Best Alaska SR-22 Insurance in 2026 (Top 10 Companies Ranked)

When looking for the best Alaska SR-22 insurance, Erie, Travelers, and Geico are the top three choices. They offer good coverage, with prices beginning at $25 monthly.

Erie is known for its cheap rates and robust coverage options. Travelers is a perfect choice if you need non-owner policies. Geico offers competitive rates for high-risk drivers, making them all top picks for SR-22 insurance coverage in Alaska.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 25% | A+ | Affordable Rates | Erie | |

| #2 | 13% | A++ | Reliable Coverage | Travelers | |

| #3 | 25% | A++ | Low Rates | Geico | |

| #4 | 17% | B | Strong Reputation | State Farm | |

| #5 | 25% | A+ | Comprehensive Options | Allstate | |

| #6 | 20% | A | Tailored Services | Farmers | |

| #7 | 25% | A | Family-Oriented Focus | American Family | |

| #8 | 20% | A+ | Broad Availability | Nationwide | |

| #9 | 10% | A+ | Innovative Discounts | Progressive | |

| #10 | 5% | A+ | Senior-Friendly Plans | The Hartford |

Comparing quotes from these companies can help you find the best fit for your needs.

To find the best comprehensive car quotes, enter your ZIP code now.

What You Should Know

- Erie offers the best Alaska SR-22 insurance with rates starting at $24/month

- High-risk Alaska SR-22 drivers benefit from reliable coverage options

- Non-owner SR-22 policies ensure compliance for drivers without vehicles

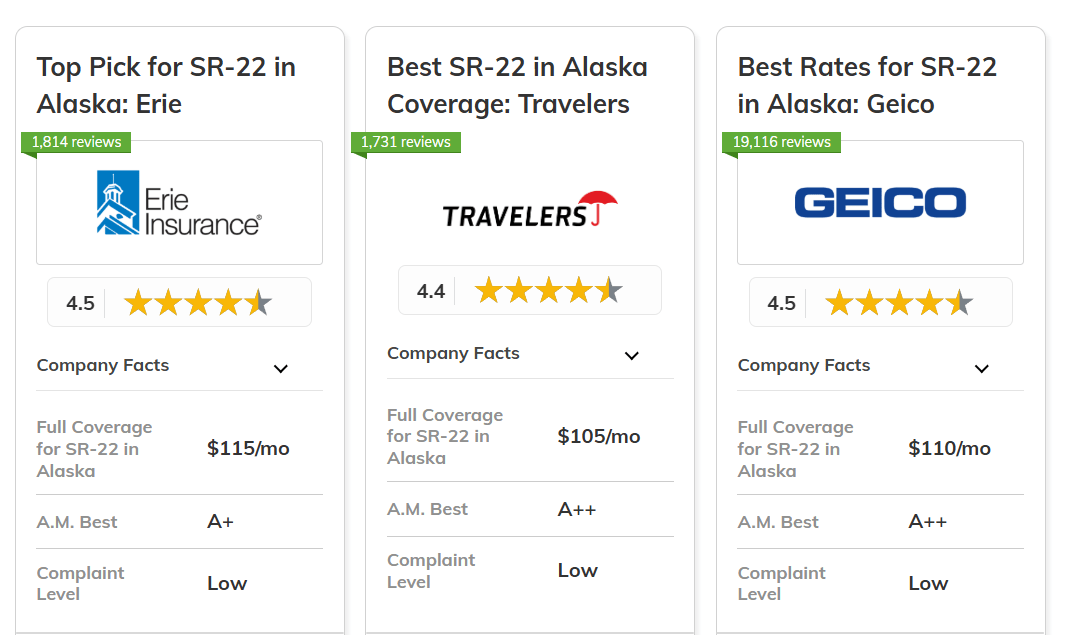

#1 – Erie: Top Overall Pick

Pros

- Affordable Rates: Erie offers Alaska SR-22 insurance starting at just $25/month. Get detailed insights in our Erie insurance review

- Great Discounts: Save up to 25% by bundling Alaska SR-22 insurance with other policies.

- Reliable Coverage: Backed by an A+ rating, Erie provides dependable Alaska SR-22 insurance.

