Best SR-22 Car Insurance in 2026

SEE FULL RANKINGS IN YOUR STATE

NATIONAL RANKINGS

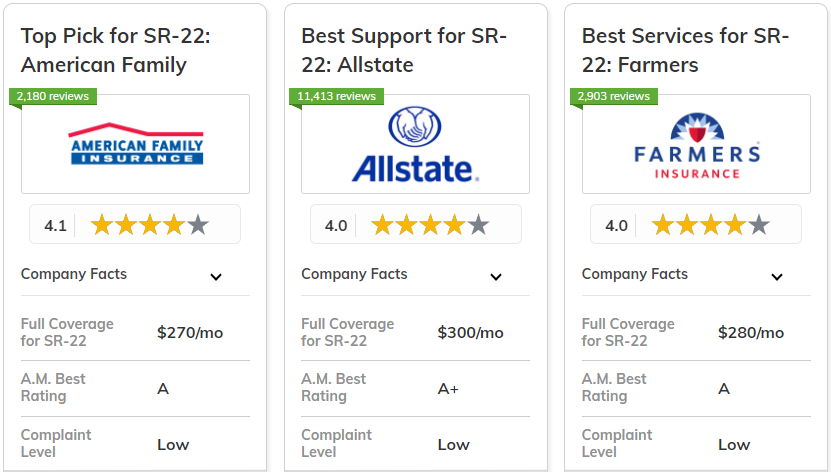

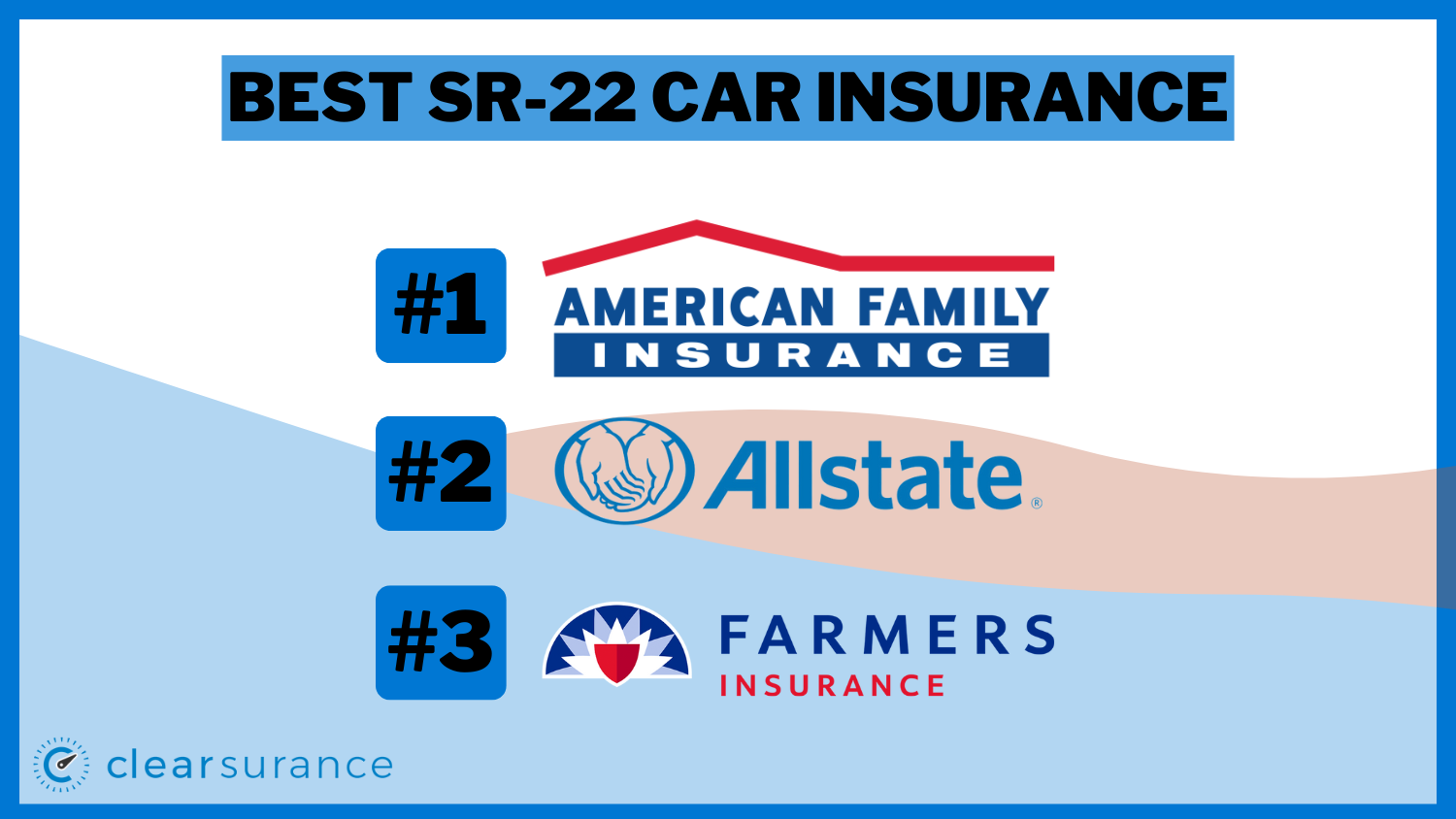

American Family, Allstate, and Farmers are the best SR-22 car insurance providers, with rates as low as $120 per month. American Family offers a bundling discount of 25% that is unique, along with stable rates over the long term for SR-22 policyholders.

Allstate offers a full range of educational resources and ensures prompt SR-22 filings, while Farmers stands out with tailored service and the option to cover multiple vehicles with SR-22.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 25% | A | Customer Loyalty | American Family | |

| #2 | 25% | A+ | Comprehensive Support | Allstate | |

| #3 | 20% | A | Personalized Service | Farmers | |

| #4 | 25% | A++ | Affordable Rates | Geico | |

| #5 | 25% | A | Customizable Options | Liberty Mutual | |

| #6 | 20% | A+ | Broad Network | Nationwide | |

| #7 | 10% | A+ | Extensive Discounts | Progressive | |

| #8 | 17% | B | Reliable Coverage | State Farm | |

| #9 | 13% | A++ | Flexible Policies | Travelers | |

| #10 | 10% | A++ | Military Focus | USAA |

SR-22 insurance is a form of proof required for high-risk drivers. This offers guidance on securing the best SR-22 car insurance. (Read More: Best Car Insurance for High-Risk Drivers)

