Best Illinois SR-22 Insurance in 2026 (Check Out the Top 10 Companies)

The top picks for the best Illinois SR-22 insurance are Geico, Allstate, and Nationwide, with Geico offering the best overall rate at just $18 per month for flexible coverage.

Geico, Allstate, and Nationwide each offer standout benefits for SR-22 insurance in Illinois, with Geico known for affordable premiums, Allstate for customizable protection, and Nationwide for budget-friendly rates.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 25% | A | Flexible Coverage | Liberty Mutual | |

| #2 | 25% | A+ | Comprehensive Options | Allstate | |

| #3 | 20% | A+ | Affordable Rates | Nationwide | |

| #4 | 10% | A+ | Broad Discounts | Progressive | |

| #5 | 20% | A | Reliable Service | Farmers | |

| #6 | 10% | A++ | Military Focused | USAA | |

| #7 | 13% | A++ | Customizable Policies | Travelers | |

| #8 | 25% | A++ | Competitive Pricing | Geico | |

| #9 | 17% | B | Nationwide Coverage | State Farm | |

| #10 | 25% | A | Loyalty Rewards | American Family |

Comprehensive insurance coverage protects against non-collision damages, such as theft, vandalism, and natural disasters. Together, these providers make it easier for high-risk drivers to find the right coverage at the best possible price.

Enter your ZIP code above to get personalized insurance quotes tailored to your needs and budget

What You Should Know

- Geico stands out as the top pick for affordable SR-22 insurance at just $18 per month

- The best Illinois SR-22 insurance offers flexible coverage options tailored to individual needs

- Regularly comparing rates can help you secure the best Illinois SR-22 insurance

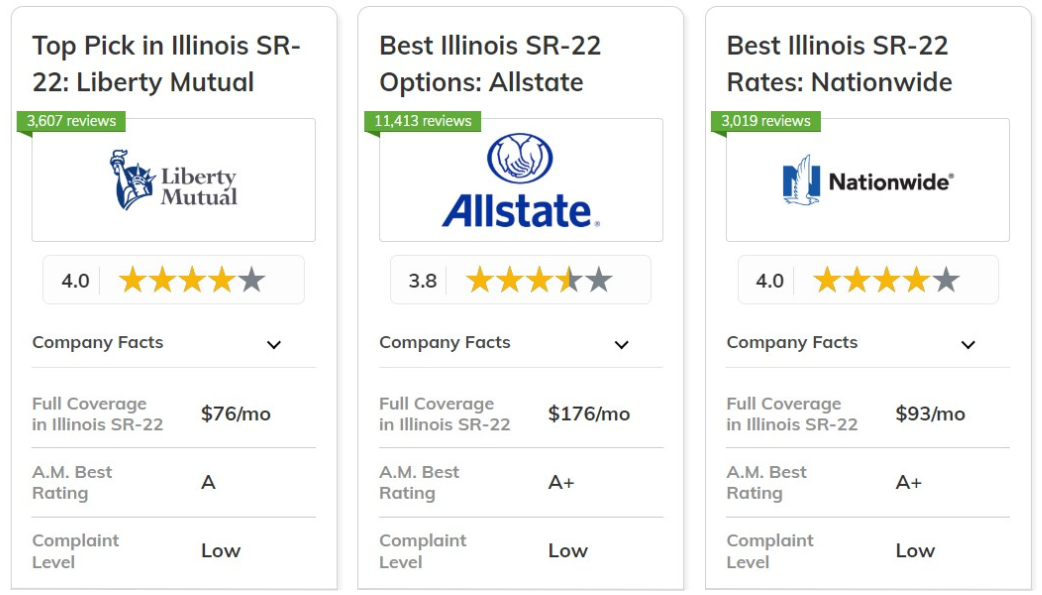

#1 – Liberty Mutual: Top Overall Pick

Pros

- Extensive Coverage Options: Discover our Liberty Mutual review for details on how the company provides comprehensive SR-22 coverage, making it one of the best Illinois SR-22 insurance providers for high-risk drivers.

- Discount Opportunities: The company provides various discounts, including multi-policy and safe driver discounts, helping reduce costs for the best Illinois SR-22 insurance.