Cons

- Not Everywhere: Erie’s Alaska SR-22 insurance isn’t available in all areas.

- Fewer Online Tools: Managing your Alaska SR-22 insurance policy digitally can be limited.

#2 – Travelers: Best for Reliable Coverage

Pros

- Good Choices: Travelers provides trustworthy Alaska SR-22 insurance for drivers that pose a high risk.

- Financially Secure: Reliable Alaska SR-22 insurance claims are ensured by an A++ rating. Explore our review of Travelers review.

- Flexible Plans: It's easier to comply with non-owner Alaska SR-22 insurance policies.

Cons

- Higher Starting Premiums: Compared to some competitors, Travelers' Alaska SR-22 insurance premiums may be more expensive.

- Smaller Discounts: For Alaska SR-22 insurance, a 13% bundling discount is not the most excellent option.

#3 – Geico: Best for Low Rates

Pros

- Budget-Friendly: Geico’s Alaska SR-22 insurance starts at $25/month. Find out tips we learned after filing a car insurance claim.

- Easy to Manage: Their online platform simplifies handling Alaska SR-22 insurance.

- Big Savings: Get a 25% discount by bundling Alaska SR-22 insurance with other coverages.

Cons

- Limited Options: Geico doesn’t always have broad Alaska SR-22 insurance coverage choices.

- Delayed Support: Customer service for Alaska SR-22 insurance might take longer.

#4 – State Farm: Best for Strong Reputation

Pros

- Reputable Brand: State Farm is a trustworthy option for SR-22 insurance in Alaska. Learn more by reading our State Farm review.

- Good Savings: When you mix Alaska SR-22 insurance with other schemes, you can save up to 17%.

- Local Representatives: For all your Alaska SR-22 insurance requirements, in-person assistance is offered.

Cons

- Increased Costs: State Farm's Alaska SR-22 insurance rates are not the lowest.

- Limited Non-Owner Options: Alaska SR-22 insurance policies for non-owners are more limited.

#5 – Allstate: Best for Comprehensive Options

Pros

- Full Coverage: Allstate offers extensive Alaska SR-22 insurance options, including liability.

- Reliable Ratings: A+ financial strength ensures your Alaska SR-22 insurance claims are secure.

- Big Bundling Perks: Save 25% by combining Alaska SR-22 insurance with other policies. Get further details in our Allstate review.

Cons

- Pricey Plans: Allstate’s Alaska SR-22 insurance costs can be high for some drivers.

- Limited Flexibility: Adjusting Alaska SR-22 insurance coverage may take extra effort.

#6 – Farmers: Best for Tailored Services

Pros

- Custom Options: Farmers customize Alaska SR-22 insurance to meet the requirements of individual drivers.

- Good Deals: When you combine Alaska SR-22 insurance with other plans, you can save 20%. Read more in our Farmers review.

- A-Rated Financial Strength: An A-rated company guarantees the security of your Alaska SR-22 insurance.

Cons

- Increased Premiums: Compared to more affordable competitors, Farmers' Alaska SR-22 insurance premiums are higher.

- Less Tech-Friendly: Online tools for managing Alaska SR-22 insurance could improve.

#7 – American Family: Best for Family-Oriented Focus

Pros

- Family-First: Alaska SR-22 insurance plans cater to household budgets. Access in-depth insights in our American Family review.

- Great Discounts: Save 25% when bundling Alaska SR-22 insurance with home and auto coverage.

- A-Rated: Financial stability backs Alaska SR-22 insurance claims with confidence.

Cons

- Limited Reach: Alaska SR-22 insurance coverage may not be available everywhere.

- Higher Premiums: Rates for Alaska SR-22 insurance can add up for high-risk drivers.

#8 – Nationwide: Best for Broad Availability

Pros

- Broad Coverage: Most areas can obtain Nationwide's Alaska SR-22 insurance.

- Discounts for Bundling: Combining policies can save you up to 20% on Alaska SR-22 insurance.

- Strong Ratings: Safe Alaska SR-22 insurance services are guaranteed by an A+ rating. Read our Nationwide reviewfor details.