Ready to find cheaper car insurance coverage? Enter your ZIP code above to begin.

What You Should Know

- American Family offers a 25% bundling discount and stable rates

- Allstate excels in accurate SR-22 filings for high-risk drivers

- Farmers provides personalized service and flexible SR-22 coverage

#1 – American Family: Top Overall Pick

Pros

- Long-Term SR-22 Rate Stability: American Family offers consistent pricing, benefiting long-term SR-22 customers.

- Loyalty Rewards for SR-22 Drivers: Provides exclusive benefits for long-term SR-22 policyholders.

- Loyalty-Based SR-22 Removal Assistance: Helps loyal customers transition away from SR-22 requirements.

Cons

- Potential for Strict Underwriting: SR-22 drivers may face additional scrutiny or limitations.

- Possible Higher Fees: SR-22 filing costs might be higher. Read our detailed review of American Family car insurance.

#2 – Allstate: Best for Comprehensive Support

Pros

- Comprehensive SR-22 Education Resources: Allstate offers detailed information to help drivers understand SR-22 requirements.

- Guaranteed SR-22 Filing Accuracy: Ensures timely and accurate SR-22 filings. Learn more in our Allstate car insurance review.

- Accident Forgiveness for SR-22 Drivers: Some SR-22 drivers may qualify for accident forgiveness programs.