- User-Friendly Claims Process: Liberty Mutual features an efficient claims handling process, ensuring quick resolutions for SR-22 insurance claims.

Cons

- **Higher Premiums: While Liberty Mutual offers quality coverage, some drivers may find their premiums higher compared to other options for the best Illinois SR-22 insurance.

- **Mixed Customer Service Reviews: Customer service experiences can vary, leading to inconsistent satisfaction among policyholders seeking the best Illinois SR-22 insurance.

#2 – Allstate: Best for Comprehensive Options

Pros

- Tailored Coverage: Allstate offers highly customizable SR-22 insurance options, allowing Illinois drivers to build policies that fit their exact needs, including additional protection like roadside assistance.

- Extensive Agent Network: With a large number of local agents throughout Illinois, Allstate provides hands-on support for SR-22 insurance, ensuring personal guidance through the entire process.

- Safe Driving Discounts: With our Allstate review, you'll learn how the company is known for fast and easy SR-22 filings for high-risk drivers in Illinois.

Cons

- Higher Premiums: Allstate’s comprehensive options come with higher costs, making it one of the pricier choices for SR-22 insurance in Illinois.

- Fewer Specific Discounts: While Allstate offers many discounts, specific savings for SR-22 policyholders are more limited compared to other providers.

#3 – Nationwide: Best for Affordable Rates

Pros

- Budget-Friendly SR-22 Coverage: In our Nationwide review, the company is known for offering competitive rates, helping Illinois drivers with SR-22 requirements keep their insurance premiums manageable.

- Accident Forgiveness: For drivers who may have minor infractions, Nationwide’s accident forgiveness prevents premiums from skyrocketing after a first-time accident.

- Multi-Policy Discounts: Bundling home, life, and auto insurance can lead to significant savings, making SR-22 coverage more affordable.

Cons

- Availability Restrictions: SR-22 insurance may not be offered in all regions of Illinois, limiting access to Nationwide’s competitive rates for some drivers.

- Fewer Local Agents: Nationwide’s presence in Illinois isn’t as expansive as competitors like State Farm, which could mean fewer in-person support options for SR-22 filings.

#4 – Progressive: Best for Broad Discounts

Pros

- Extensive Discount Options: Progressive offers one of the widest ranges of discounts for SR-22 insurance, including savings for bundling, good driving habits, and automatic payments.

- User-Friendly Mobile App: Based on our Progressive review, the company allows high-risk drivers to easily manage their SR-22 insurance through a top-rated mobile app, providing seamless access to their policy, claim filing, and tracking.

- Flexible Payment Plans: Progressive offers flexible payment options that can help spread out SR-22 insurance costs, making it easier for drivers to manage premiums.

Cons

- Varied Rates Based on Risk: While discounts are plentiful, SR-22 insurance premiums can fluctuate significantly based on driving history, making it less predictable for high-risk drivers.

- Inconsistent Customer Service: Some customers have reported mixed experiences with customer service, particularly during the claims process, which could affect SR-22 policyholders needing immediate help.

#5 – Farmers: Best for Reliable Service

Pros

- Exceptional Customer Support: Farmers is known for its excellent customer service, offering responsive and knowledgeable agents who are readily available to assist with SR-22 filings and policy updates.

- Comprehensive Coverage: Farmers offers a wide range of coverage options for SR-22 insurance, including optional add-ons like rental car coverage and towing, providing extra protection for Illinois drivers.

- Quick Claims Handling: View our Farmers review to learn more about how the company ensures a fast claims process for drivers with SR-22 insurance, allowing them to resolve incidents quickly and efficiently.

Cons

- Higher Premiums: Farmers is generally more expensive than some competitors, which could make SR-22 insurance unaffordable for drivers on a tight budget.

- Fewer SR-22 Discounts: Unlike other insurers, Farmers offers fewer discounts specifically for SR-22 policyholders, limiting potential savings.

#6 – USAA: Best for Military Focused

Pros

- Specialized for Military Members: USAA is tailored to the unique needs of military personnel and their families, providing exclusive benefits and affordable SR-22 insurance coverage for this group.

- Top-Rated Customer Service: Explore our USAA review to see how the company consistently ranks high for customer satisfaction, providing outstanding support throughout the SR-22 filing and maintenance process.

