Best California SR-22 Insurance in 2026 (Top 10 Companies Ranked)

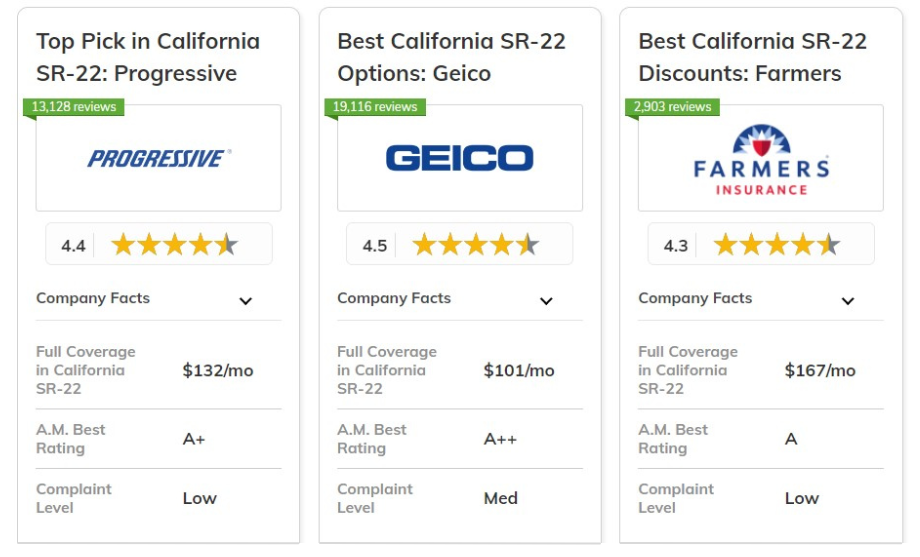

Progressive, Geico, and Farmers rank among the best California SR-22 insurance companies with rates starting at $24 per month. Progressive has solid claim handling and dedicated SR-22 filing support.

Geico is one of the most competitive companies for California SR-22 auto insurance, and Farmers’ flexible policies accommodate various driving histories.

| Company | Rank | UBI Savings | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 30% | A+ | Competitive Rates | Progressive | |

| #2 | 25% | A++ | Coverage Options | Geico | |

| #3 | 15% | A | Extensive Discounts | Farmers | |

| #4 | 30% | A++ | Military Service | USAA | |

| #5 | 30% | B | Nationwide Network | State Farm | |

| #6 | 30% | A | Customizable Plans | Liberty Mutual | |

| #7 | 40% | A+ | Trusted Reputation | Allstate | |

| #8 | 40% | A+ | Comprehensive Options | Nationwide | |

| #9 | 20% | A++ | Financial Strength | Travelers | |

| #10 | 20% | A | Personalized Service | American Family |

This article reviews each provider’s SR 22 offers and standout features, as well as car insurance companies that customers recommend. Ready to find SR-22 insurance quotes in California? Enter your ZIP code above to begin.

What You Should Know

- Progressive offer exclusive 30% UBI savings program for SR-22 filers

- Geico stands out for its affordable SR-22 insurance in California

- Farmers provides the largest discount opportunities for California SR-22 policies

#1 – Progressive: Best for Competitive Rates

Pros

- Online Dashboard Integration: In California, Progressive’s complete digital platform provides real-time SR-22 filing status tracking and instant certificate download.

- Mobile App Accessibility: The dedicated app makes SR-22 documentation and automated renewal reminders available instantly to keep lapses from occurring.

- Paperless Filing System: As mentioned in our Progressive car insurance review they offer completely digital SR-22 processing, reducing processing time.

Cons

- Higher Premiums for Multiple Violations: California drivers with multiple incidents may face significantly increased rates for SR-22 policies.

- Limited In-Person Support: Few physical locations in California for drivers who prefer face-to-face SR-22 assistance.

#2 – Geico: Best for Coverage Options

Pros

- Minimal Administrative Charges: Lowest SR-22 filing and administrative fees in California.

- Transparent Pricing Structure: No hidden charges in SR-22 costs and fees.

- Fast Online Quotes: Provides instant SR-22 insurance quotes through their website for California drivers and has high car insurance claims ratings.

Cons

- Strict Violation Guidelines: May deny coverage for certain types of violations requiring SR-22 in California.