Cons

- May Lack Specialized SR-22 Support Teams: SR-22 customers may not have access to high-risk insurance experts.

- Possible Higher SR-22 Filing Fees: Allstate might charge more for SR-22 processing than some competitors.

#3 – Farmers: Best for Personalized Service

Pros

- SR-22 Policy Customization: Farmers offers tailored coverage options for specific SR-22 requirements.

- Multi-Vehicle SR-22 Coverage: Suitable for SR-22 drivers with multiple cars. Check our Farmers car insurance review.

- Periodic SR-22 Rate Reassessment: Reviews rates to potentially lower premiums for responsible drivers.

Cons

- Potential for Slower SR-22 Verification: Delays in SR-22 filing or confirmation may occur.

- Possible Restrictions on SR-22 Policy Adjustments: Changes to coverage may be challenging for SR-22 holders.

#4 – Geico: Best for Affordable Rates

Pros

- Recommended for SR-22: Geico’s among the car insurance companies that customers recommend for SR-22 coverage.

- Potential for SR-22 Discounts: Various discount programs help offset higher high-risk premiums.

- Gradual SR-22 Rate Improvement: Safe driving can lead to reduced premiums over time.

Cons

- Potential for Limited SR-22 Coverage Options: SR-22 policyholders may have fewer customization options.

- Possible Higher SR-22 Down Payments: Initial costs for SR-22 policies might be steeper than others.

#5 – Liberty Mutual: Best for Customizable Options

Pros

- SR-22 Coverage Options: They offer multiple coverage choices for high-risk drivers. You can find more details in this car insurance review of Liberty Mutual.

- Multi-Vehicle SR-22 Policies: Ideal for SR-22 filers needing coverage for multiple vehicles.

- SR-22 Education Resources: Provides comprehensive information on SR-22 requirements.

Cons

- Potential for Slower SR-22 Processing: Some customers may experience delays in SR-22 filings.

- Complex SR-22 Terms: Policy language could be confusing for some high-risk drivers.

#6 – Nationwide: Best for Broad Network

Pros

- SR-22 Specialist Agents: They offer specialists in handling SR-22 insurance needs. Discover more in our Nationwide car insurance review.

- Consistent SR-22 Availability: Provides SR-22 coverage across different states for high-risk drivers.

- SR-22 Removal Assistance: Offers guidance on transitioning away from SR-22 when eligible.

Cons

- May Lack Specialized SR-22 Programs: Some insurers offer more tailored options for specific SR-22 needs.

- Possible Restrictions on SR-22 Adjustments: Making policy changes may be challenging for SR-22 holders.

#7 – Progressive: Best for Extensive Discounts

Pros

- SR-22 Bundling Discounts: Combining SR-22 with other policies can lead to significant savings.

- Name Your Price SR-22 Tool: Helps drivers find affordable SR-22 coverage based on budget. (Read More: Progressive Car Insurance Review)

- Snapshot Program for SR-22 Drivers: Safe driving could lower rates through usage-based insurance.

Cons

- Automated SR-22 Handling: Some drivers may prefer more personalized support for high-risk needs.

- Limited SR-22 Forgiveness Programs: Fewer options for improving rates after SR-22 status.

#8 – State Farm: Best for Reliable Coverage

Pros

- Comprehensive SR-22 Coverage: Offers a broad range of policy options for high-risk SR-22 drivers.

- Drive Safe & Save for SR-22 Drivers: Our State Farm car insurance review mentioned usage-based insurance could lower rates for safe drivers.

- Flexible SR-22 Payment Plans: Multiple payment options to help manage SR-22 costs.

Cons

- Limited Online SR-22 Tools: Fewer digital features for managing SR-22 policies online.

- May Lack Specialized SR-22 Support Teams: No dedicated experts for complex high-risk situations.

#9 – Travelers: Best for Flexible Policies

Pros

- Adjustable SR-22 Policy Terms: Travelers offers flexible policy lengths to meet state mandates.