- Competitive Pricing for Military: USAA offers some of the lowest SR-22 insurance rates for eligible military drivers in Illinois, making it a great choice for service members.

Cons

- Eligibility Limitations: SR-22 insurance from USAA is only available to military members, veterans, and their families, excluding civilians from accessing these benefits.

- Limited SR-22 Coverage Options: USAA’s SR-22 offerings are fewer compared to other major providers, which may limit flexibility for some drivers.

#7 – Travelers: Best for Customizable Policies

Pros

- Highly Flexible Policies: Travelers offers a high degree of customization for SR-22 insurance, allowing Illinois drivers to choose coverage that best fits their personal needs and driving habits.

- Accident Forgiveness: This policy feature prevents premium increases after a first accident, making it ideal for drivers trying to maintain affordable SR-22 rates.

- Cost-Saving Discounts: See our Travelers review for insights on how the company offers significant multi-policy discounts for bundling SR-22 insurance with home or renters insurance, helping to lower overall costs.

Cons

- Limited SR-22 Availability: Not all Illinois locations provide SR-22 coverage, which may limit access to Travelers’ customizable plans.

- Higher Premiums for Customization: While the flexibility is valuable, the cost of SR-22 insurance through Travelers can be higher due to the extra features and custom options.

#8 – Geico: Best for Competitive Pricing

Pros

- Affordable Rates: Geico consistently offers some of the lowest premiums for SR-22 insurance, making it an ideal choice for drivers seeking cost-effective coverage.

- Efficient SR-22 Process: Geico provides a user-friendly online platform for quick SR-22 filings, allowing drivers to meet Illinois requirements swiftly. These tips we learned after filing a car insurance claim can also enhance your filing experience.

- Diverse Discount Programs: A variety of discounts, including those for good driving and vehicle safety features, can further reduce SR-22 insurance costs.

Cons

- Limited Agent Support: As an online-first provider, Geico lacks the in-person agent assistance that some drivers may prefer when dealing with SR-22 requirements.

- High Risk Premium Increases: Drivers with multiple violations or high-risk profiles may face significant premium hikes with SR-22 coverage.

#9 – State Farm: Best for Nationwide Coverage

Pros

- Widespread Agent Support: With an extensive network of agents across Illinois, State Farm offers strong in-person assistance for drivers handling SR-22 insurance requirements.

- Consistent SR-22 Rates: According to our State Farm review, the company is known for providing steady and dependable rates for SR-22 insurance in Illinois, allowing drivers to manage their budgets more effectively.

- Comprehensive Coverage Options: State Farm’s range of SR-22 coverage options ensures drivers can choose the best protection for their specific needs.

Cons

- Higher Premiums: State Farm’s SR-22 insurance may be more expensive for drivers with violations or higher-risk profiles.

- Few Discount Programs: Discounts specifically for SR-22 insurance are limited, reducing opportunities for drivers to save on their premiums.

#10 – American Family: Best for Loyalty Rewards

Pros

- Loyalty Discount Benefits: Delve into our American Family review to discover how the company provides loyalty rewards and discounts for long-term customers, helping to reduce SR-22 premiums over time.

- Personalized Agent Support: Drivers receive dedicated, hands-on support from local agents who can assist with SR-22 filings and policy management.

- Safe Driving Incentives: Drivers with a clean record can benefit from additional savings, lowering the cost of SR-22 insurance.

Cons

- High Premiums for Violations: Drivers with past violations or risky driving records may see higher rates for SR-22 insurance.

- Limited Customization Options: SR-22 insurance policies offer fewer custom options compared to competitors, which may restrict flexibility for some drivers.

Understanding SR-22 Insurance in Illinois

Finding the best Illinois SR-22 insurance is crucial for drivers needing to meet state requirements. This type of insurance provides proof of financial responsibility to reinstate your license.

- State Requirements: Illinois mandates SR-22 insurance for certain drivers, often following a suspension or DUI.

- Proof of Coverage: SR-22 is a form filed by your insurer, ensuring you meet minimum liability coverage.

- Higher Premiums: SR-22 policies often result in higher premiums, so comparing rates is essential.

Understanding the basics of SR-22 insurance is crucial when selecting the best Illinois SR-22 insurance provider. By grasping the requirements and implications of having an SR-22, you can make informed decisions tailored to your unique situation.

