Best Indiana SR-22 Insurance in 2026 (Top 10 Companies Ranked)

Travelers, Liberty Mutual, and Geico stand out as the best Indiana SR-22 insurance providers. Rates start at $15 per month, and Travelers provides 24-hour BMV filing.

Liberty Mutual offers a 25% bundling discount, and Geico delivers basic SR-22 rates averaging 20% below competitors' rates. Indiana drivers need SR-22 insurance after serious violations like DUIs, penalties for driving without car insurance, or license suspensions. Proof of minimum liability coverage of $25,000/$50,000 for bodily injury and $25,000 for property damage is required.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 13% | A++ | Reliable Service | Travelers | |

| #2 | 25% | A | Coverage Options | Liberty Mutual | |

| #3 | 25% | A++ | Affordable Rates | Geico | |

| #4 | 17% | B | Customer Satisfaction | State Farm | |

| #5 | 10% | A++ | Military Support | USAA | |

| #6 | 20% | A | Innovative Discounts | Farmers | |

| #7 | 10% | A+ | Technological Innovation | Progressive | |

| #8 | 20% | A+ | Strong Reputation | Nationwide | |

| #9 | 25% | A+ | Financial Stability | Allstate | |

| #10 | 25% | A | Loyalty Rewards | American Family |

Still, drivers can reduce costs through discounts like multi-policy bundles, safe driver programs, and good student discounts. Shop for the best Indiana SR-22 insurance with our free quote comparison tool. Enter your ZIP code to begin.

What You Should Know

- Travelers lead Indiana SR-22 providers with 24-hour BMV filing

- Liberty Mutual offers the highest bundling discount at 25%

- Geico delivers affordable SR-22 coverage with rates averaging 20%

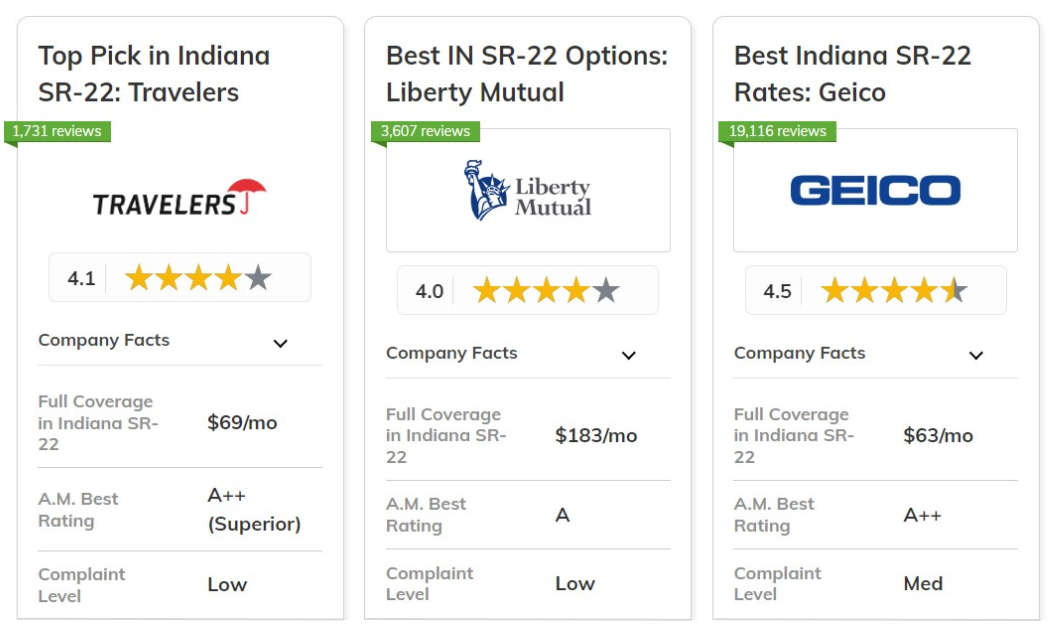

#1 - Travelers: Best for Reliable Service

Pros

- Fastest Filing Process: Offers industry-leading 24-hour SR-22 filing with Indiana BMV compared to standard 48-72 hour processing.

- Dedicated SR-22 Department: Maintains a specialized team of Indiana SR-22 experts for streamlined documentation and support.

- Competitive Filing Fees: Provides some of Indiana's lowest SR-22 filing fees at just $15, well below the state average of $ 25. Only offers quarterly and annual payment plans for Indiana SR-22 policies. Learn more in our Travelers car insurance review.

Cons

- Limited Payment Options: Only offers quarterly and annual payment plans for Indiana SR-22 policies.

- Higher Initial Premiums: Base rates for new Indiana SR-22 filings are 10% above the state average.

#2 - Liberty Mutual: Best for Coverage Options

Pros

- Flexible Coverage Plans: Offers Indiana's most customizable SR-22 policy options with unique add-ons.