- Limited Payment Plans: Only fewer installment options for high risk SR-22 policies.

#3 – Farmers: Best for Extensive Discounts

Pros

- Dedicated SR-22 Specialists: California SR22 specialists, trained to handle your filing requirements locally in California.

- Custom Filing Assistance: Step-by-step guidance through the SR-22 filing process with personal support.

- Flexible Coverage Options: Several SR-22 filing options depending on which policy you’re under. See details in our Farmers car insurance review.

Cons

- Higher Service Costs: Premium rates reflect the personalized service model for SR-22 filing.

- Varying Agent Availability: The quality of service may vary according to a local agent’s knowledge of SR-22 cases.

#4 – USAA: Best for Military Service

Pros

- Military-Specific Support: Handles SR-22 requirements for active duty personnel in California.

- Deployment Considerations: Adjustments to policy for deployed service members requiring SR-22.

- Family Coverage Options: Extended SR-22 support for military family members.

Cons

- Membership Restrictions: As mentioned in our USAA car insurance review, it is available only for military members and immediate families.

- Limited Physical Locations: Primarily online service for California SR-22 processing.

#5 – State Farm: Best for Nationwide Network

Pros

- Progressive Rate Reduction: Structured program for reducing SR-22 premiums over time with good driving. (Read More: State Farm Car Insurance Review)

- Safe Driver Rewards: Specific incentives for SR-22 drivers maintaining clean records.

- Renewal Guarantees: Assured policy renewal options for compliant SR-22 holders.

Cons

- Initial Cost Investment: Higher upfront premiums for new SR-22 policies.

- Extended Commitment Required: Benefits primarily reward long-term policy retention.

#6 – Liberty Mutual: Best for Customizable Plans

Pros

- Multi-Policy Integration: Our car insurance review of Liberty Mutual mentioned that you can get savings when combining SR-22 auto insurance with home or renters policies.

- Discount Stacking: Multiple discount opportunities even with SR-22 filing requirements.

- Flexible Payment Structure: Several payment procedures for handling SR-22 policy costs.

Cons

- Bundle Requirements: Maintaining multiple policies gives you best rates.

- Complex Discount Qualifications: May need multiple products to get savings.

#7 – Allstate: Best for Trusted Reputation

Pros

- 24/7 Claims Processing: Round-the-clock support for SR-22 policy claims in California.

- Accident Forgiveness Options: Special considerations for first accidents under SR-22 policies. Get more info in our Allstate car insurance review.

- Claims Satisfaction Guarantee: Written guarantee for satisfaction with SR-22 claims handling.

Cons

- Premium Claims Service Costs: Higher rates are due to enhanced claims support services.

- Strict Documentation Requirements: You’ll need clear documentation to claim under SR-22 policies.

#8 – Nationwide: Best for Comprehensive Options

Pros

- Personalized Risk Evaluation: Detailed assessment process that may result in lower SR-22 rates for some violations.

- SmartRide Program: Usage-based options to demonstrate safe driving and reduce SR-22 premiums.

- Flexible Risk Categories: Multiple rating tiers for different SR-22 situations. Find out more in our Nationwide car insurance review.

Cons

- Extensive Evaluation Period: More time is needed for the assessment of SR-22 policies.

- Complex Rating Factors: Many factors determine your final SR-22 premium.

#9 – Travelers: Best for Financial Strength

Pros

- Comprehensive Guide System: Take a look at our Travelers car insurance review for a detailed educational resources about California SR-22 requirements and compliance.

- Online Learning Tools: Interactive modules helping drivers understand their SR-22 obligations.

- Compliance Tracking: Track your SR-22 filing status and tools to monitor your SR-22 as well.

Cons

- Limited California Coverage Areas: Travelers SR-22 services are not available in some California regions.

- Self-Service Focus: Instead of personal assistance, they especially focus on online resources.

#10 – American Family: Best for Personalized Service

Pros

- New Filer Support Program: Specialized assistance for drivers requiring SR-22 for the first time.

- Clear Filing Guidelines: Step-by-step process explanation for new SR-22 requirements.

- First-Time Filing Discounts: Explore our American Family review as they have special rates for first-time SR-22 policy holders.

Cons

- Limited California Presence: Smaller network of agents in California compared to other providers.

- Restricted Coverage Options: Fewer policy customization choices for new SR-22 filers.