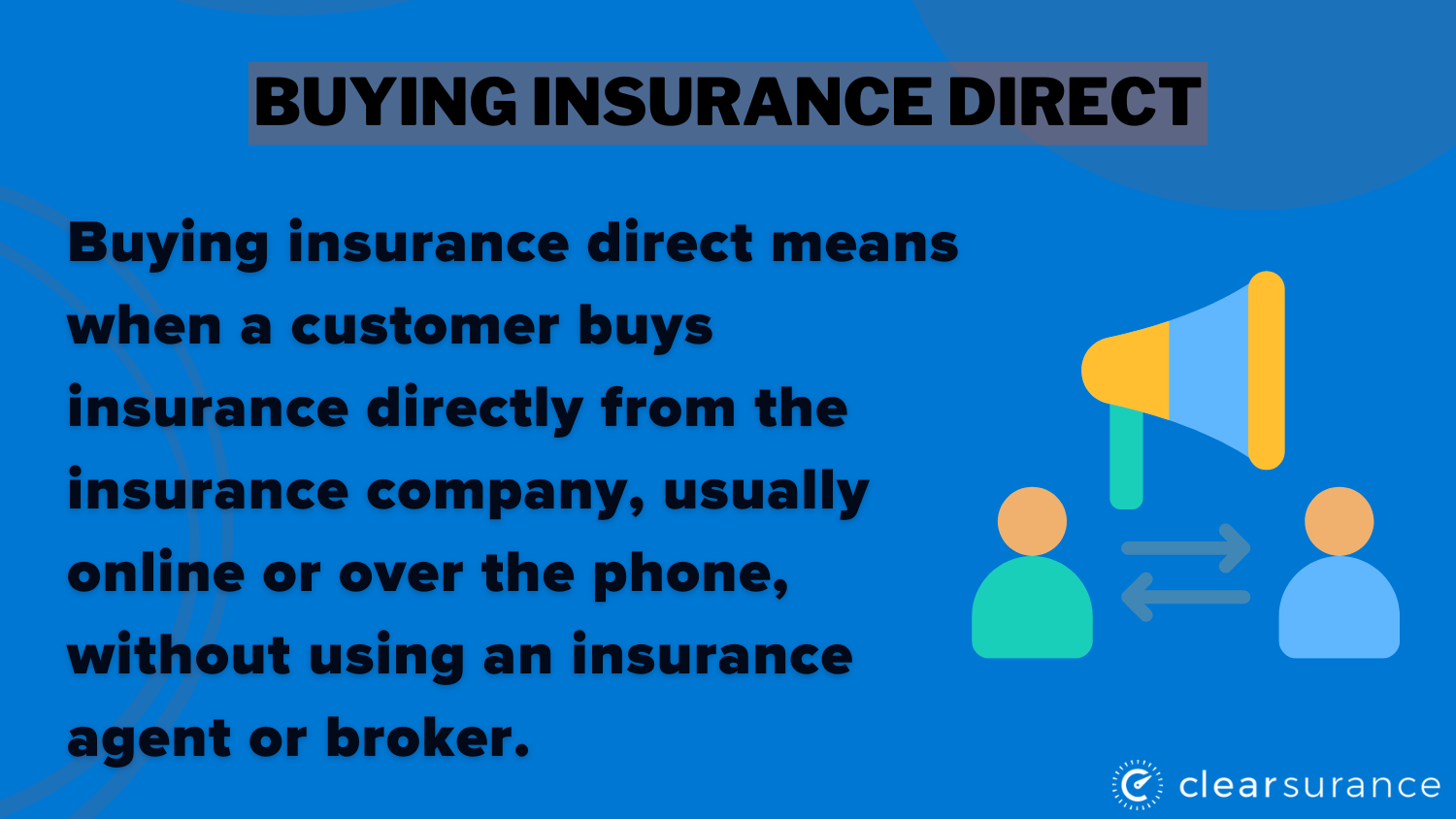

Additionally, consider buying insurance directly from providers, as this can often lead to more competitive rates and better customer service. Ensuring you meet all state requirements is essential to avoid further penalties and complications in the future.