- High Bundling Discount: Provides a maximum 25% discount when combining SR-22 auto with home insurance in Indiana.

- Violation Forgiveness: This unique program allows one minor violation in Indiana without a rate increase during SR-22. Read our car insurance review of Liberty Mutual for more details.

Cons

- Complex Application: Requires more extensive documentation than other Indiana SR-22 providers.

- SR-22 Strict Eligibility: Has more stringent qualification requirements for high-risk Indiana drivers.

#3 - Geico: Best for Affordable Rates

Pros

- Competitive Base Rates: Consistently offers Indiana's lowest minimum SR-22 coverage rates, averaging 20% below competitors.

- Easy Digital Management: Features the most user-friendly mobile app for SR-22 policy management and instant document access. Geico is one of the car insurance companies that customers recommend in Indiana.

- Military Savings: Provides special SR-22 rate reductions for Indiana's active duty and veteran drivers.

Cons

- Limited Local Support: Minimal physical offices in Indiana are available for in-person SR-22 assistance.

- Strict Renewal Criteria: More demanding requirements for SR-22 policy renewal than other providers in Indiana.

#4 - State Farm: Best for Customer Service

Pros

- Local Agent Network: The Largest local agents in Indiana provide personalized SR-22 assistance.

- Flexible Payments: Offers the most payment plan options for Indiana SR-22 policies, including monthly installments.

- Claims Support: Provides 24/7 dedicated claims service for Indiana SR-22 policyholders. Check out our State Farm car insurance review for more details.

Cons

- Higher Base Premiums: Initial SR-22 rates are typically 15% above Indiana's average.

- Strict Coverage Requirements in Indiana: More comprehensive SR-22 coverage requirements than minimum state standards.

#5 - USAA: Best for Military Members

Pros

- Military Expertise: Specialized understanding of military deployment impacts on Indiana SR-22 requirements.

- Deployment Protection: Unique coverage adjustments for Indiana active duty members with SR-22 filings.

- Family Discounts: Extended benefits for military family members in Indiana requiring SR-22 insurance. Read our USAA car insurance review for more information.

Cons

- Limited Eligibility in Indiana: SR-22 coverage is restricted to military members and their immediate families.

- Restricted Services: Fewer physical locations in Indiana are available for in-person SR-22 support.

#6 - Farmers: Best for Innovative Discounts

Pros

- Signal Program: Unique usage-based discount program for SR-22 drivers in Indiana to earn lower rates.

- Alternative Payment Options: Offers pay-per-mile options for low-mileage SR-22 drivers in Indiana.

- Multiple Discount Programs: The most extensive discount opportunities for Indiana SR-22 filers. See our Farmers car insurance review for additional details.

Cons

- Complex Discount Structure: Qualification requirements for discounts can be challenging to meet for Indiana SR-22 insurance policyholders.

- Higher Filing Fees in Indiana: Initial SR-22 filing fees above the state average.

#7 - Progressive: Best for Technology Integration

Pros

- Snapshot Program: Advanced telematics program offering unique discounts for Indiana-safe SR-22 drivers.

- Online Tools: Most comprehensive online quote comparison tool for Indiana SR-22 insurance.

- Digital Filing: Fastest electronic SR-22 filing system in Indiana. Learn more in our Progressive car insurance review.

Cons

- Variable Rates: Premiums can increase significantly based on Snapshot program results for Indiana SR-22 insurance drivers.

- Limited Agent Access: Fewer local agents in Indiana are available for in-person SR-22 insurance assistance.

#8 - Nationwide: Best for Strong Reputation

Pros

- Financial Stability: Highest financial strength ratings among Indiana SR-22 providers.

- Vanishing Deductible: This unique program reduces Indiana policyholders' deductibles for accident-free SR-22 periods.

- Accident Forgiveness: Available for SR-22 drivers in Indiana after the qualifying period. Read our Nationwide car insurance review for more details.

Cons

- Higher Initial Costs: Premium rates start higher than the state average for Indiana SR-22 policies.

- Strict Guidelines: More stringent requirements for policy maintenance for Indiana SR-22 policyholders.

#9 - Allstate: Best for Financial Stability

Pros

- Drivewise Program: Telematics program offering significant discounts for safe SR-22 drivers in Indiana.

- Claim Satisfaction: Guaranteed satisfaction with the Indiana SR-22 claims process or money back.

- Local Support: Extensive network of Indiana agents for SR-22 assistance. Check out our Allstate car insurance review for more information.

Cons

- Premium Costs: Higher than average rates for Indiana SR-22 coverage.

- Limited Online Options in Indiana: Less comprehensive digital services for SR-22 insurance than competitors.