- Flexible SR-22 Payment Structures: Offers multiple payment plan options. (Learn More: Travelers Car Insurance Review.

- Adaptable Coverage Limits: Allows drivers to adjust coverage limits as their circumstances change.

Cons

- Possible Overpayment Risk: Customization options could lead to choosing more coverage than needed.

- Limited Standardized SR-22 Packages: Fewer simple, pre-designed policy options for ease of choice.

#10 – USAA: Best for Military Focus

Pros

- Lowest SR-22 Pricing: USAA’s $210 rate is the most affordable for high-risk drivers. Read more in our USAA car insurance review.

- Military-Focused SR-22 Expertise: Tailored support for SR-22 filers with military backgrounds.

- Personalized SR-22 Support: USAA provides individualized assistance for complex SR-22 situations.

Cons

- Higher SR-22 Filing Fees: Administrative costs may be higher despite low premiums.

- Longer SR-22 Verification Times: Processing SR-22 filings could take longer than with competitors.

Understanding SR-22 Insurance

SR-22 insurance refers to the need for an SR-22 form filed with your state by your auto insurance company, proving you have the required liability coverage due to legal violations. (Read More: What does liability car insurance cover?)

While not a different type of insurance, SR-22 coverage indicates high-risk status, potentially limiting your insurance options and increasing costs. Not all companies provide SR-22 insurance, but those that do, like those listed on Clearsurance, will file the form on your behalf.

How Much Does SR-22 Insurance Cost

An SR-22 will likely affect your car insurance coverage and cost. The SR-22 form itself may not cost you much, if anything, depending on your state. But your car insurance rates are affected by it. High-risk drivers tend to pay the highest car insurance rates, but the cost of car insurance can vary by company and by state. The table below shows a comparison of monthly car insurance rates for minimum and full coverage.

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $175 | $300 | |

| $155 | $270 | |

| $165 | $280 | |

| $125 | $225 | |

| $185 | $320 | |

| $170 | $285 | |

| $145 | $250 | |

| $135 | $235 | |

| $180 | $305 | |

| $120 | $210 |

There are many other factors that go into the cost of SR-22 insurance such as your age, gender, location, credit score, vehicle type, marital status and so on. Insurance companies also consider the length of time since the incident that made it necessary. If you maintain a clean driving record for a certain period, it will matter less, especially when your state drops the requirement.

Rate data Clearsurance examined shows car insurance rates increase by over $1,200 after a DUI on average. It can be important to shop around after you've had a DUI. You can see the average car insurance rates after a DUI for the 10 largest car insurance companies on our blog.

Situations Requiring SR-22 Insurance

Proof of insurance with SR-22s is required after you've committed certain violations with the law. You may even be required to have an SR-22 if you've had a series of small violations within a short span of time. You could need SR22 insurance for the following reasons:

- Conviction for driving under the influence (DUI or DWI)

- Driving without insurance or with a suspended/revoked license

- Multiple traffic violations or numerous at-fault accidents

- Fatal or injury-causing at-fault accidents, reckless driving

- Court orders, unpaid fines, or refusing breathalyzer tests

Typically, a high-risk driver will need to file an SR-22 with the state every year for three years. However, some states require it for a longer time period as SR-22 requirements vary by state. Minimum requirements for your coverage can also vary by state.

These eight states don't have SR22 insurance requirements: Delaware, Kentucky, Minnesota, New Mexico, New York, North Carolina, Oklahoma and Pennsylvania.

These states may have other requirements and/or forms. If you're facing serious restrictions, make sure to talk to someone at your local DMV to understand exactly what liability insurance is required.

If you move from a state that requires an SR-22 and were required to file one to a state that doesn't require it, you may still need to file the form depending on the laws of the state you're moving from.

What to Do When Your SR-22 Filing Period Ends

Insurance companies typically don't check your driving record every cycle due to the expense. If you don’t switch insurers, they might not notice new accidents, but your policy will still reflect SR-22 requirements until you prove otherwise. After fulfilling SR-22 requirements, you must file an SR-26 form to indicate you no longer need it, potentially lowering your rates.

