Best and Cheapest Renters Insurance in 2026

SEE FULL RANKINGS IN YOUR STATE

NATIONAL RANKINGS

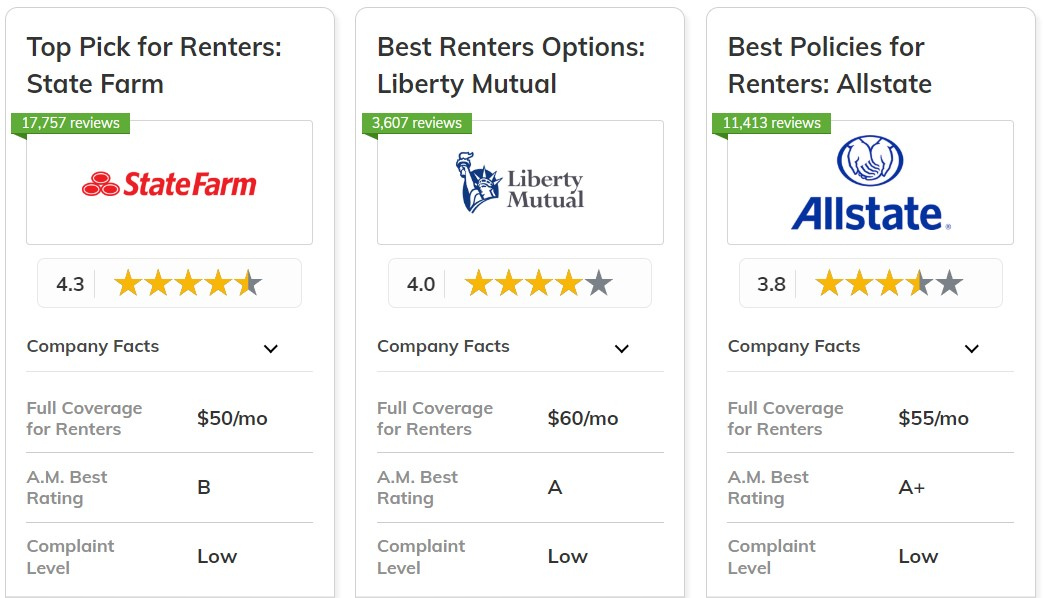

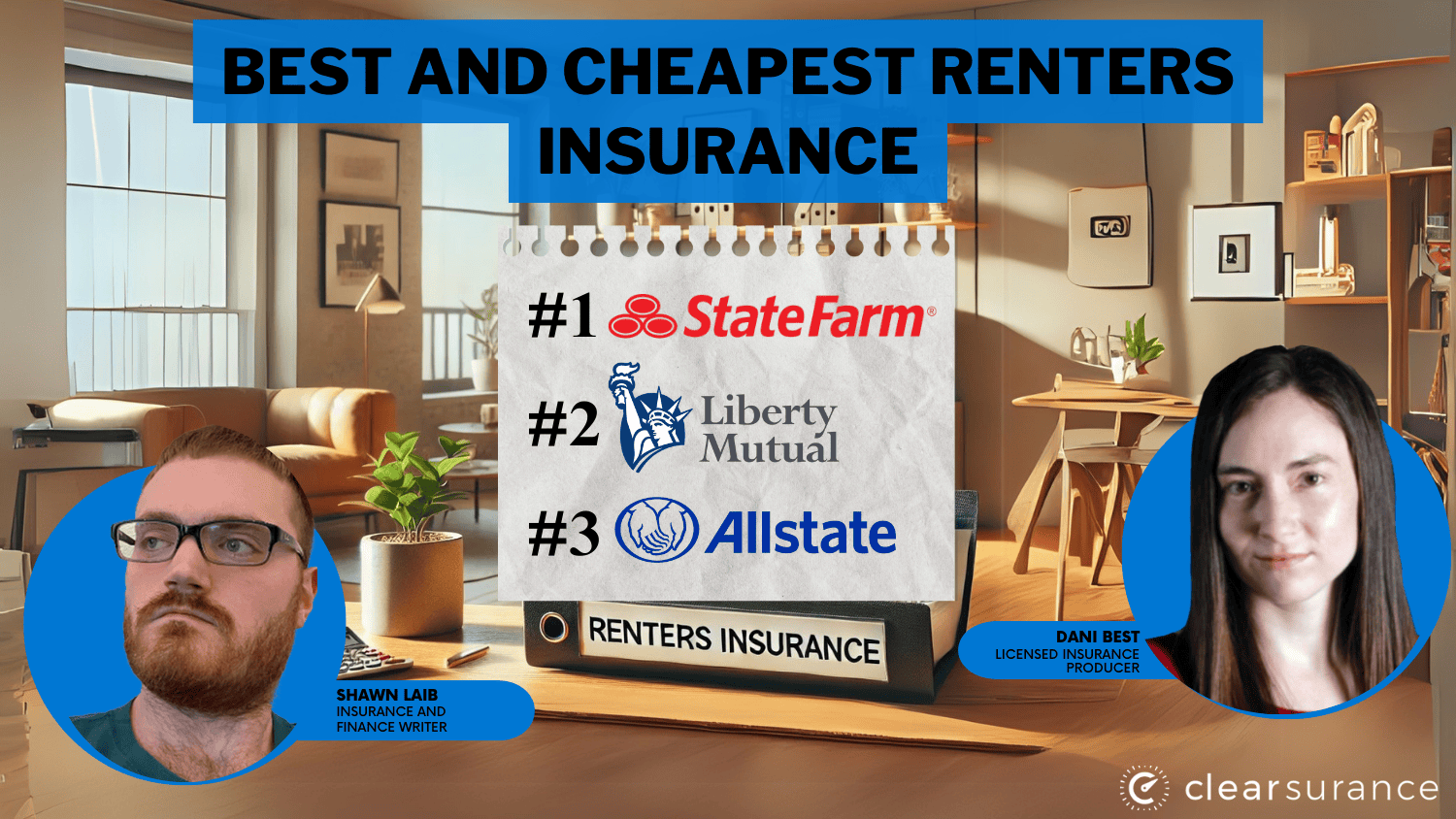

The best and cheapest renters insurance comes from State Farm, Liberty Mutual, and Allstate, with rates starting as low as $15/month. State Farm is great for affordable policies and claims-free discounts.

Liberty Mutual stands out for its customizable plans and 25% bundling discount, while Allstate offers personalized coverage and strong financial support. Getting low-cost renters insurance is easier than ever.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 17% | B | Claims Free | State Farm | |

| #2 | 25% | A | Policy Options | Liberty Mutual | |

| #3 | 25% | A+ | Customized Policies | Allstate | |

| #4 | 10% | A++ | Military Service | USAA | |

| #5 | 20% | A+ | Multi-Policy | Nationwide | |

| #6 | 25% | A++ | Good Credit | Geico | |

| #7 | 10% | A+ | Quote Advance | Progressive | |

| #8 | 20% | A | Paperless Billing | Farmers | |

| #9 | 13% | A++ | Early Quote | Travelers | |

| #10 | 15% | A | Loyalty Discount | Safeco |

Coverage limits, deductibles, and available discounts can lower your premium even more. Compare these top companies today to protect your belongings for less. Secure cheap insurance by entering your ZIP code into our free quote comparison tool.

What You Should Know

- Find the best and cheapest renters insurance with rates starting at just $15/month

- State Farm is the top pick for affordable policies and claims-free discounts

- Compare coverage, deductibles, and discounts to save on renters insurance premiums

#1 – State Farm: Top Overall Pick

Pros

- Claims-Free Discounts: State Farm gives renters savings for having no past claims.

- Low Rates: Renters can get minimum coverage starting at $23/month.

- Bundling Savings: Renters can save up to 17% by bundling insurance policies.

Cons

- Lower Bundling Discount: The bundling discount is less compared to other insurers.

- Average Financial Rating: State Farm has a lower financial rating than some competitors.

#2 – Liberty Mutual: Best for Policy Options

Pros

- Custom Options: Renters can adjust policies to fit their personal needs.

- Affordable Rates: Minimum coverage starts at $30/month for renters.

- Big Discounts: Renters can bundle insurance and save up to 25%. Read our Liberty Mutual review to learn more.

Cons

- Higher Base Prices: Without discounts, renters may pay higher starting rates.

