Best Iowa SR-22 Insurance in 2026 (See the Top 10 Companies Here!)

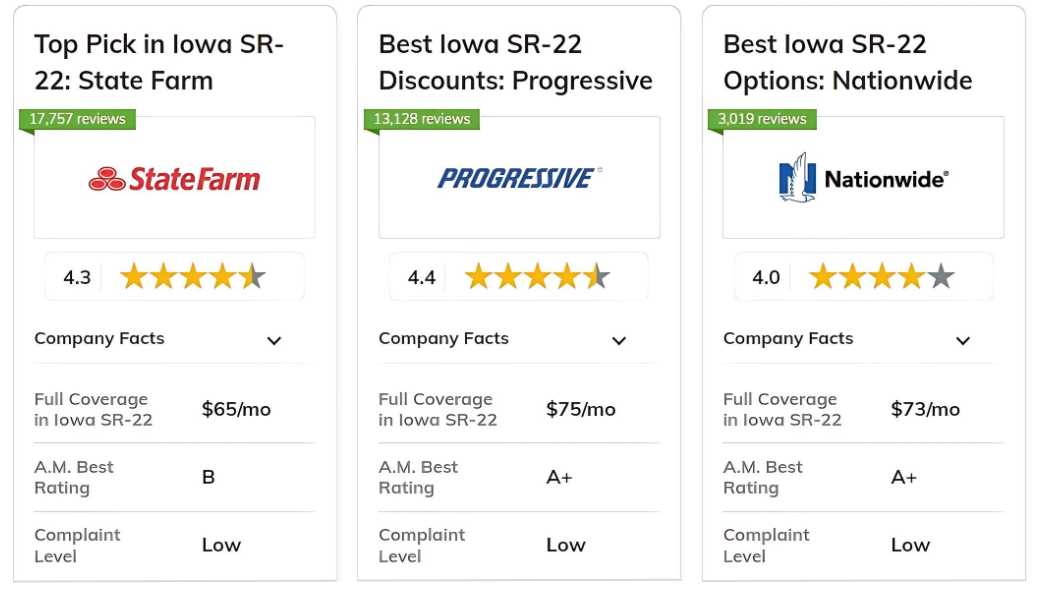

The best Iowa SR-22 insurance providers are State Farm, Progressive, and Nationwide, offering affordable rates and reliable coverage for high-risk drivers.

State Farm stands out with rates starting at $13 per month, while Progressive and Nationwide provide competitive pricing with flexible coverage options.

| Company | Rank | UBI Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 30% | B | Reliable Coverage | State Farm | |

| #2 | 30% | A+ | Innovative Discounts | Progressive | |

| #3 | 40% | A+ | Deductible Options | Nationwide | |

| #4 | 25% | A++ | Affordable Premiums | Geico | |

| #5 | 30% | A | Comprehensive Options | Farmers | |

| #6 | 30% | A++ | Military Friendly | USAA | |

| #7 | 30% | A | Customer Satisfaction | American Family | |

| #8 | 30% | A++ | Flexible Policies | Travelers | |

| #9 | 30% | A | Strong Financials | Liberty Mutual | |

| #10 | 30% | A+ | Excellent Service | Allstate |

Each offers innovative discounts and helps drivers maintain compliance with Iowa's SR-22 requirements. These companies are top picks for balancing cost and quality.

See if you’re getting the best deal on car insurance by entering your ZIP code above.

What You Should Know

- State Farm offers the best Iowa SR-22 insurance with rates starting at $13/month

- Get affordable coverage to meet Iowa SR-22 requirements for high-risk drivers

- Find the best Iowa SR-22 insurance with flexible options and reliable service

#1 – State Farm: Best for Reliable Coverage

Pros

- Dependable SR-22 Compliance: State Farm provides reliable SR-22 insurance that ensures compliance with Iowa’s legal requirements.

- Strong Customer Support: The company is known for its effective customer service, particularly in managing high-risk driver policies.

- Variety of Discounts: According to our State Farm review, the company offers discounts that can help reduce costs for loyal SR-22 insurance policyholders.

Cons

- Potential Rate Increases: Iowa SR-22 insurance premiums can be higher for drivers with severe violations.

- Limited Customization Options: Fewer options to adjust SR-22 policies compared to other providers.