#10 - American Family: Best for Loyalty Rewards

Pros

- KnowYourDrive: Usage-based program offering unique savings for SR-22 drivers in Indiana.

- Loyalty Discounts: Most generous long-term customer rewards for Indiana SR-22 policies.

- Diminishing Deductible: Reduces deductibles annually for safe Indiana SR-22 drivers. See our review of American Family car insurance for more details.

Cons

- Regional Limitations: SR-22 insurance is unavailable in some Indiana counties.

- Strict Qualification in Indiana: More demanding criteria for SR-22 insurance policy qualification.

SR-22 Insurance Rates in Indiana

After a license suspension, you must purchase SR-22 insurance in Indiana to show financial responsibility to the BMV. This insurance certificate must be kept up continuously and without lapses to reinstate your driving privileges.

Coverage periods last 3-5 years, depending on your violation, with costs averaging 71.5% more than standard insurance. Here are the current monthly rates for the best Indiana SR-22 insurance providers:

Coverage periods last 3-5 years, depending on your violation, with costs averaging 71.5% more than standard insurance. Here are the current monthly rates for the best Indiana SR-22 insurance providers:

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $48 | $140 | |

| $37 | $107 | |

| $27 | $79 | |

| $22 | $63 | |

| $63 | $183 | |

| $33 | $97 | |

| $24 | $69 | |

| $24 | $71 | |

| $24 | $69 | |

| $15 | $43 |

USAA charges the lowest rates, starting at $15 per month, but it is only available to military members. Geico has the lowest rates for general availability at $22 for minimum coverage, but Liberty Mutual is number one with the most comprehensive coverage options for higher rates. Compare quotes from multiple providers to find your best rate.

🔔 #SafeDrivingTip: Turning on your phone’s “do not disturb” function before you begin driving can help reduce the temptation to browse online at a red light or immediately respond to a text message.

— Travelers (@Travelers) October 19, 2023

Find more tips from the @NatlDDCoalition: https://t.co/iS4wx4sbQW #FocusOn pic.twitter.com/y0btT0vBOt

Understanding the statistics of SR-22 insurance in Indiana can help explain the cost of SR-22 insurance in Indiana. Here's a breakdown of claim types and their impact:

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Rear-End Collisions | 30% | $3,500 |

| Single-Vehicle Accidents | 25% | $4,200 |

| Intersection Accidents | 20% | $5,000 |

| Parked Vehicle Damage | 15% | $1,800 |

| Weather-Related Incidents | 10% | $6,500 |

Indiana SR-22 insurance rates will depend on your location. Take, for instance, Indianapolis because they have 15,000 accidents and 12,000 claims annually, so they usually have higher premiums. Here's how accidents and claims affect the cost of SR-22 insurance in Indiana across major cities:

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Carmel | 1,800 | 1,500 |

| Evansville | 3,500 | 2,800 |

| Fort Wayne | 5,000 | 4,000 |

| Indianapolis | 15,000 | 12,000 |

| South Bend | 2,500 | 2,000 |

These statistics explain why SR-22 insurance rates vary depending on where you live and your driving history. For example, SR-22 insurance in Indianapolis, IN, might cost more due to frequent accidents and claims in that city.

The SR-22 Insurance Limits in Indiana

Indiana SR-22 insurance requires minimum liability coverage of $25,000 for bodily injury or death per person, $50,000 for bodily injury or death per accident, and $25,000 for property damage coverage per accident. Here's a snapshot of factors affecting SR-22 insurance rates in Indiana, from vehicle theft to weather conditions:

| Category | Grade | Explanation |

|---|---|---|

| Vehicle Theft Rate | A- | Low theft occurrences |

| Average Claim Size | B+ | Below national average |

| Uninsured Drivers Rate | B+ | Slightly below average |

| Traffic Density | B | Moderate urban congestion |

| Weather-Related Risks | B | Moderate weather incidents |

These ratings help explain why Indiana maintains relatively moderate SR-22 insurance requirements of $25,000/$50,000 for bodily injury and $25,000 for property damage. The state's favorable risk factors help keep insurance costs manageable.

Lessen Your Indiana SR-22 Insurance Cost

When your license is suspended in Indiana, you'll need to pay reinstatement fees and potentially additional SR-22 filing fees. Here are the top insurance discounts available to help reduce your costs:

| Discount Name | Grade | Savings | Participating Providers |

|---|---|---|---|

| Multi-Policy | A | 25% | State Farm, Allstate, Progressive, Geico |

| Safe Driver | A- | 20% | State Farm, Allstate, Progressive, Geico |

| Good Student | B+ | 15% | State Farm, Allstate, Progressive, Geico |

| Low Mileage | B | 10% | State Farm, Allstate, Progressive, Geico |

| Anti-Theft Device | B- | 5% | State Farm, Allstate, Progressive, Geico |

While these costs can be significant, many insurance companies offer ways to save money on car insurance and tips for reducing your premiums. Here are the available discounts from top SR-22 insurance providers:

| Insurance Company | Available Discount |

|---|---|

| Multi-Policy, Safe Driver, Teen Safe Driver, Defensive Driving, Accident-Free Driver | |

| Multi-Policy, Safe Driver, Signal App, Homeowner, Good Student | |

| Multi-Policy, Defensive Driving, Good Student, Anti-Theft, Vehicle Equipment | |

| Multi-Policy, Military, Hybrid/electric Vehicle, Advanced Safety Features | |

| Multi-Policy, Defensive Driving, Smart Ride, Anti-Theft, Good Student | |

| Multi-Policy, Safe Driver, Snapshot App, Homeowner, Continuous Coverage | |

| Multi-Policy, Defensive Driving, Safe Vehicle, Steer Clear (for Young Drivers) | |

| Multi-Policy, Safe Driver, New Car, Good Student, Continuous Coverage | |

| Multi-Policy, Safe Driver, Military, Defensive Driving, New Vehicle | |

| Multi-Policy, Safe Driver, Teen Safe Driver, Defensive Driving |

Despite higher SR-22 insurance costs, multi-policy bundling, defensive driving courses, and usage-based insurance can still yield savings.

In addition, many providers offer unique discounts; for example, Geico provides hybrid vehicle savings, and State Farm provides a new car discount, so it's worth comparing several quotes.

Compare Best Indiana SR-22 Insurance Providers

Travelers, Liberty Mutual, and Geico stand out among Indiana's best SR-22 insurance providers. Travelers offer a quick 24-hour filing. Liberty Mutual gives a 25% discount for bundling and forgiveness for violations. For bundles, check out our best car & homeowners insurance to compare insurance bundles in your state.

Geico keeps its rates 20% lower than the others. In Indiana, SR-22 insurance costs are higher than regular coverage. However, you may find considerable savings if you compare quotes from different companies. Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

Frequently Asked Questions

What is SR-22 insurance in Indiana?

SR-22 insurance Indiana is not insurance, but a certificate filed with the Indiana BMV proving you maintain the state's minimum required auto liability coverage after certain driving violations. High-risk drivers are required to reinstate their license after suspension.

How much is SR-22 insurance in Indiana?

SR-22 insurance in Indiana costs an average of $131 monthly for drivers with one DUI, about 71.5% more than standard insurance. Monthly premiums range from $15-63 for minimum coverage and $43-183 for full coverage, depending on the provider.

Ready to find cheaper car insurance coverage? Enter your ZIP code to begin.

Who has the best SR-22 insurance in Indiana?

Travelers offer the best SR-22 insurance with 24-hour BMV filing and $15 filing fees. It is followed by Liberty Mutual, which offers a 25% bundling discount and violation forgiveness, and Geico, which has rates averaging 20% below competitors.

Read More: Ultimate Guide to Switching Car Insurance Companies to Save Money

How much is an SR-22 in Indiana?

The SR-22 filing fee in Indiana typically ranges from $15 to $25, with Travelers offering the lowest fee at $15. However, the total cost includes both the filing fee and increased insurance premiums for high-risk coverage.

Who needs SR-22 insurance in Indiana?

SR-22 insurance is required for drivers convicted of DUIs, driving without insurance, license suspension, multiple traffic violations, reckless driving, fatal accidents, or those failing to pay traffic fines.

Read More: DUI vs. DWI: What's The Difference?

Where to get the cheapest SR-22 insurance in Indiana?

USAA offers the cheapest SR-22 insurance, with a minimum coverage of $15 monthly, but it's limited to military members. For general availability, Geico provides the lowest rates, starting at $22 monthly.

Who carries SR-22 insurance in Indiana?

All major insurance providers in Indiana offer SR-22 filing, including Travelers, Liberty Mutual, Geico, State Farm, USAA, Farmers, Progressive, Nationwide, Allstate, and American Family.

How long do you need an SR-22 in Indiana?

Indiana requires SR-22 filing for either 3 years (first/second no-insurance suspension) or 5 years (third or subsequent suspension), depending on the violation.

Read More: What is SR-22 insurance?

Where is the cheapest place to get SR-22 insurance in Indiana?

Compare quotes online from multiple providers, starting with Geico ($22/month), Progressive ($24/month), and Travelers ($24/month) for minimum coverage. USAA offers military members the lowest rates ($15/month).

How much will an SR-22 increase my insurance?

An SR-22 filing typically increases insurance rates by 71.5% in Indiana. For example, after a DUI, rates increase from an average of $76 to $131 monthly.

Ready to shop around for the best car insurance company? Enter your ZIP code and see which offers the coverage you need.