- Limited Claims-Free Benefits: Discounts for a clean claims record are minimal.

#3 – Allstate: Best for Customized Policies

Pros

- Custom Coverage: Renters can add coverage options to fit their needs.

- Good Rates: Minimum coverage starts at $28/month for renters.Explore more in our Allstate review.

- Strong Financial Rating: Allstate has a top financial rating, ensuring claims get paid.

Cons

- Higher Premiums Without Discounts: Rates can be high if renters don’t qualify for discounts.

- Few Loyalty Rewards: Long-term renters get fewer loyalty benefits.

#4 – USAA: Best for Military Service

Pros

- Exclusive Benefits: USAA offers special renters coverage for military families.

- Lowest Rates: Minimum coverage starts at $15/month for renters. Delve into our USAA review.

- Top Financial Rating: USAA has a top financial rating for paying claims on time.

Cons

- Membership Needed: Only military members and their families can qualify.

- Not for Civilians: Non-military renters can’t use USAA for coverage.

#5 – Nationwide: Best for Multi-Policy

Pros

- Bundling Deals: Renters can save up to 20% by combining policies. For a comprehensive list, refer our Nationwide review.

- Reasonable Rates: Minimum renters insurance starts at $25/month.

- Trusted Company: Nationwide has a top financial rating for reliability.

Cons

- No Bundling Means Higher Prices: Without bundling, renters may face higher rates.

- Fewer Claims-Free Rewards: Discounts for no claims are limited.

#6 – Geico: Best for Good Credit

Pros

- Credit-Based Discounts: Renters with good credit get better rates. (Learn more: 32 Genius Ways to Save Money).

- Low Prices: Minimum renters insurance starts at $20/month.

- Wide Coverage Options: Extra coverage choices are available for renters.

Cons

- Fewer Local Agents: Renters may have fewer in-person service options.

- Standard Claims Discounts: Claims-free savings aren’t as big as some competitors’.

#7 – Progressive: Best for Quote Advance

Pros

- Early Quote Deals: Renters save by getting quotes ahead of time.

- Budget-Friendly Rates: Minimum coverage starts at $22/month for renters.

- Policy Bundles: Renters can combine auto and renters insurance for extra savings which covered in our Progressive review.

Cons

- Higher Rates Without Discounts: Without bundles, prices may be higher.

- Limited Custom Plans: Renters looking for highly personalized plans may need add-ons.

#8 – Farmers: Best for Paperless Billing

Pros

- Paperless Savings: Renters get discounts for managing policies online.

- Fair Prices: Minimum renters insurance starts at $24/month, see our Farmers review for detailed insight.

- Policy Bundles: Renters can bundle auto and renters insurance for savings.

Cons

- Fewer Custom Plans: Custom coverage options are limited.

- Higher Costs After Claims: Renters who file claims may face increased prices.

#9 – Travelers: Best for Early Quote

Pros

- Early Quote Deals: Renters save when getting a quote before their policy starts.

- Competitive Prices: Minimum coverage starts at $26/month for renters.

- Loyalty Rewards: Long-term renters get discounts over time. Check out our Travelers review.

Cons

- Limited Custom Choices: Renters may need extra coverage for full protection.

- Higher Starting Rates: Initial prices can be higher without discounts.

#10 – Safeco: Best for Loyalty Discount

Pros

- Loyalty Savings: Long-term renters earn loyalty discounts (Read more: Safeco Review).

- Good Prices: Minimum coverage starts at $27/month for renters.

- Flexible Coverage: Various coverage options are available for renters.

Cons

- Limited Online Quotes: Some renters must call agents for price quotes.

- Fewer Discounts: Safeco has fewer savings options compared to competitors.

Basic Renters Insurance Costs

Renters insurance is often much cheaper than car or homeowners insurance, with average rates around $185 per year, or about $15 per month, according to the Insurance Information Institute. Compared to homeowners insurance, which averages $1,192 per year or $100 per month, renters insurance is a cost-effective way to protect your belongings. Here’s a breakdown of monthly renters insurance rates based on minimum and full coverage options:

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $28 | $55 | |

| $24 | $54 | |

| $20 | $45 | |

| $30 | $60 | |

| $25 | $52 | |

| $22 | $51 | |

| $27 | $58 | |

| $23 | $50 | |

| $26 | $56 | |

| $15 | $40 |

Renters insurance costs less because it doesn’t cover the structure of your apartment—that’s your landlord’s responsibility. Instead, renters insurance covers your personal belongings, liability, and additional living expenses. This limited coverage makes it more affordable while still providing essential protection (Read more: Why Do Landlords Require Renters Insurance?).