Cons

- Rates Vary: The cost of Alaska SR-22 insurance varies greatly depending on the area.

- Fewer Deals: Discounts for high-risk Alaska SR-22 insurance drivers could improve.

#9 – Progressive: Best for Innovative Discounts

Pros

- Usage-Based Savings: Progressive rewards safe driving with Alaska SR-22 insurance discounts.

- Flexible Plans: Policies are customizable to fit specific Alaska SR-22 insurance needs.

- Reliable Backing: An A+ rating ensures dependable Alaska SR-22 insurance claims. Discover insights in our Progressive review.

Cons

- Small Bundling Discount: Only 10% savings on combined Alaska SR-22 insurance policies.

- Higher DUI Rates: Progressive’s Alaska SR-22 insurance costs for DUIs can be steep.

#10 – The Hartford: Best for Senior-Friendly Plans

Pros

- Senior Perks: Alaska SR-22 insurance includes discounts for older drivers. Discover more about offerings in our The Hartford review.

- Financial Security: A+ rating backs Alaska SR-22 insurance with dependable claims support.

- Added Benefits: Roadside assistance enhances Alaska SR-22 insurance policies.

Cons

- Narrow Focus: Best suited for senior drivers needing Alaska SR-22 insurance.

- Smaller Discounts: A 5% bundling discount doesn’t stretch far for Alaska SR-22 insurance.

Top Providers Offering Competitive SR-22 Rates

The table below breaks down monthly rates for Alaska SR-22 insurance, showing how much you can expect to pay for minimum and full coverage with different providers.

Alaska SR-22 Monthly Rates by Coverage Level

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $35 | $145 | |

| $40 | $130 | |

| $25 | $115 | |

| $38 | $125 | |

| $28 | $110 | |

| $42 | $140 | |

| $45 | $135 | |

| $30 | $120 | |

| $48 | $150 | |

| $27 | $105 |

Monthly prices for Alaska SR-22 insurance change significantly, so it's good to check different options. Erie is notable because it offers the cheapest rate for basic coverage at only $25 per month. Travelers come next with a price of $27 per month, and Geico follows close behind with a $28 monthly cost.

Again, Travelers is the best choice for full coverage, costing $105 per month. Geico and Erie come next at $110 and $115 monthly. On the more expensive side, The Hartford's full coverage costs $150 monthly for those who want detailed plans. Whether you want to save money or prioritize comprehensive insurance coverage), these monthly rates highlight the importance of comparing options to find what works best for your budget.

Top Discounts for Alaska SR-22 Insurance

The table below breaks down the discounts from top providers offering Alaska SR-22 insurance. These discounts can significantly lower your monthly rates by rewarding safe driving, bundling policies, and other perks.

| Insurance Company | Available Discount |

|---|---|

| Safe Driver, Bundling, Payment-in-Full, Anti-Theft Device | |

| Safe Driver, Bundling, Homeowner, EFT Payment | |

| Good Driver, Multi-Vehicle, Military, Defensive Driving | |

| Safe Driver, Good Student, Bundling, Anti-Theft Device | |

| Safe Driver, Bundling, Early Signing, Anti-Lock Brakes | |

| Good Driver, Bundling, Paperless, Homeowner | |

| Safe Driver, Bundling, Auto Pay, Good Student | |

| Safe Driver, Bundling, Paperless, Accident-Free | |

| Snapshot, Bundling, Continuous Insurance, Pay-in-Full | |

| Bundle (Auto & Home), Defensive Driving, Vehicle Safety Features |

Regarding Alaska SR-22 insurance, there are plenty of ways to save with discounts. Erie offers safe driver rewards, bundling deals, and even anti-theft device discounts, making it a top pick for keeping costs down. Geico has excellent options like military car insurance and defensive driving discounts, while Progressive’s Snapshot program gives safe drivers significant savings.

Both Travelers and State Farm give discounts if you have a safe driving record or if you combine different insurance policies. Allstate and American Family focus more on providing benefits to students with good grades or when customers sign up early for their services. These discounts can help you find a good deal and keep your monthly insurance payments low.