Finding the Best Illinois SR-22 Insurance Providers

Finding the best Illinois SR-22 insurance providers can be a challenge, but focusing on specific criteria will make it easier. It's important to choose companies that offer competitive rates for high-risk drivers.

- Compare Providers: Look for insurers specializing in SR-22 policies to find the best Illinois SR-22 insurance rates.

- Look for Discounts: Some providers offer discounts even with SR-22 insurance, helping you save on premiums.

- Check Reviews: Customer reviews can help ensure you're picking a reliable insurer with expertise in SR-22 requirements.

Selecting the best Illinois SR-22 insurance providers requires careful comparison of coverage options. By reviewing premium rates and available discounts, you can find affordable solutions.

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $67 | $176 | |

| $43 | $114 | |

| $45 | $117 | |

| $18 | $47 | |

| $29 | $76 | |

| $35 | $93 | |

| $34 | $89 | |

| $25 | $64 | |

| $33 | $87 | |

| $24 | $62 |

Evaluating customer feedback also ensures reliable service. This approach helps you secure an SR-22 policy that meets your needs while staying within budget.

Tips for Lowering SR-22 Insurance Costs in Illinois

Even with SR-22 insurance, there are ways to lower your premiums. Implement these strategies to find the best Illinois SR-22 insurance without breaking the bank.

Maintaining a clean driving record post-SR-22 is essential, as it can lead to lower insurance rates over time. Additionally, bundling your SR-22 insurance with other policies, such as home or renters insurance, can help you save money through multi-policy discounts.

To broaden your understanding, explore our comprehensive resource on insurance coverage titled "Best and Cheapest Car Insurance in Illinois."

It's also crucial to regularly compare quotes from different insurers, as this practice can help you find more affordable SR-22 coverage. By implementing these strategies, you can effectively manage your SR-22 insurance costs.

| Insurance Company | Available Discount |

|---|---|

| Multi-policy, loyalty, early-bird, safe driver, good student, paperless billing, generational, young volunteer, anti-theft device, SR-22 | |

| Multi-policy, multi-car, safe driver, good student, homeowner, accident forgiveness, mature driver, ePolicy, SR-22 | |

| Multi-policy, good student, multi-car, defensive driving, military, anti-theft system, federal employee, accident-free, paperless billing, SR-22 | |

| Multi-policy, multi-car, safe driver, paperless billing, anti-theft device, homeowner, military, early shopper, hybrid/electric vehicle, accident-free, SR-22 | |

| Multi-policy, smart ride, anti-theft, defensive driving, accident-free, good student, paperless billing, automatic payments, SR-22 | |

| Multi-policy, multi-car, safe driver, continuous insurance, online quote, good student, paperless billing, homeowner, SR-22 | |

| Multi-policy, good driver, good student, accident-free, defensive driving, safe vehicle, homeownership, multi-car, SR-22 | |

| Multi-policy, homeownership, safe driver, new car, good student, continuous insurance, hybrid/electric vehicle, paperless billing, SR-22 | |

| Multi-policy, military, safe driver, good student, defensive driving, multi-vehicle, loyalty, SR-22 (only for military families) | |

| Multi-policy, homeownership, safe driver, new car, good student, continuous insurance, hybrid/electric vehicle |

Over time, your safe driving habits and proactive approach to policy management can lead to significant savings. Ultimately, staying informed and vigilant is key to securing the best rates available.

By applying these tips, you can significantly reduce the cost of your SR-22 insurance and ease the financial burden it often brings. It’s crucial to compare providers frequently to ensure you’re consistently getting the best Illinois SR-22 insurance available in the market.

This ongoing evaluation allows you to identify any changes in rates or coverage that can benefit you. Ultimately, staying proactive in your search will help you find a policy that offers both affordability and adequate protection.

Factors That Affect Illinois SR-22 Insurance Rates

Understanding the factors that influence Illinois SR-22 insurance rates is crucial for securing the best Illinois SR-22 insurance coverage. These factors can vary significantly between providers and can impact your overall premium costs.

- Driving History: Your driving record plays a major role in determining your insurance rates, as a clean record generally results in lower premiums.

- Type of Vehicle: The make and model of your vehicle can affect your rates; high-performance or luxury cars often lead to higher premiums due to increased risk.