For instance, consider how much it would cost to replace your electronics, furniture, and clothes after a fire or theft. Without renters insurance like Lemonade, you’d have to cover those expenses yourself. In contrast, affordable policies from the best companies for renters insurance, such as State Farm, Geico, or Liberty Mutual, provide peace of mind at a low monthly cost.

To get the best inexpensive renters insurance, compare providers, adjust your coverage limits, and explore discounts like bundling policies or paying annually. If you're unsure where to start, check the best renters insurance reviews on trusted sites like site:clearsurance.com Lemonade for honest customer experiences. Whether you need renters insurance for one month or long-term coverage, exploring top providers ensures the best protection for your valuables.

For personalized coverage comparisons, consider popular matchups like State Farm vs Lemonade Renters Insurance or browse providers offering the cheapest renters insurance in PA or best renters insurance in Florida for tailored rates. Investing in renters insurance today could save you thousands in the long run.

Ways to Get the Best Renters Insurance

Finding the best renters insurance is essential to protect your personal belongings and save money. Start by comparing policies from the best renter insurance companies based on customer reviews, coverage options, and pricing. Whether you're looking for cheap renter insurance or the best inexpensive renters insurance, consider both affordability and quality of service.

| Insurance Company | Available Discount |

|---|---|

| Multi-Policy, Claims-Free, Home Safety Devices, Paperless | |

| Multi-Policy, Smoke Alarms/Security System, Good Credit, Claim-Free, Loyalty | |

| Multi-Policy, Claims-Free, Early Shopper, Online Purchase, Home Safety Devices | |

| Multi-Policy, Claims-Free, Home Safety Devices, Paperless, Loyalty | |

| Multi-Policy, Quote in Advance, Safety Devices, Claims-Free | |

| Multi-Policy, Protective Devices (Alarms), Claims-Free, Home Renovation, Loyalty | |

| Multi-Policy, Claims-Free, Home Alert Protection (Security Devices), Loyalty | |

| Multi-Policy, Protective Device, Claims-Free, Green Home, Early Quote | |

| Multi-Policy (Bundling With Auto Insurance), Claims-Free, Loyalty, Safety Devices | |

| Multi-Policy, Claims-Free, Home Safety Devices, Paperless |

Many of the best companies for renters insurance offer valuable discounts such as bundling home and auto policies, installing safety devices, and maintaining a claims-free history. If you’re searching for renters insurance like Lemonade, note that it provides a user-friendly digital experience with customizable policies.

Renters insurance rates vary by location. If you’re in states like North Carolina (cheapest renters insurance NC), Texas (best renters insurance Texas), Florida (best renters insurance Florida), Arkansas (best renters insurance Arkansas), Virginia (best renters insurance Virginia), or Hawaii (best renters insurance Hawaii), comparing local providers ensures you get tailored coverage at a competitive price.

To secure the best cheap renters insurance, compare quotes from multiple companies. Look for policies with low monthly premiums, strong financial ratings, and top customer reviews. Best rated renters insurance providers like Nationwide, Progressive, and USAA stand out for reliability and customer service. Visiting company websites helps you learn about their available discounts, coverage options, and real customer experiences.

Read more: Top ways customers say they've saved money on renters insurance

Top Renters Insurance Options for College Students

Whether college students need renters insurance depends on where they live during school. Students living in on-campus dorms usually don’t need separate renters insurance because their parents’ homeowners insurance often covers their belongings. If this applies to you, check with your parents’ insurance provider to confirm coverage.

For students living off-campus in apartments, renters insurance is essential. It covers valuable items like laptops, TVs, furniture, and textbooks in case of theft, fire, or other damages. Check out our guide about the top 17 questions to ask about apartments before you rent).