SR-22 Insurance Cost in California

After certain driving violations, California drivers must file the SR-22 form to reinstate driving privileges. The California Insurance Proof Certificate, or SR-22, is proof that you meet minimum insurance requirements and lets you drive legally. Here's the monthly average cost of SR-22 insurance in California from top providers:

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $65 | $199 | |

| $45 | $138 | |

| $54 | $167 | |

| $33 | $101 | |

| $70 | $216 | |

| $47 | $142 | |

| $43 | $132 | |

| $35 | $108 | |

| $40 | $122 | |

| $24 | $74 |

Eventually, continuous coverage can get you to normal rates post-SR-22. Failure to file an SR-22 will lead to a registration suspension, so be sure you’re in compliance to drive legally in California.

SR-22 insurance also requires keeping coverage for a minimum of three years. Your insurer may file an SR-26 if the policy is canceled, and if you get suspended, you may need a new one (SR-22). Here is the required SR-22 coverage in California:

- $15,000 for bodily injury per person

- $30,000 for bodily injury per accident

- $5,000 for property damage per accident

To find low cost SR 22 insurance in California, compare quotes from several different providers to get affordable coverage on the cheap. By knowing which are the most common auto insurance claims in California, drivers are aware of some of the most common risks and related costs.

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Rear-End Collisions | 0.3 | 10000 |

| Single-Vehicle Accidents | 0.25 | 15000 |

| Vehicle Theft | 0.15 | 12000 |

| Parking Lot Accidents | 0.1 | 5000 |

| Weather-Related Damage | 0.08 | 7000 |

The claim types above are why choosing the correct coverage when you live in California is important so you can avoid unexpected expenses should something happen. The following gives a picture of accidents and claims in major cities.

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Bakersfield | 5,600 | 5,000 |

| Fresno | 8,200 | 7,500 |

| Long Beach | 6,800 | 6,200 |

| Los Angeles | 50,000 | 45,000 |

| Oakland | 9,500 | 8,900 |

| Riverside | 7,200 | 6,500 |

| Sacramento | 10,500 | 9,800 |

| San Diego | 25,000 | 22,000 |

| San Francisco | 18,000 | 15,500 |

| San Jose | 12,000 | 11,000 |

Understanding these statistics will help you identify high risk areas and help drivers make coverage decisions based on local accident trends.

Read More: How To Register a Car in California

Discounts to Get for SR-22 Insurance in California

Best California SR-22 insurance companies will offer saving options for high risk drivers like specific insurance discounts and usage-based insurance plans.

Geico and State Farm are two of the providers that may offer California SR22 holders multi policy discounts or safe driving incentives that can help reduce their SR22 insurance rates California drivers have to pay.

| Insurance Company | Available Discount |

|---|---|

| Multi-Vehicle, Defensive Driver, Loyalty, Good Student, Auto Safety Equipment | |

| Multi-Policy, Good Driver, Pay-in-Full, Homeowner, Good Student, Signal Program | |

| Defensive Driver, Good Student, Multi-Policy, Anti-Theft, New Vehicle, Military | |

| Multi-Car, Early Shopper, Pay-in-Full, Homeowner, Military, Online Purchase | |

| Multi-Policy, SmartRide, SmartMiles, Good Student, Anti-Theft, Accident-Free | |

| Multi-Policy, Snapshot, Pay-in-Full, Homeowner, Good Student, Continuous Insurance | |

| Good Student, Safe Driver, Multi-Policy, Anti-Theft, Drive Safe & Save, Defensive Driver | |

| Multi-Policy, Safe Driver, Homeowner, Pay-in-Full, New Car, Continuous Insurance | |

| Safe Driver, Military, Loyalty, Defensive Driving, New Vehicle, Multi-Policy | |

| Safe Driver, Military, Loyalty, Defensive Driving, New Vehicle, Multi-Policy |

However, for people who want cheap SR 22 insurance California plans, adding a higher insurance deductible or only liability coverage can keep costs down, while offering a mixture of flexible, affordable California SR 22 insurance plans.

| Discount Name | Grade | Savings | Participating Providers |

|---|---|---|---|

| Multi-Policy Discount | A+ | 30% | Allstate, State Farm, Liberty Mutual, Geico |

| Good Driver Discount | A | 25% | Geico, Progressive, Farmers, Nationwide |

| Good Student Discount | B+ | 20% | State Farm, Allstate, American Family |

| Multi-Vehicle Discount | B | 15% | Progressive, Farmers, Liberty Mutual |

| Low Mileage Discount | B- | 10% | Nationwide, Allstate, State Farm |

| Defensive Driving Discount | C+ | 10% | Liberty Mutual, Geico, Allstate |

| Paperless & AutoPay Discount | C | 5% | Progressive, Geico, Travelers |

Choosing a provider with the right discounts can significantly reduce costs, making coverage more affordable for California drivers.