Understanding Alaska SR-22 Filing Requirements

The Alaska SR-22 insurance form is a document that proves you’re carrying the minimum auto insurance required in the state. You may be required by the state or court to file an SR-22 form if you’ve committed a certain driving violation and have had your license suspended.

The requirement is often called SR-22 insurance, even though it isn’t a different type of insurance from your traditional car insurance. It’s called SR-22 insurance because the requirement may affect your car insurance coverage and rates. On average, drivers in Alaska pay 40.5 percent more for SR-22 insurance after a DUI than drivers with a clean record, but some SR-22 insurance companies are cheaper than others.

Alaska SR-22 insurance is typically required for a minimum of three years. Still, the duration you need the SR-22 varies from person to person, depending on why your license has been suspended and if you’re a repeat offender. If you have a DUI and it’s your first offense, Alaska SR-22 insurance is required for five years. SR-22 insurance is required for 10 years after a second DUI, 20 years after a third, and a lifetime after a fourth, including for breathalyzer refusals.

You must maintain your Alaska SR-22 insurance policy for the duration of your filing period without a lapse in coverage. If you let this insurance lapse or need to cancel your car insurance, your insurance provider is required by law to notify the state of Alaska know that you no longer have an active SR-22 insurance policy with the company.

Your company files an SR-26 to cancel the SR-22, and lapses may restart your filing period. Non-car owners need a non-owner SR-22 policy.

If you maintain your SR-22 insurance, keep a clean driving record, and fulfill all other requirements related to your violation, you won’t need to continue to file an SR-22 once your required filing period has ended. If you commit another violation in the future, you may need SR-22 insurance again.

Understanding Alaska's SR-22 Insurance Limits

The SR-22 verifies to the state of Alaska that you have at least the minimum requirements for liability insurance. All drivers are required to have liability insurance in Alaska. If you’re required to have SR-22 insurance in Alaska, you’ll also need to understand when to file a car insurance claim to ensure you’re properly covered under your policy. The required minimum coverage limits for SR-22 insurance include:

- $50,000 for Bodily Injury per Person

- $100,000 for Bodily Injury per Accident

- $25,000 for Property Damage per Accident

Having the right coverage for Alaska SR-22 insurance keeps you on the right side of the law and protected on the road. Stick to the required limits, and you’ll stay insured and avoid any unnecessary hassles.

Eligibility for Alaska SR-22 Insurance

SR-22 insurance is required in Alaska after certain traffic offenses. It could even be required after a number of small driving violations in a short period of time. You could need Alaska SR-22 insurance for the following reasons:

- Conviction for Driving Under the Influence (DUI or DWI)

- Driving Without Car Insurance

- Driving With a Revoked or Suspended License

- Numerous At-Fault Accidents

- Reckless or Dangerous Driving

A single traffic violation like a speeding ticket is unlikely to come with an SR-22 requirement, but multiple speeding tickets might.

Top Claim Types and Their Costs

This table highlights common accidents in Alaska, their costs, and frequency. Rear-end crashes lead with 40% of claims at $7,000 each, followed by fender benders at 25% and $3,000 per claim. Single-vehicle accidents, while 20% of claims are costliest.

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Rear-End Collision | 40% | $7000 |

| Fender Bender | 25% | $3000 |

| Single Vehicle Accident | 20% | $15000 |

| Side-Impact Collision | 10% | $12000 |

| Theft Claim | 5% | $15000 |

Side-impact collisions (10%) average $12,000, and theft claims, though rare (5%), cost $15,000. Knowing these stats helps us understand the steps to take after a car accident for proper documentation and claims handling.

Accident Trends and Claims Insights Across Alaskan Cities

Anchorage reports 3,500 accidents and 2,800 claims yearly, with Fairbanks at 1,200 accidents and 950 claims. Smaller towns like Juneau, Ketchikan, and Wasilla see 400–800 accidents and 300–650 claims.

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Anchorage | 3,500 | 2,800 |

| Fairbanks | 1,200 | 950 |

| Juneau | 800 | 650 |

| Ketchikan | 400 | 300 |

| Wasilla | 600 | 500 |

One of the tips learned after filing car insurance claims in high-traffic areas like Anchorage is the importance of thoroughly documenting accidents. This includes photos, witness accounts, and quick insurer reporting to prevent disputes.