To save money, consider companies that offer both renters and auto insurance if you own a car. Many insurers provide good student discounts, helping you get affordable coverage while protecting your personal items and vehicle. Compare quotes from top-rated companies to find the best renters insurance policy that fits your budget and needs.

Factors Affecting Renters Insurance Rates

The cost of renters insurance varies based on several factors unique to each person. Your actual rate could be higher or lower depending on where you live, your coverage needs, and other personal details (Learn more: Does renters insurance cover storage units?

For example, a renter with $25,000 in personal property coverage and a $1,000 deductible will likely pay less than someone with $50,000 in coverage and a $500 deductible. Understanding what affects your rate can help you choose the right policy and save money. Here are the key factors insurance companies consider when determining your renters insurance premium:

- Coverage Amount: More coverage means higher premiums.

- Type of Coverage: Policies with extra features cost more.

- Deductible Amount: A higher deductible lowers your monthly premium.

- Location: Living in areas with higher crime or weather risks raises rates.

- Building Type: Newer, safer buildings cost less to insure.

- Credit Score (in some states): Better credit can lower your insurance rate.

- Claims History: A clean claims record helps keep premiums low.

That’s why getting a customized insurance quote is essential to find the best deal. By knowing these factors, you can adjust your coverage choices and get the best renters insurance policy for your budget.

Coverage Details of Renters Insurance

A standard renters insurance policy, also called an HO-4 policy, protects your personal belongings against specific risks, known as “perils.” If your items are damaged or stolen due to one of these covered events, your insurance company will reimburse you up to your policy's coverage limit after you pay a deductible.

Renters insurance typically covers 16 common perils that can cause damage to your personal belongings. These include theft, which protects against stolen items, and fire or lightning, covering damage from unexpected fires or lightning strikes. Windstorms or hail are also included, offering protection against severe weather damage. In case of an explosion or riots or civil commotion, renters insurance will pay for losses caused by such events.

Damage from aircraft or vehicles is covered if a car or airplane hits your home. Smoke damage and vandalism or malicious mischief are included to protect against smoke-related issues or intentional damage. Additional perils such as falling objects, volcanic eruptions, and the weight of ice, snow, or sleet ensure coverage in extreme natural events.

Water damage from plumbing or appliances, sudden system failures like heating or fire sprinklers, and freezing of pipes or appliances are also protected. Lastly, renters insurance covers power surges causing damage, ensuring financial protection from sudden electrical failures. Many renters insurance policies also offer some sort of additional liability coverage and medical payments for a non-resident's accident that occurs on your rental property.

- Liability Protection: Covers legal costs if someone gets hurt or property damage while visiting your rental home. Typical limits start at $100,000, though higher limits are available.

- Medical Payments: Pays for medical expenses if a guest gets injured in your home, regardless of who’s at fault.

- Loss of Use Coverage: Helps pay for temporary living expenses if your rental becomes unlivable due to a covered peril, like a fire or flood.

These extra coverages are optional but can be valuable, especially if you own expensive items or want extra peace of mind. Consider adding them based on your specific needs.

Strategies for Finding Cheap Renters Insurance

Finding cheap renters insurance is easier than you might think, especially since renters insurance is already more affordable than car or homeowners insurance. The best way to get a low rate is by comparing quotes from multiple companies. Start by getting free online quotes to see which providers offer the best deals. Be sure to compare similar coverage options and limits to ensure you’re making a fair comparison. Saving money shouldn’t mean sacrificing quality service or essential coverage.

Many renters insurance companies offer discounts that can lower your premium. For example, bundling your renters insurance with your car insurance can earn you a multi-policy discount. Staying claims-free for several years can also reduce your rates. Additionally, if your rental unit has safety features like smoke detectors, carbon monoxide alarms, or a home security system, you could qualify for extra savings. Living in a gated community may also help you get a lower rate.

You can further reduce your renters insurance costs by raising your deductible, which lowers your monthly premium. Consider reviewing your personal property’s value and adjusting your coverage limits if needed. Paying your policy in full instead of monthly can also result in a small discount. Compare quotes from the cheapest home insurance companies by entering your ZIP code into our free tool.

How to save money on your renters insurance

While renters insurance may be more affordable than other types of insurance, no one wants to pay more than they have to. So what are the different ways that you can lower your renters insurance premium and have some extra spending money?