#2 – Progressive: Best for Innovative Discounts

Pros

- Wide Range of Discounts: Progressive offers several innovative discounts that help lower Iowa SR-22 insurance.

- User-Friendly Online Platform: Easily manage your Iowa SR-22 insurance filings through their streamlined online system.

- Flexible Coverage Options: Based on our Progressive review, the company allows high-risk drivers to tailor their SR-22 coverage to their specific needs.

Cons

- Higher Rates for Some Drivers: Drivers with multiple violations may experience significantly higher premiums.

- Mixed Claims Experience: Some customers report delays in the claims process, particularly for Iowa SR-22 filings.

#3 – Nationwide: Best for Deductible Options

Pros

- Customizable Deductible Plans: Nationwide offers flexible deductible options to help manage the costs of Iowa SR-22 insurance.

- Efficient SR-22 Filing Process: In our Nationwide review, the company is known for quick and smooth SR-22 filings for high-risk drivers.

- Strong Financial Stability: Provides confidence for policyholders in Iowa needing long-term SR-22 coverage.

Cons

- Higher Premiums for High-Risk Drivers: Iowa SR-22 insurance may come at a higher cost for drivers with severe violations.

- Limited Discount Availability: Fewer discount opportunities compared to some competitors for SR-22 policies.

#4 – Geico: Best for Affordable Premiums

Pros

- Competitive Pricing: Geico offers some of the most affordable SR-22 insurance premiums in Iowa.

- Easy Online Tools: Provides easy-to-use digital tools for managing SR-22 filings and payments.

- Quick Filing: Known for fast and efficient SR-22 filings to meet Iowa requirements, these tips we learned after filing a car insurance claim can also help streamline the process and improve your experience.

Cons

- Basic Coverage Options: SR-22 coverage options may be more limited compared to other providers.

- Claims Process Issues: Some customers report delays in the claims process for Iowa SR-22 insurance.

#5 – Farmers: Best for Comprehensive Options

Pros

- Comprehensive SR-22 Coverage: Farmers offers a wide range of coverage options, ensuring compliance with Iowa’s SR-22 requirements.

- Excellent Customer Service: Known for responsive customer service and support for high-risk drivers.

- Discount Opportunities: View our Farmers review to learn more about how the company offers several discounts for long-term policyholders with Iowa SR-22 insurance.

Cons

- Higher Premiums: Iowa SR-22 insurance with Farmers may come at a higher cost for certain drivers.

- Limited Availability: Some discounts may not apply to SR-22 policyholders in Iowa.

#6 – USAA: Best for Military Friendly

Pros

- Exclusive to Military Members: Offers Iowa SR-22 insurance tailored specifically for military personnel and their families.

- Strong Customer Satisfaction: Known for exceptional customer service and support for SR-22 filings.

- Affordable Rates for Military Drivers: Explore our USAA review to see how the company provides competitive SR-22 rates for Iowa’s military members.

Cons

- Limited Eligibility: Only available to military personnel, limiting access for other high-risk drivers.

- Higher Rates for Non-Active Members: Rates for inactive military members may be higher compared to active members.

#7 – American Family: Best for Customer Satisfaction

Pros

- High Customer Satisfaction: American Family is highly rated for its customer service and handling of SR-22 filings.

- Customizable Coverage: Delve into our American Family review to discover how the company offers flexible SR-22 coverage options to meet Iowa’s legal requirements.

- Good Discount Opportunities: Several discount options can help reduce costs for SR-22 policyholders.

Cons

- Higher Rates for High-Risk Drivers: Iowa SR-22 insurance may come with higher premiums for drivers with multiple violations.

- Limited Online Tools: Less comprehensive digital tools for managing SR-22 policies compared to competitors.

#8 – Travelers: Best for Flexible Policies

Pros

- Flexible Coverage Options: Travelers offers customizable SR-22 insurance policies to meet Iowa’s unique needs.

- Efficient Claims Process: See our Travelers review for insights on how the company is known for its smooth and quick claims handling for Iowa SR-22 insurance.

- Good Discounts for Safe Drivers: Offers discounts that help reduce premiums for SR-22 policyholders with improved driving records.

Cons

- Higher Costs for Some Drivers: Premiums may be higher for drivers with serious violations or extensive claims history.

- Less User-Friendly Online Platform: Some customers report challenges with managing SR-22 policies online.