Balancing Discounts with Risk Factors

This table highlights ways to save on SR-22 insurance and what drives premiums up in Alaska. Safe driver discounts can cut costs by 40% with Geico, Progressive, and State Farm, while a multi-vehicle policy offers 25% savings through Allstate and Nationwide.

| Discount Name | Grade | Savings | Participating Providers |

|---|---|---|---|

| Safe Driver | A | 40% | Geico, Progressive, State Farm |

| Multi-Vehicle | B+ | 25% | Allstate, Nationwide |

| Defensive Driving | B | 15% | Farmers, Liberty Mutual |

| Bundling Policies | C+ | 10% | Travelers, The Hartford |

| Paperless Billing | C | 5% | Progressive, USAA |

The cost benefits of taking a defensive driving course include a 15% discount with Farmers and Liberty Mutual. Bundling policies and going paperless offer smaller savings of 10% and 5%, lowering premiums while encouraging safer driving.

Alaska's moderate theft rate raises premiums, while low traffic cuts risks. But because of expensive repairs and towing, average claim sizes are more significant, and harsh winters cause more accidents, which drives up rates.

| Category | Grade | Explanation |

|---|---|---|

| Vehicle Theft Rate | B | Moderate vehicle theft rate impacts premium calculation for SR-22 policies |

| Traffic Density | B | Low population density reduces the frequency of major traffic congestion |

| Average Claim Size | C | Claims in Alaska tend to be higher due to costly vehicle repairs and towing |

| Weather-Related Risk | C | Harsh winters increase accident risk, raising premiums for SR-22 policyholders |

| Uninsured Drivers Rate | D | High percentage of uninsured drivers increases costs for insured individuals |

The vast number of uninsured drivers also raises costs for those insured. For better protection, drivers should consider gap insurance, especially in high-risk areas.

Breakdown of Alaska SR-22 Insurance Rates

If you need SR-22 insurance, you'll be considered a high-risk or non-standard driver. Your SR-22 rates depend on your driving record, insurer, age, location, credit score, and vehicle type.

A DUI is a common reason for needing SR-22 insurance. On average, drivers with one DUI conviction in Alaska pay approximately $135 monthly for car insurance. That's 40.5% more than drivers with clean records.

However, the cost you pay differs significantly based on the company you buy car insurance from. In the table below, you can find average rates for Alaska drivers who have one DUI conviction from some of the largest auto insurance companies in the state.

| Insurance Company | Monthly Rates |

|---|---|

| $205 | |

| $144 | |

| $124 | |

| $93 | |

| $93 |

*USAA is only available to active and former military members and their families.

These rates are based on a 35-year-old single adult with one driver and one vehicle on a policy. The car used was a 2015 Toyota Highlander LEs. Full coverage was used with 100/300/50 limits and a $500 collision and comprehensive deductible. The driver had 1 DUI on their record. The rates displayed should only be used for comparative purposes as individual rates for high-risk insurance in Alaska will differ. Rate data is provided by Quadrant Information Services.

SR-22 insurance is expensive, but once your filing period is over, you have a good chance of your premiums dropping to more affordable levels. To ensure this, you should make sure to pay premiums on time during the mandatory filing period. Also, you should drive carefully and maintain a clean record of safe driving free from violations.

Navigating the SR-22 Insurance Process in Alaska

To file an SR-22 form in Alaska, you’ll need to go through an insurance company because it’s not something you can file on your own. It’s important to note that not all car insurance companies offer SR-22 insurance. You can shop around by getting quotes from multiple SR-22 insurance companies in order to find the best price.

Use the table at the top of this page to find all the car insurance companies that offer SR-22 insurance in Alaska with a minimum of 25 reviews. If you want to see which companies customers say are the best car insurance companies for SR-22 insurance in Alaska, sort the table by highest rated. You can sort through companies and find the ones you want to get quotes from. To get quotes, click on the orange “Click for quote” button next to the company, call the number available, or visit the company’s website.

If you want to read customer reviews of the company, click the company name in the table and you will be directed to the company’s profile page containing information about the company and reviews.