Choosing the Right SR-22 Insurance in California

California’s auto insurance premiums are influenced by factors like affordability, claims satisfaction, and discount availability.

| Category | Grade | Explanation |

|---|---|---|

| Affordability for Good Drivers | A | California provides competitive premiums for good drivers with clean records, often below the national average. |

| Rate Stability | A- | Premium rates in California remain relatively stable compared to other states, with fewer sudden increases. |

| Discount Availability | B+ | A wide range of discounts, including multi-policy and good driver discounts, are available across providers. |

| Claims Satisfaction | B | Claim processing times are generally reasonable, though satisfaction varies among insurers. |

| Rate for High-Risk Drivers | C+ | High-risk drivers face significant premiums due to California's stricter regulations on driving records. |

| Customer Service | C | Customer service ratings are average; some insurers excel, but others receive complaints about response times. |

| Rate Affordability for Young Drivers | C- | Young drivers in California often experience high premiums, primarily due to the elevated risk factor. |

The best California SR 22 insurance is provided by Progressive, Geico and Farmers, each with its own edge. One of the best things about Progressive is its competitive rates and usage based discounts, which means it’s great for budget minded drivers. (Read More: Best Usage-Based Car Insurance)

Geico offers a wide selection of coverage choices and keeps filing fees low. Farmers presents an extensive number of discount options for all types of driving histories.

Finding cheap SR-22 insurance quotes in California is easy. Just enter your ZIP code into our free comparison tool below to instantly compare quotes near you.

Frequently Asked Questions

How much does SR-22 insurance cost in California?

SR-22 insurance in California typically starts at around $24 per month for minimum coverage, but costs can vary based on factors like the driver’s history and provider.

How to get an SR-22 in California?

To obtain an SR-22 in California, contact the best SR-22 car insurance companies that offer filing services, such as Progressive, Geico, or Farmers. They will file the SR-22 certificate on your behalf with the DMV.

How long do you need SR-22 insurance in California?

Most drivers in California are required to maintain SR-22 insurance for at least three years, but this duration can vary depending on the specifics of the violation.

See how much you’ll pay for car insurance by entering your ZIP code below into our free comparison tool.

How much does an SR-22 raise your insurance?

An SR-22 can raise your insurance by a significant amount, depending on your provider and driving history. Premium increases vary, as some factors are one of the reasons why car insurance is so expensive .

How long does SR-22 stay on insurance in California?

The SR-22 filing typically stays active on your insurance record for the mandated period of three years. After that, it can be removed if you meet compliance requirements.

How to file an SR-22 in California?

Filing an SR-22 in California requires contacting an insurance company and requesting them to file it for you. Providers like Progressive, Geico, and Farmers can assist with SR-22 filings.

How do I find out if I still need an SR-22 in California?

To check your SR-22 status, contact your insurance provider or the California DMV. They can confirm if your SR-22 requirements have been fulfilled.

How expensive is SR-22 insurance?

SR-22 insurance costs vary widely but start as low as $24 per month in California. However, rates can increase based on driving history and the provider's risk assessment.

How long does SR-22 last in California?

In California, SR-22 insurance is generally required for a minimum of three years, but some situations may require a longer duration depending on the offense.

Read More: What Is Considered a Clean Driving Record?

How much is an SR-22 per month?

In California, SR-22 insurance starts at about $24 per month for minimum coverage, though rates can rise based on individual risk factors.

How to get an SR-22 online?

Many providers, including Geico and Progressive, offer online SR-22 filings. You can get an SR-22 online by selecting an insurance plan that includes SR-22 filing, then applying through the provider's website.

Find the best comprehensive car insurance quotes by entering your ZIP code below into our free comparison tool today.