- Coverage Levels: The amount of coverage you choose can also impact your rates; opting for higher limits or additional coverage can raise your premium costs.

Considering these factors can help you make informed decisions when shopping for the best Illinois SR-22 insurance. By understanding how your driving history, vehicle type, and coverage levels influence your rates, you can tailor your choices to find the most affordable options.

Additionally, being aware of these elements allows you to negotiate effectively with insurance providers. Ultimately, addressing these factors will position you for lower rates and more favorable insurance options that meet your specific needs.

Illinois SR-22 Insurance Rates Calculation

SR-22 insurance is for high-risk or non-standard driver. To account for your higher risk, the insurer charges you high premiums. However, the rates for SR-22 insurance are not the same across all insurers in Illinois. You can shop around for the best policies before you sign up for one. Remember that many factors impact the cost of this insurance, so what you can find may not match what your spouse or neighbor gets. Some factors that affect the cost of SR-22 coverage are your age, gender, marital status, location, the reason for the SR-22 requirement, the type of vehicle you drive, and so on.

One of the most common reasons drivers need SR-22 insurance is because of a DUI conviction. On average, drivers with one DUI conviction in Illinois pay $1,570 per year for car insurance. That’s 55 % more than car insurance for a driver with a clean driving record. However, the insurance cost you pay differs significantly based on the company you buy car insurance from. In the table below, you can find average rates for Illinois drivers who have one DUI conviction from some of the largest companies in the state.

| Company | Car insurance rate |

|---|---|

| Safeco | $894 |

| Geico | $1,104 |

| Erie | $1,137 |

| State Farm | $1,210 |

| Auto-Owners | $1,229 |

| USAA* | $1,258 |

| Country Financial | $1,318 |

| Travelers | $1,324 |

| Farmers | $1,470 |

| Progressive | $1,683 |

| Nationwide | $1,719 |

| Cincinnati Insurance Company | $2,048 |

| AAA | $2,088 |

| American Family | $2,094 |

| Allstate | $2,403 |

*USAA is only available to active and former military members and their families.

These rates are based on a 35-year-old single adult with one driver and one vehicle on a policy. The car used was a 2015 Toyota Highlander LEs. Full coverage was used with 100/300/50 limits and a $500 collision and comprehensive deductible. The driver had 1 DUI on their record. The rates displayed should only be used for comparative purposes as individual rates for high-risk insurance in Illinois will differ. Rate data is provided by Quadrant Information Services.

Stop overpaying for your insurance by entering your ZIP code below to find the lowest rates in your area.

Frequently Asked Questions

What is the best car insurance for obtaining an SR-22 in Illinois?

The best Illinois SR-22 insurance providers typically include companies known for their competitive rates and good customer service, such as Geico, Allstate, and Nationwide.

Do I need an SR-22 to reinstate my license in Illinois?

Yes, if your license was suspended due to certain violations, you typically need to file an SR-22 to reinstate it.

Does an SR-22 cover any car I drive in Illinois?

Yes, an SR-22 is a certificate that proves you have the required liability insurance, but you must have coverage for each vehicle you drive.

How do I check the status of my SR-22 in Illinois?

You can check the status of your SR-22 by contacting your insurance provider or the Illinois Secretary of State's office.

How long is an SR-22 required in Illinois?

An SR-22 is generally required for a minimum of three years in Illinois, depending on the severity of the offense.

How much does SR-22 insurance cost in Illinois per month?

On average, SR-22 insurance in Illinois can cost anywhere from $30 to $100 per month, depending on various factors like your driving record and the insurance provider.

How do I get an SR-22 removed in Illinois?

To get an SR-22 removed, you need to complete the required period of coverage and request your insurance provider to cancel the SR-22 filing.

Can you own a car without insurance in Illinois?

No, Illinois law requires all vehicle owners to have at least minimum liability insurance coverage to legally operate a vehicle.

What is the minimum full coverage car insurance in Illinois?

Illinois law requires drivers to carry minimum liability coverage of $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $20,000 for property damage.

Why is car insurance more expensive in Illinois compared to other states?

Factors contributing to higher car insurance rates in Illinois include urban traffic, higher rates of accidents, and state-specific regulations impacting coverage costs.