#9 – Liberty Mutual: Best for Strong Financials

Pros

- Strong Financial Standing: Liberty Mutual offers financial stability, ensuring long-term support for SR-22 policyholders.

- Wide Range of Discounts: Discover our Liberty Mutual review for details on how the company provides several discounts to help reduce SR-22 insurance costs in Iowa.

- Reliable Coverage Options: Offers dependable SR-22 coverage that meets Iowa’s legal requirements.

Cons

- Complex Claims Process: Some customers report challenges with the claims process, which may delay SR-22 filings.

- Limited Discounts for High-Risk Drivers: Some discounts may not be available for drivers requiring SR-22 insurance.

#10 – Allstate: Best for Excellent Service

Pros

- Exceptional Customer Service: Allstate is well-regarded for its customer support, particularly for SR-22 policyholders.

- Comprehensive SR-22 Coverage: Offers a wide range of SR-22 coverage options to comply with Iowa’s requirements.

- Efficient SR-22 Filings: With our Allstate review, you'll learn how the company is known for fast and easy SR-22 filings for high-risk drivers in Iowa.

Cons

- Higher Premiums for High-Risk Drivers: SR-22 insurance may come with higher costs compared to other providers.

- Limited Discount Options: Fewer discounts available for SR-22 policyholders than with some competitors.

Affordable Iowa SR-22 Insurance: Compare Top Provider Rates

If you're looking for the best Iowa SR-22 insurance, providers like State Farm, USAA, and Nationwide offer competitive rates. With minimum coverage starting as low as $13/month, you can find affordable options to meet Iowa's SR-22 requirements.

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $31 | $126 | |

| $23 | $95 | |

| $20 | $82 | |

| $20 | $81 | |

| $28 | $116 | |

| $18 | $73 | |

| $18 | $75 | |

| $16 | $65 | |

| $23 | $92 | |

| $13 | $55 |

Finding the right SR-22 insurance in Iowa can be simple. By comparing rates from leading providers, you can secure affordable coverage, fulfill state requirements, and stay protected on the road. It's also important to consider comprehensive insurance coverage to ensure broader protection in your policy.

Maximize Discounts on Iowa SR-22 Insurance

This table highlights the available discounts offered by top Iowa SR-22 insurance providers. Each company provides a variety of discounts, such as multi-policy, safe driver, and good student, allowing high-risk drivers to save on their SR-22 insurance premiums.

| Insurance Company | Available Discount |

|---|---|

| Multi-Policy, Safe Driver, Good Student, Homeowner | |

| Multi-Policy, Good Student, Homeowner, Safe Driver | |

| Good Driver, Multi-Car, Military, Federal Employee | |

| Multi-Policy, Safe Driver, Homeowner, Early Signing | |

| Multi-Policy, Safe Driver, Good Student, Early Signing | |

| Snapshot, Multi-Policy, Continuous Insurance, Homeowner | |

| Safe Driver, Multi-Policy, Good Student, Defensive Driving | |

| Multi-Policy, Safe Driver, Good Student, Claim-Free | |

| Multi-Policy, Good Student, Safe Driver, Military | |

| Multi-Policy, Safe Driver, Good Student |

Maximizing discounts is an effective strategy to save on Iowa SR-22 insurance. Understanding how credit scores affect insurance premiums can help you find better rates. Compare the offerings from top providers to secure the best deal and meet your SR-22 requirements at a lower cost.

5 Most Common Auto Insurance Claims in Iowa

The table outlines the five most common auto insurance claims in Iowa, highlighting both the frequency and cost of each claim type. Rear-end collisions lead with 30% of total claims, averaging a cost of $3,000 per incident. Weather-related damage, representing 25% of claims, shows the highest financial impact at $5,500 each.

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Rear-end Collisions | 30% | $3,000 |

| Weather-related Damage | 25% | $5,500 |

| Side-impact Collisions | 20% | $4,200 |

| Single-vehicle Accidents | 15% | $3,800 |

| Theft/Vandalism | 10% | $2,500 |

Side-impact collisions make up 20% of insurance claims, averaging $4,200 each, while single-vehicle accidents account for 15% with an average cost of $3,800 per claim. Theft and vandalism occur less frequently at 10%, but each incident costs around $2,500. Knowing when to file a car insurance claim in these situations offers valuable insights for both insurers and policyholders in Iowa, highlighting common risks and potential financial impacts.

