without insurance in Missouri can result in license suspension, fines up to $500, and possible jail time for repeat offenses.

Our free online comparison tool below allows you to compare cheap car insurance quotes instantly — just enter your ZIP code to get started.