Here are the top 5 ways to save on your renters insurance:

- Raise your deductible

- Ask about potential discounts

- Bundle your policies

- Determine the value of your personal property

- Pay in full by check

How we rank renters insurance companies

Wondering how Clearsurance determines scores for insurance companies? Our algorithm analyzes a range of inputs from our community of unbiased insurance customers, including:

- Cost

- Customer Service

- Overall Experience

- Claim service

- Purchasing experience

- Likelihood to recommend

Guide to understanding renters insurance

As we mentioned above, there’s common misconceptions regarding what is and isn’t covered by a renters insurance policy. Before you purchase a policy, it’s best to understand what your policy covers. For example, did you know that many renters insurance policies include liability protection in the event a non-resident is injured on the property. Plus, if your apartment becomes uninhabitable from an incident, some policies may cover your expenses as you find temporary housing.

We want to make sure you’re equipped with a proper knowledge of renters insurance, so check out our practical guide to understanding renters insurance. Looking for more educational information about renters insurance? Check out our blog for more information and topics related to renters insurance.

Frequently Asked Questions

What is the difference between actual cash value (ACV) and replacement cost coverage in renters insurance?

ACV pays for the depreciated value of your belongings at the time of loss, while replacement cost coverage reimburses the full cost of replacing items with new ones. Replacement cost coverage typically costs more but provides better financial protection.

Read more: Homeowners insurance vs. renters insurance

Does renters insurance cover accidental damage to a neighbor's property?

Yes, renters insurance includes liability coverage that can cover accidental damage you cause to a neighbor’s property. For example, if a plumbing issue in your unit causes water damage to the unit below, your policy may cover repair costs. Learn more relevant guide titled "What does renters insurance NOT cover?"

Can I get renters insurance if I share an apartment with roommates?

Yes, but it’s usually better for each roommate to have their own renters insurance policy. Sharing a policy can cause disputes over claims and limit coverage if one person moves out. Some insurers allow roommates to be listed, but this option is less common. The best place to start when you want affordable renters insurance is to enter your ZIP code into our free comparison tool.

Does renters insurance cover hotel stays if my apartment becomes unlivable?

Yes, renters insurance often includes "loss of use" or "additional living expenses" coverage. If a covered event like a fire makes your apartment unlivable, your policy can pay for temporary accommodations such as hotel stays and related expenses.

Is renters insurance required by law?

No, renters insurance is not legally required, but many landlords require tenants to carry a policy as part of the lease agreement. Even if it’s not mandatory, renters insurance is a smart way to protect your belongings and avoid costly out-of-pocket expenses.

What natural disasters does renters insurance cover?

Standard renters insurance covers common disasters like fire, lightning, windstorms, and hail. However, events like floods and earthquakes are usually excluded. If you live in a high-risk area, consider purchasing separate flood or earthquake insurance. Visit our guide titled "A Practical Guide for Understanding Renters Insurance."

How does renters insurance handle stolen items outside my home?

Most renters insurance policies cover theft even when it happens outside your home. For example, if your laptop is stolen from your car or while traveling, your policy may reimburse you, subject to coverage limits and deductibles.

Can I adjust my renters insurance policy after I buy it?

Yes, renters insurance policies are flexible and can be adjusted at any time. You can increase or decrease coverage limits, add additional insured individuals, or update your deductible if your needs change during the policy term.

How much liability coverage should I include in my renters insurance policy?

Most renters policies come with $100,000 in liability coverage by default, but you may want to increase this amount if you have significant assets or frequently host guests. Higher liability limits provide better financial protection in case of lawsuits or large claims. Don’t wait until it’s too late – enter your ZIP code into our free renters insurance comparison tool to find affordable coverage today.

Is Lemonade renters insurance a good option for first-time renters?

Yes, Lemonade renters insurance is a popular choice for first-time renters due to its easy online application process, fast claims payouts, and affordable rates. Its app-driven platform makes managing policies simple, and coverage starts as low as $5/month, depending on your location and coverage needs. Lemonade also donates unused premiums to charitable causes through its Giveback program, making it an appealing option for socially conscious renters.

Read more: Why do customers rate Lemonade Insurance so highly?