Iowa Accidents & Claims per Year by City

The table provides an overview of auto accidents and insurance claims per year across various cities in Iowa. Des Moines records the highest number of accidents annually at 1,200, with corresponding claims reaching 800. Cedar Rapids, despite having 900 accidents, sees a relatively lower number of claims at 600.

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Cedar Rapids | 900 | 600 |

| Davenport | 750 | 550 |

| Des Moines | 1200 | 800 |

| Iowa City | 500 | 300 |

| Sioux City | 650 | 400 |

Davenport reports 750 accidents and 550 claims. Iowa City, with 500 accidents, has a lower claim rate of 300 per year. Sioux City sees 650 accidents and 400 claims annually. These variations in claim rates reflect differences in driving conditions, reporting practices, or the steps to take after a car accident, which can impact how quickly claims are filed and processed.

Iowa Report Card: Auto Insurance Discounts

The table outlines various auto insurance discounts available in Iowa, ranking them by value and listing participating insurers. Top-rated discounts, such as Multi-Vehicle and Safe Driver, offer savings of 20% and 15%, respectively, with companies like State Farm, Nationwide, and Geico. These discounts are key for those seeking tips on how to get cheap car insurance in the state.

| Discount Name | Grade | Savings | Participating Providers |

|---|---|---|---|

| Multi-Vehicle | A | 20% | State Farm, Nationwide, Farmers |

| Safe Driver | A | 15% | Allstate, Progressive, Geico |

| Low Mileage | C+ | 7% | Allstate, American Family, Liberty |

| Good Student | B+ | 10% | Progressive, Liberty Mutual, AAA |

| Anti-theft Device | B | 5% | Farmers, USAA, State Farm |

A Good Student discount also provides substantial benefits with a 10% savings through companies such as Progressive and Liberty Mutual. Conversely, Low Mileage and Anti-theft Device discounts offer lower savings of 7% and 5%, with participation from insurers like Allstate, American Family, and USAA, respectively. This guide helps Iowa drivers understand which discounts can maximize their insurance savings.

Iowa Report Card: Auto Insurance Premiums

The table grades various auto insurance premiums in Iowa, highlighting cost comparisons with regional and national averages. Full Coverage receives an 'A' for competitive rates, while Liability Coverage is rated 'B+' for being slightly above average.

| Category | Grade | Explanation |

|---|---|---|

| Full Coverage | A | Competitive Rates for Full Coverage Options |

| Liability Coverage | B+ | Slightly Above Average for Liability Costs |

| Comprehensive | B | Average Cost Compared to Neighboring States |

| Collision | C+ | Higher Than National Average |

| Uninsured Motorist | C | Premiums Significantly Higher |

Comprehensive coverage, rated 'B', aligns with costs in neighboring states. Collision coverage earns a 'C+' due to above-average costs, while uninsured motorist coverage receives a 'C' for significantly higher premiums.

This evaluation reflects the top ways customers have saved money on car insurance rates by comparing coverage options in Iowa.

Iowa SR-22 Insurance Requirements

In Iowa, an SR-22 form is necessary if you've been mandated by the state or a court to prove financial responsibility due to a driving violation. This form, filed by your insurer, confirms you meet the state's minimum vehicle liability insurance requirements. Often required for high-risk drivers, SR-22 can lead insurers to increase premiums or refuse coverage.

Non-vehicle owners must obtain a non-owner SR-22 policy to cover driving a rented or borrowed car. Typically, after a DUI, SR-22 insurance costs about 50% more than standard policies because it confirms adherence to minimum liability coverage following serious offenses. The cost varies based on the filing fee, violation severity, and lost discounts, urging a comparison of rates for affordability.

The filing requirement typically lasts three years, during which premiums remain elevated. Maintaining continuous coverage and a clean record can lead to lower rates after this period. A lapse or cancellation prompts your insurer to file an SR-26 form with the Iowa DOT, possibly resulting in license suspension or penalties. For more details, refer to a practical guide for understanding car insurance to navigate these requirements effectively.

Understanding SR-22 Insurance Limits in Iowa

If you’re required to have SR-22 insurance in Iowa, you’ll be required to have at least the following auto insurance coverage:

- Bodily injury liability — $20,000 per person

- Bodily injury liability — $40,000 per accident

- Property damage liability — $15,000 per accident

Meeting these minimum coverage limits ensures compliance with Iowa's SR-22 requirements, helping you maintain driving privileges and stay protected. It’s also important to understand how much bodily injury liability coverage you need to fully meet state regulations and safeguard yourself on the road.