SR-22 Filing and Reinstatement Expenses in Alaska

Your insurance company may charge you a filing fee for the SR-22 form. The form usually costs between $25 and $50, but the price can vary by company.

Additionally, you may need to pay fees specific to the violation you committed that required you to have SR-22 insurance. If your license was suspended, you’ll need to pay a reinstatement fee in order to regain your driving privileges. The reinstatement fee starts at $100 for a non-DUI related offense and $200 for a DUI. Working with the best car insurance in Alaska can help streamline this process and provide support for your unique needs.

Factors That Influence Car Insurance Rates

When searching and comparing car insurance quotes, it can be frustrating trying to understand how your insurance rates are calculated and how to get cheap car insurance. While there is no exact formula that each car insurance company uses when providing you a quote, there are many factors that do contribute to the price you pay for your insurance. Among the factors that car insurers consider are:

- Your Driving Record and How Much You Drive

- Location, Age, and Marital Status

- Gender and Credit Score (In Some States)

- Your Car’s Make, Model, and Year

- Required and Optional Car Insurance Coverage Levels

One of the biggest misunderstanding when it comes to insurance rates is that the history of drivers in your area also contributes to how much you pay. For instance, even if you go two years without an accident, if there were a lot of accidents near you recently, your rates might still go up. Why is that the case?

Insurance companies disperse risk across all policyholders so that when it comes time to pay a claim, they have enough money to pay out. But imagine a scenario where they only raised rates for drivers with an accident. Drivers with costly claims often can't afford the higher rates tied to their accident costs. To offset this, insurers slightly raise rates for all policyholders, with at-fault drivers seeing larger increases.

Determining the Right Amount of Car Insurance

You certainly don’t want to be underinsured or uninsured while staring at a claim after a car accident or other damage to your car. But at the same time, there’s no sense in paying for more coverage than you need, right? So it begs the question: How much car insurance coverage do you actually need?