If your rates don't drop, review your coverage. An SR-26 is also required if your SR-22 policy is canceled or not renewed. Failing to complete the SR-22 period can result in needing a new insurer or starting over.

Difference Between an SR-22 and an FR-44

An FR-44 is similar to an SR-22 form but is required in specific instances in certain states. Like the SR-22, the FR-44 is a form of financial responsibility that you may be required to file by your state or the court.

It guarantees to your state that you have the required amount of car insurance. Also like an SR-22 form, an FR-44 form must be filed by your car insurance company. The FR-44 form is only used in Florida and Virginia.

data-media-max-width="560">Are you or do you know a senior driver? If you are looking to improve your driving while also saving money, consider taking a defensive driving course. Read all the ways you can save here! ➡️ https://t.co/5b0jmSJ8xd #OlderDriverSafetyAwarenessWeek #Seniors #Savings #Driving 👵 pic.twitter.com/e1a1OOV9CV

— Clearsurance (@clearsurance) December 8, 2021

An FR-44 is often called “DUI Insurance” because it's required if you've been convicted of a DUI or DWI. For more information, read our article titled "How Long Does a DUI Stay on Your Record?". The difference between an FR-44 and an SR-22 is that an FR-44 requires higher liability limits on drivers' car insurance policies than the SR-22 requires.

How Car insurance Rates are Calculated

When comparing car insurance quotes, it can be frustrating to understand how rates are calculated. While there’s no exact formula, insurers consider factors such as your driving record, mileage, location, age, marital status, car details, credit history, and coverage amount. Note that some states prohibit using gender or credit score in rate calculations.

Read More:

Ways to Save Money on Your Car Insurance

While you never want to sacrifice quality to save a couple of dollars, there are some different ways you can lower your car insurance premium Here are six ways you may be able to lower your car insurance rates by bundling policies, raising deductibles, paying in full, using usage-based insurance, monitoring price changes, and shopping for better rates.

A usage-based insurance program uses a telematics device or mobile app on your phone to monitor your driving habits. When you drive safely, you are rewarded with a discount on your insurance rates. Other common discounts include the safe driver discount, multi-policy discount (for bundling), good student discount, and multi-vehicle discount.

Many auto insurers also offer a discount for certain safety features on your vehicle, like anti-lock brakes and daytime running lights. Below is a table highlighting the discounts offered by some of the top insurance companies, helping you find the best savings for your coverage.

| Insurance Company | Available Discount |

|---|---|

| Safe Driver, Multi-Policy, Early Signing, Anti-Theft | |

| Good Driver, Multi-Vehicle, Loyalty, Defensive Driving | |

| Bundling, Good Student, Pay-in-Full, Anti-Theft | |

| Multi-Policy, Good Driver, Military, Anti-Theft | |

| Multi-Policy, Safe Driver, Homeowner, Paperless Billing | |

| Multi-Policy, Good Student, Accident-Free, Defensive Driving | |

| Multi-Policy, Snapshot Program, Homeowner, Continuous Insurance | |

| Safe Driver, Multi-Policy, Good Student, Accident-Free | |

| Multi-Policy, Safe Driver, Homeowner, New Car | |

| Safe Driver, Multi-Policy, Military, Defensive Driving |

Experts recommend you get at least three auto insurance quotes before you choose a policy. Make sure to take the discounts each company offers into consideration when you're looking at quotes.

Finding cheap car insurance quotes is easy. Just enter your ZIP code into our free comparison tool below to instantly compare quotes near you.

Frequently Asked Questions

How do you get SR-22 insurance?

To get SR22 insurance, you'll need to contact your car insurance company. An SR-22 can only be obtained through an insurance carrier; you can't complete it on your own. If your auto insurance company offers insurance coverage to drivers who need an SR-22, your company can file the form with your state and offer you car insurance coverage. Depending on your state, you may also be able to submit your SR-22 form by mail or by delivering it in person.