Key SR-22 Insurance Requirements for Iowa Drivers

In Iowa, what is SR-22 insurance comes into play in certain situations where you need it to get your license reinstated. SR-22 is typically required after committing specific legal violations, and it may also be necessary if you’ve accumulated multiple minor offenses in a short period.

Violations requiring an SR-22 vary from state to state. Drivers in Iowa could need SR22 insurance for the following reasons:

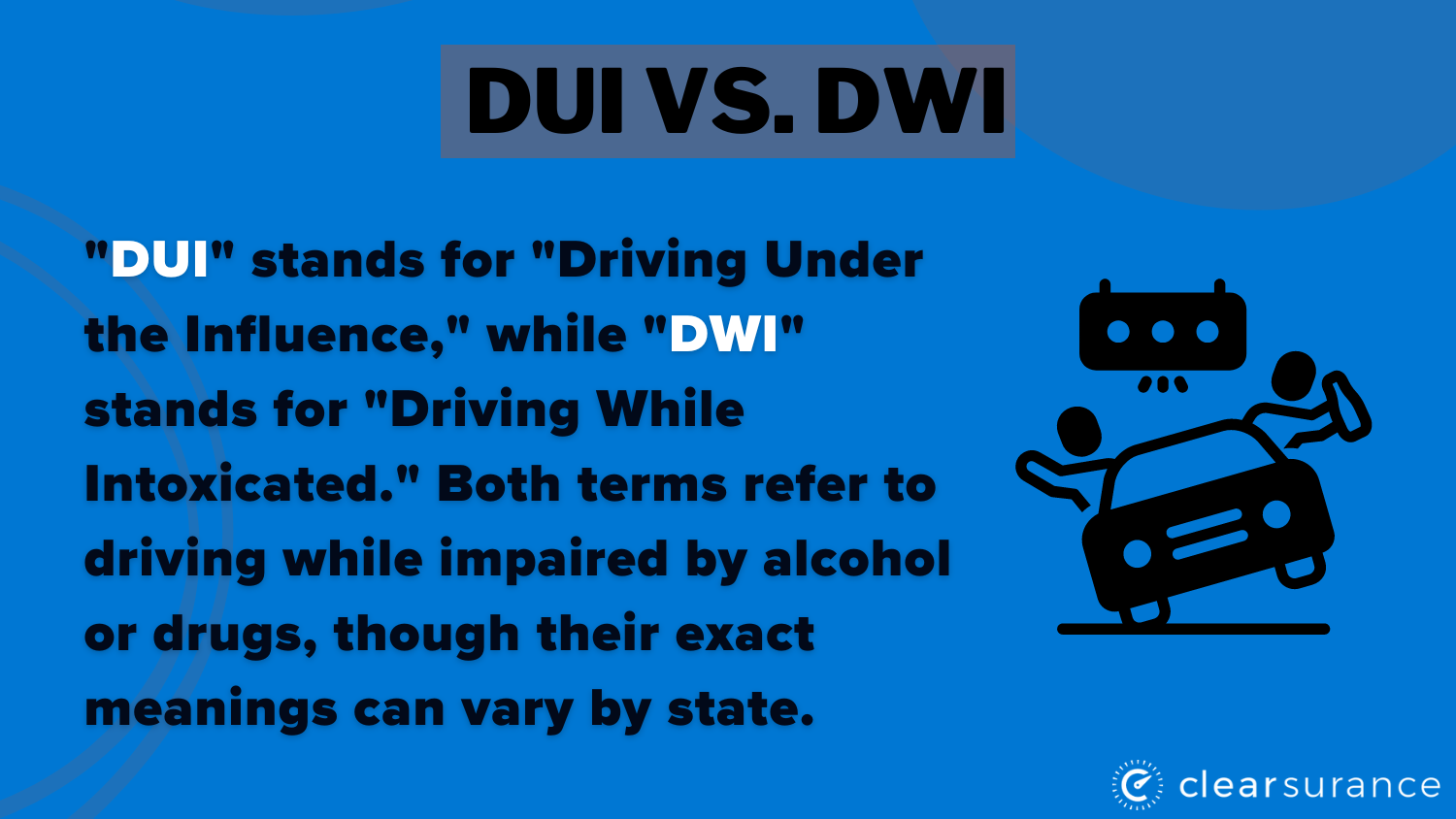

- Operating While Intoxicated (OWI) or refusal to take a breathalyzer/urine test

- Reckless driving or legal judgments from serious traffic offenses

- Uninsured vehicle accidents or driving without insurance

- Accumulation of excessive points due to multiple offenses

- Child support or neglect cases involving legal action

Violating the drunk driving laws is a serious offense requiring the driver to carry an SR-22 in Iowa. According to the Implied Consent Laws, refusal to undergo a chemical breath, blood or urine alcohol test results in the immediate suspension of your driver's license. Minor violations usually do not require SR-22 insurance in Iowa.

Iowa SR-22 Insurance: How Rates Are Determined

If you need SR-22 insurance in Iowa, you are considered a high-risk or non-standard driver. High-risk drivers that need SR22 insurance tend to pay the highest car insurance rates. The insurance cost increase is triggered by the violation that made the SR-22 necessary. The cost of car insurance can vary by company and there are many other factors that go into the cost of SR-22 insurance such as your age, gender, location, credit score, motor vehicle type, marital status and so on.

One of the primary reasons drivers require SR-22 insurance is due to a DUI and DWI conviction. In Iowa, drivers with a single DUI conviction pay an average of $1,248 per year for car insurance, which is 50% higher than rates for drivers with a clean record.

However, the actual cost can vary significantly depending on the insurance provider. The table below shows average rates for Iowa drivers with a DUI conviction from some of the largest companies in the state.

Steps to Obtain SR-22 Insurance in Iowa

The first step to get SR-22 insurance is to find an insurer. An SR-22 must be filed through a car insurance provider. You can’t complete it on your own. Several insurance companies offer SR-22 insurance in Iowa. You can start by talking to your insurance company to see if it offers SR-22 insurance. It may be a good idea to shop around for SR-22 insurance even if your car insurance company provides it. The insurance rates vary from company to company.