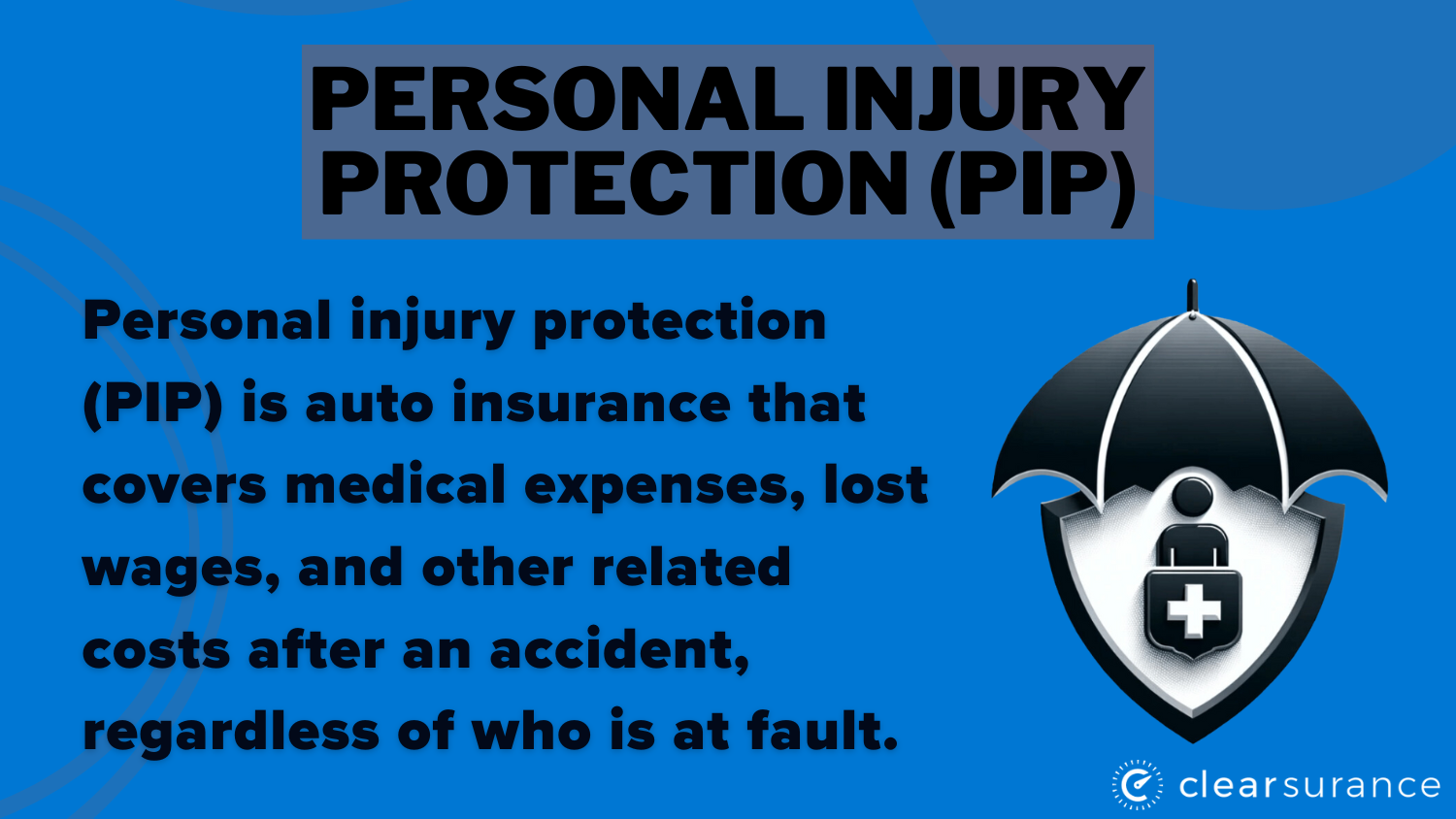

The answer, as frustrating as it may be, is it depends. For example, someone insuring a brand-new, leased car is likely required to purchase collision and comprehensive coverage, but for someone driving an older car that doesn’t have much value, it may not make sense to purchase optional coverage. Plus, states have different car insurance requirements. There are 12 no-fault states that require its drivers to purchase personal injury protection (PIP).

So when it comes to determining what car insurance coverage and limits you should purchase, it’s important to do your research. Consulting an insurance agent or your company ensures you get coverage tailored to your needs while exploring the top ways customers have saved money on car insurance rates.

Tips to Reduce Your Car Insurance Costs

At the end of the day, we’d all like to have the best coverage at a cheap, affordable price. While you never want to sacrifice quality to save a couple of dollars, there are some different ways you can lower your car insurance premium.

Here are ways you may be able to lower your car insurance rates:

- Bundle Your Car Insurance With Other Policies

- Consider Raising Your Deductibles

- Pay Your Car Insurance Policy in Full

- Try Usage-Based Car Insurance

- Monitor Price Changes to Your Policy

A usage-based insurance program uses a telematics device or mobile app on your phone to monitor your driving habits. When you drive safely, you are rewarded with a discount on your auto insurance coverage.

Other common discounts include the safe driver discount, multi-policy discount (for bundling), good student discount, and multi-vehicle discount. Many auto insurers also offer a discount for certain safety features on your vehicle, like anti-lock brakes and daytime running lights.

Experts recommend you get at least three auto insurance quotes before you choose a policy. Comparing these quotes and applying hacks to save money on your car insurance rates, like leveraging discounts, can help you find a deal that fits your budget. If SR-22 insurance feels too expensive, shop around for better options that meet your needs.

Clearsurance’s Approach to Ranking Insurers

Wondering how Clearsurance determines scores for insurance companies? Our algorithm analyzes a range of inputs from our community of unbiased insurance customers, including:

- Cost

- Customer Service

- Overall Experience

- Claim Service

- Purchasing Experience

Clearsurance ratings come straight from real customers, focusing on things like cost, customer service, and overall experience. We break it all down, including claims and buying experiences, to help you pick the right insurance with confidence. (Read More: Clearsurance’s Customers’ Choice Top Ranked Insurance Companies).

Understanding the Basics of Car Insurance

When you buy insurance by yourself or with help from an agent, it is essential to know the different options for car insurance coverage. Do you understand what comprehensive coverage includes? Are you familiar with uninsured motorist coverage? Do you understand how a deductible works?