If your company doesn't offer insurance coverage to drivers who need an SR-22, you'll need to switch to a car insurance company that does. Enter your zip code in the filters to see companies offering SR22 insurance in your state.

If you don’t have a car but need your license reinstated, you’ll need non-owner SR-22 insurance. While this is similar to standard SR-22 insurance, the difference is that a non-owner policy only provides liability coverage, but it won’t cover damage to the car you’re driving. That coverage falls under the responsibility of the car’s owner. In order to get a non-owner SR-22 policy, you can’t own a car or have one in your household that you regularly drive.

Where can you get SR-22 insurance quotes?

You can use Clearsurance to get SR-22 insurance quotes. Fill out the filters on this page to view a list of the best companies that offer SR22 insurance in your area. You can sort through companies and find the ones you want to get quotes from. To get quotes, click on the orange “Click for quote” button next to the company, call the number available or visit the company's website.

If you need SR22 insurance, you may want to consider shopping for a new insurance company, even if your current company will insure you with an SR-22. The filing of an SR-22 form will almost always lead to a car insurance rate increase and rates for SR-22 insurance vary by company. You can shop around by requesting car insurance quotes from multiple companies and comparing the quotes to see which company offers you the best coverage for the best price.

What is the best car insurance for SR-22?

The best car insurance companies for SR-22 depends on your needs, but companies like American Family, Geico, and Progressive offer competitive rates and reliable service for high-risk drivers. These insurers handle SR-22 filings and provide support to help you manage the requirements.

What age is car insurance most expensive?

Car insurance is typically most expensive for drivers aged 16-25, with rates peaking around age 16 due to inexperience and higher accident risk. Rates generally begin to decrease after age 25.

See if you’re getting the best deal on car insurance by entering your ZIP code below.

What age is insurance the cheapest?

Insurance becomes cheaper for drivers starting at age 25 and continues to decline into middle age. Drivers in their 30s and 40s generally benefit from the lowest car insurance rates, provided they have a clean driving record.

Read More: Best Car Insurance Companies that Decrease Rates After You Turn 21

What is the best age to get car insurance?

The best age to get car insurance is in your mid-20s, when rates tend to drop significantly. At this age, drivers have gained experience and may qualify for lower premiums, particularly if they maintain a clean driving record.

How long do you need to carry an SR-22?

You typically need to carry an SR-22 for about three years, though the duration can vary depending on state laws and the severity of the violation that required the SR-22 in the first place.

How do I find out when my SR-22 expires?

You can find out when your SR-22 expires by checking your state's Department of Motor Vehicles (DMV) records or contacting your insurance company. They can inform you of the expiration date and assist with any necessary filings.

What states don’t require an SR-22?

The following eight states don’t require SR-22 insurance: Delaware, Kentucky, Minnesota, New Mexico, New York, North Carolina, Oklahoma, and Pennsylvania. However, they may have alternative requirements for high-risk drivers.

Read More:

How much is SR-22 insurance per month?

SR-22 insurance can increase premiums by $50 to $100 per month on top of standard rates. On average, monthly rates range from $125 to $300, but this varies based on your location, driving history, and insurer.

Does SR-22 insurance cover any car that I drive?

Yes, SR-22 insurance typically covers any car you drive, as long as you maintain continuous coverage. If you have a non-owner SR-22 policy, it only provides liability coverage when you're driving a vehicle you don't own.

How do I find out when my SR-22 expires?

To check when your SR-22 expires, contact your insurance provider or your state's DMV. They can provide the expiration date and confirm if any further actions are required before your SR-22 filing is complete.

Shop for the best liability-only car insurance with our free quote comparison tool. Enter your ZIP code below to begin.

Frequently Asked Questions

How do you get SR-22 insurance?