Use the table at the top of this page to find all the car insurance companies that offer SR-22 insurance in Iowa with a minimum of 25 reviews. If you want to see which companies customers say are the best car insurance companies for SR-22 insurance in Iowa, sort the table by highest rated. You can sort through companies and find the ones you want to get quotes from. To get quotes, click on the orange "Click for quote" button next to the company, call the number available, or visit the company's website.

To view customer reviews of a company, simply click the company name in the table, and you’ll be taken to its profile page, which includes detailed information and reviews. This can help you evaluate the best car insurance in Iowa based on real customer experiences.

Alternative Options to SR-22 Insurance in Iowa

There is an alternative to obtaining SR-22 insurance in Iowa, though it's less common as it requires setting aside a substantial sum. You can deposit $55,000 as a surety bond, cash, or securities to cover any damages in the event of an accident. Also, understanding how long after a car accident you can file a claim is essential if you choose this route, as it impacts your ability to access funds for damage coverage.

SR-22 Filing Fees and Costs in Iowa

Filing for an SR-22 in Iowa indicates that you've violated specific driving laws. To reinstate your license, you must provide proof of financial responsibility. In Iowa, SR-22 insurance tends to be costly, as violations raise car insurance premiums. Maintaining a clean driving record can help reduce these costs over time.

The SR-22 insurance rates and premium depend on the offense, but the fees for filing in Iowa is typically between $15 to $35. Further, you’re required to pay another $10 as a license fee for a duplicate license. On completion of the period of revocation, you’ll be required to pay a license reinstatement fee, which varies based on your violation.

An OWI (commonly referred to as a DUI in most states) is one of the most common reasons for needing SR22 insurance and it’s a very costly conviction. There are many penalties for an OWI in Iowa including license suspension or revocation. When you’re able to get your license reinstated after an OWI, you’ll have to pay a civil penalty of $200.