We want to ensure that you have the right knowledge about car insurance, so please look at our practical guide to understanding car insurance.

Comparing quotes is the simplest method for locating reasonably priced auto insurance. Use our free comparison tool to view rates in your area.

Frequently Asked Questions

What is SR-22 insurance in Alaska?

SR-22 insurance in Alaska is a certificate proving you meet the state's minimum liability coverage after certain driving violations, such as DUIs or license suspensions.

What is the cost of SR-22 insurance in Alaska?

The cost of SR-22 insurance in Alaska varies by provider but typically starts at $25 monthly for minimum coverage. Premiums increase based on driving history and coverage needs.

What are the requirements for SR-22 in Alaska?

Alaska requires SR-22 insurance to meet minimum liability limits, including how much bodily injury liability is needed: $50,000 bodily injury per person, $100,000 per accident, and $25,000 property damage.

Where can I find Alaska SR-22 insurance quotes?

You can find Alaska SR-22 insurance quotes by comparing providers like Geico, Progressive, and State Farm online or through local agents offering SR-22 filings.

What is DUI insurance in Alaska?

DUI insurance in Alaska refers to high-risk auto insurance policies required after a DUI conviction, often including an SR-22 filing. Premiums are typically 40% higher than standard rates.

What age is car insurance most expensive in Alaska?

Car insurance is the most expensive for drivers under 25 in Alaska due to their higher risk profile. Still, car insurance companies for high-risk drivers can help provide affordable options tailored to their needs.

Where can I get SR-22 insurance in Anchorage, AK?

SR-22 insurance for high-risk drivers is offered in Anchorage, AK, by both regional brokers and national companies such as Geico, State Farm, and Travelers.

Who are the top car insurance companies in Alaska?

Some of the best auto insurance in Alaska are offered by Geico, Progressive, State Farm, and Allstate. Rates and incentives for different types of drivers are extremely competitive with these firms.

Is Alaska a no-fault state?

Driving without insurance in Alaska can result in fines, license suspension, and a penalty for driving without insurance, such as a requirement to file SR-22 insurance to reinstate your driving privileges.

Does SR-22 cover any car I drive in Alaska?

SR-22 insurance can cover any car you drive if you purchase non-owner SR-22 insurance or apply your policy to multiple vehicles.

What is the best car insurance for SR-22?

Erie is considered the best car insurance for SR-22 in Alaska, offering rates starting at $25 per month with comprehensive coverage options.

What is the cheapest auto insurance in Alaska?

Geico or Erie often offer the cheapest auto insurance in Alaska, with rates starting as low as $25 per month for minimum coverage.

Is car insurance high in Alaska?

Car insurance in Alaska is relatively affordable compared to other states. Still, rates can be higher for SR-22 policies or high-risk drivers, leading some to wonder why is car insurance so expensive for specific individuals.

What company has the cheapest SR-22?

A basic coverage policy with Erie begins at $25/month, making it the most affordable SR-22 insurance in Alaska.

Is Alaska a no-fault state?

No, Alaska is not a no-fault state; drivers are liable for damages they cause in an accident.

What is the highest type of car insurance?

Full coverage is the optimal choice for auto insurance. To offer you the maximum protection, it often combines liability, collision, and comprehensive coverage.

How much does SR-22 insurance cost in SC?

SR-22 insurance in SC usually costs an additional $25-$50 for filing, with monthly premiums starting around $100, depending on driving history and coverage.

What is SR-22 insurance in Arizona?

Arizona SR-22 insurance is a certificate filed by your insurer to prove you carry the state's required liability coverage after violations like DUIs or license suspensions.

How much is SR-22 insurance in VA?

SR-22 insurance in VA typically costs $50 for the filing fee, and monthly premiums, depending on your provider and driving record, average $120- $150.

Regardless matter the amount of coverage you need, our free comparison tool can help you find the best rates.

What is the average cost of SR-22 insurance in Alaska?

The average cost of SR-22 insurance in Alaska is approximately $135 per month, depending on the driver's record and insurance provider.