To get SR22 insurance, you'll need to contact your car insurance company. An SR-22 can only be obtained through an insurance carrier; you can't complete it on your own. If your auto insurance company offers insurance coverage to drivers who need an SR-22, your company can file the form with your state and offer you car insurance coverage. Depending on your state, you may also be able to submit your SR-22 form by mail or by delivering it in person.

If your company doesn't offer insurance coverage to drivers who need an SR-22, you'll need to switch to a car insurance company that does. Enter your zip code in the filters to see companies offering SR22 insurance in your state.

If you don’t have a car but need your license reinstated, you’ll need non-owner SR-22 insurance. While this is similar to standard SR-22 insurance, the difference is that a non-owner policy only provides liability coverage, but it won’t cover damage to the car you’re driving. That coverage falls under the responsibility of the car’s owner. In order to get a non-owner SR-22 policy, you can’t own a car or have one in your household that you regularly drive.

Where can you get SR-22 insurance quotes?

You can use Clearsurance to get SR-22 insurance quotes. Fill out the filters on this page to view a list of the best companies that offer SR22 insurance in your area. You can sort through companies and find the ones you want to get quotes from. To get quotes, click on the orange “Click for quote” button next to the company, call the number available or visit the company's website.

If you need SR22 insurance, you may want to consider shopping for a new insurance company, even if your current company will insure you with an SR-22. The filing of an SR-22 form will almost always lead to a car insurance rate increase and rates for SR-22 insurance vary by company. You can shop around by requesting car insurance quotes from multiple companies and comparing the quotes to see which company offers you the best coverage for the best price.

What is the best car insurance for SR-22?

The best car insurance companies for SR-22 depends on your needs, but companies like American Family, Geico, and Progressive offer competitive rates and reliable service for high-risk drivers. These insurers handle SR-22 filings and provide support to help you manage the requirements.

What age is car insurance most expensive?

Car insurance is typically most expensive for drivers aged 16-25, with rates peaking around age 16 due to inexperience and higher accident risk. Rates generally begin to decrease after age 25.

See if you’re getting the best deal on car insurance by entering your ZIP code below.

What age is insurance the cheapest?

Insurance becomes cheaper for drivers starting at age 25 and continues to decline into middle age. Drivers in their 30s and 40s generally benefit from the lowest car insurance rates, provided they have a clean driving record.

Read More: Best Car Insurance Companies that Decrease Rates After You Turn 21

What is the best age to get car insurance?

The best age to get car insurance is in your mid-20s, when rates tend to drop significantly. At this age, drivers have gained experience and may qualify for lower premiums, particularly if they maintain a clean driving record.

How long do you need to carry an SR-22?

You typically need to carry an SR-22 for about three years, though the duration can vary depending on state laws and the severity of the violation that required the SR-22 in the first place.

How do I find out when my SR-22 expires?

You can find out when your SR-22 expires by checking your state's Department of Motor Vehicles (DMV) records or contacting your insurance company. They can inform you of the expiration date and assist with any necessary filings.

What states don’t require an SR-22?

The following eight states don’t require SR-22 insurance: Delaware, Kentucky, Minnesota, New Mexico, New York, North Carolina, Oklahoma, and Pennsylvania. However, they may have alternative requirements for high-risk drivers.

Read More:

How much is SR-22 insurance per month?

SR-22 insurance can increase premiums by $50 to $100 per month on top of standard rates. On average, monthly rates range from $125 to $300, but this varies based on your location, driving history, and insurer.

Does SR-22 insurance cover any car that I drive?

Yes, SR-22 insurance typically covers any car you drive, as long as you maintain continuous coverage. If you have a non-owner SR-22 policy, it only provides liability coverage when you're driving a vehicle you don't own.

How do I find out when my SR-22 expires?

To check when your SR-22 expires, contact your insurance provider or your state's DMV. They can provide the expiration date and confirm if any further actions are required before your SR-22 filing is complete.

Shop for the best liability-only car insurance with our free quote comparison tool. Enter your ZIP code below to begin.