Factors Affecting SR-22 Insurance Rates

When comparing SR-22 insurance rates in Iowa, it can be challenging to understand the various factors that affect the cost. Each insurance company uses different criteria, but several key elements contribute to the price you pay:

- Your driving record, including any violations requiring an SR-22

- Location and its accident history, impacting overall rates

- How much you drive and the type of vehicle you own

- Age, marital status, and gender, which insurers consider when calculating risk

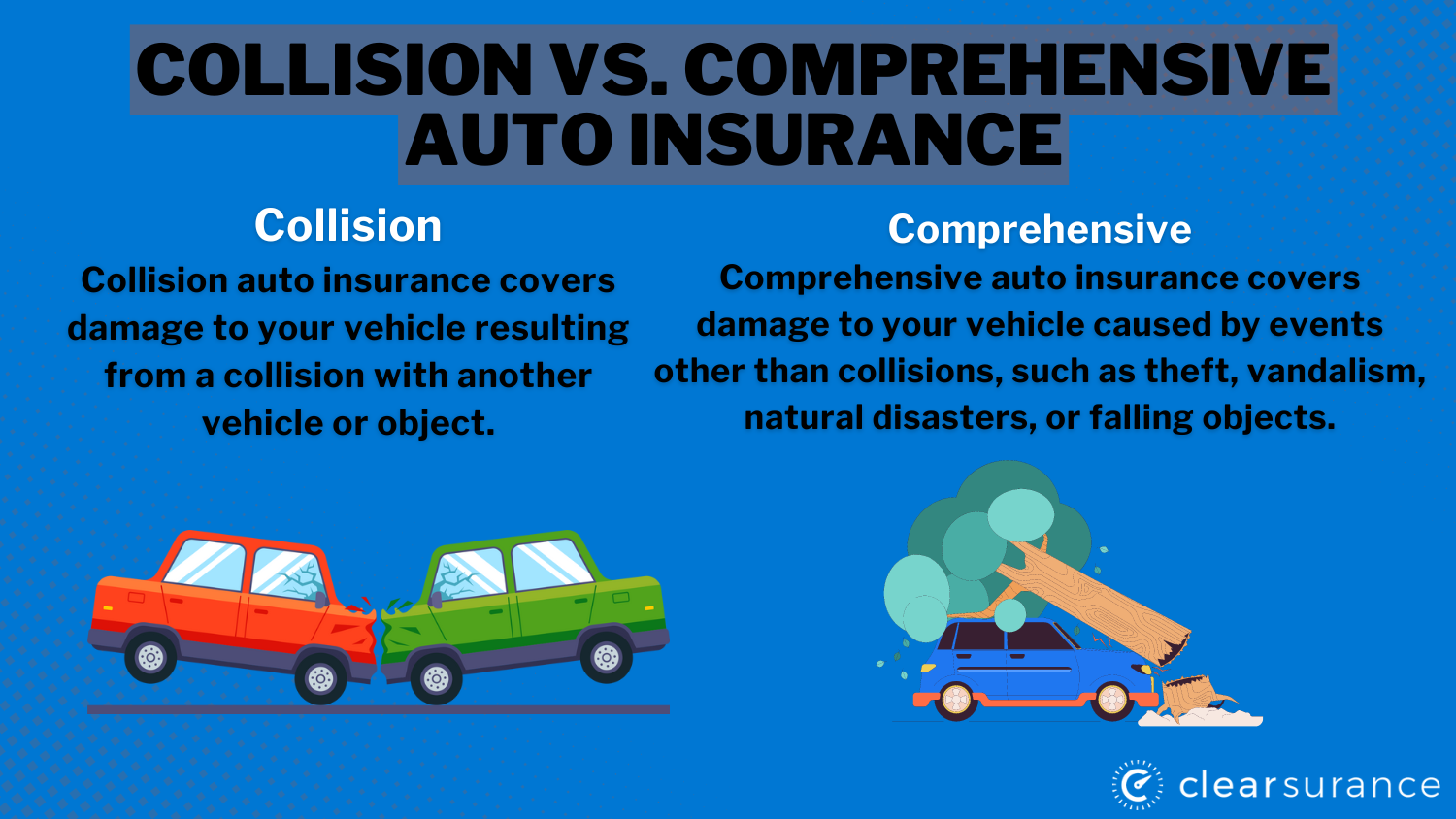

- Required coverage and optional add-ons, such as collision and comprehensive insurance

The accident history in your area can influence insurance rates. Even if you’ve maintained a clean record, a high number of local accidents may still cause your rates to increase. Insurance companies assess what a driving record is and what it tracks, distributing risk across all policyholders to ensure they can cover claims, which may lead to slight rate increases even for drivers with no accidents.

Choosing the Right SR-22 Insurance Coverage in Iowa

When dealing with SR-22 insurance, it’s important not to be underinsured or uninsured, especially if you're facing claims after an accident. However, paying for more coverage than necessary doesn't make sense either. So, how much SR-22 insurance coverage do you actually need?

The answer depends on several factors. For instance, drivers with new, leased vehicles may need collision and comprehensive coverage, while those with older cars may opt for less coverage. Additionally, each state, including Iowa, has specific SR-22 insurance requirements that must be met to stay compliant.

To determine the right SR-22 insurance coverage and limits for your situation, consult with an insurance agent or provider to ensure you meet legal obligations while avoiding unnecessary costs.

Tips to Save on SR-22 Insurance in Iowa

At the end of the day, we’d all like to have the best coverage at a cheap, affordable price. While you never want to sacrifice quality to save a couple of dollars, there are some different ways you can lower your car insurance premium.

Here are five ways you may be able to lower your car insurance rates:

- Bundle your SR-22 insurance with other policies to receive discounts

- Raise your deductibles to lower your premium costs

- Pay your SR-22 insurance policy in full to avoid extra fees

- Consider usage-based insurance to reduce costs based on driving habits

- Regularly shop and compare rates to find the best deals on SR-22 insurance

Applying these strategies and the tips learned after filing a car insurance claim allows you to secure affordable coverage while still meeting your SR-22 requirements.

SR-22 Insurance Guide

Whether you're purchasing SR-22 insurance directly or through an agent, understanding your coverage options is essential. Are you familiar with what comprehensive coverage includes? Do you know how uninsured motorist coverage works or how deductibles impact your premiums?

To ensure you're well-informed about SR-22 insurance, explore our practical guide. For more educational resources and information, visit our blog for additional insights on SR-22 and other car insurance topics.

By entering your ZIP code below, you can get instant car insurance quotes from top providers.

Frequently Asked Questions

How long is SR-22 required in Iowa?

In Iowa, SR-22 insurance is typically required for three years, although this period can vary depending on the severity of the driving violation. It's important to maintain continuous coverage during this time to avoid penalties.

How to check SR-22 status in Iowa?

You can check your SR-22 status in Iowa by contacting the Iowa Department of Transportation or by reaching out to your insurance provider, which submits the SR-22 filing on your behalf.

What is the SR-22 code in Iowa?

The SR-22 code is a certificate of financial responsibility required for high-risk drivers in Iowa, ensuring that they meet the state's minimum liability insurance standards. For a more secure option, consider exploring the Top 10 Car Insurance Companies for High-Risk Drivers to find providers that cater to such specific needs.

How much is SR-22 insurance in Iowa?

SR-22 insurance in Iowa typically costs more than standard insurance. Rates can range from $13 to $55 per month for minimum coverage, depending on the provider and your driving record.

How does SR-22 work in Iowa?

In Iowa, SR-22 is not a type of insurance but a certificate that proves you carry the minimum required auto insurance. Your insurance provider files it with the state to show compliance with Iowa's financial responsibility laws.

Can I get insurance without a license in Iowa?

Yes, getting non-owner SR-22 insurance in Iowa is possible even if you don't own a vehicle. This option primarily benefits drivers who rent or borrow cars but must still fulfill SR-22 obligations. Can you buy a car without a license? This type of policy can be a step toward meeting requirements without owning a car.

How long does SR-22 stay on your record in Iowa?

SR-22 stays on your record for three years in Iowa. During this time, you must maintain continuous coverage, as any lapse can result in penalties or suspension of your driving privileges.

What happens if you drive without insurance in Iowa?

Driving without insurance in Iowa can lead to serious consequences, including fines, license suspension, and the requirement to file SR-22 insurance. Repeated offenses may increase penalties and insurance rates.

Who has the cheapest car insurance in Iowa?

The cheapest SR-22 car insurance in Iowa varies by company, with State Farm offering rates as low as $13 per month. Other providers like Nationwide and Progressive also provide competitive pricing, making them some of the [Best and Cheapest Car Insurance in Iowa] (https://clearsurance.com/best-car-insurance/IA).

What is the minimum insurance coverage in Iowa?

The minimum auto insurance coverage in Iowa includes $20,000 for bodily injury per person, $40,000 per accident, and $15,000 for property damage per accident. SR-22 filers must meet these minimums to stay compliant with state laws.