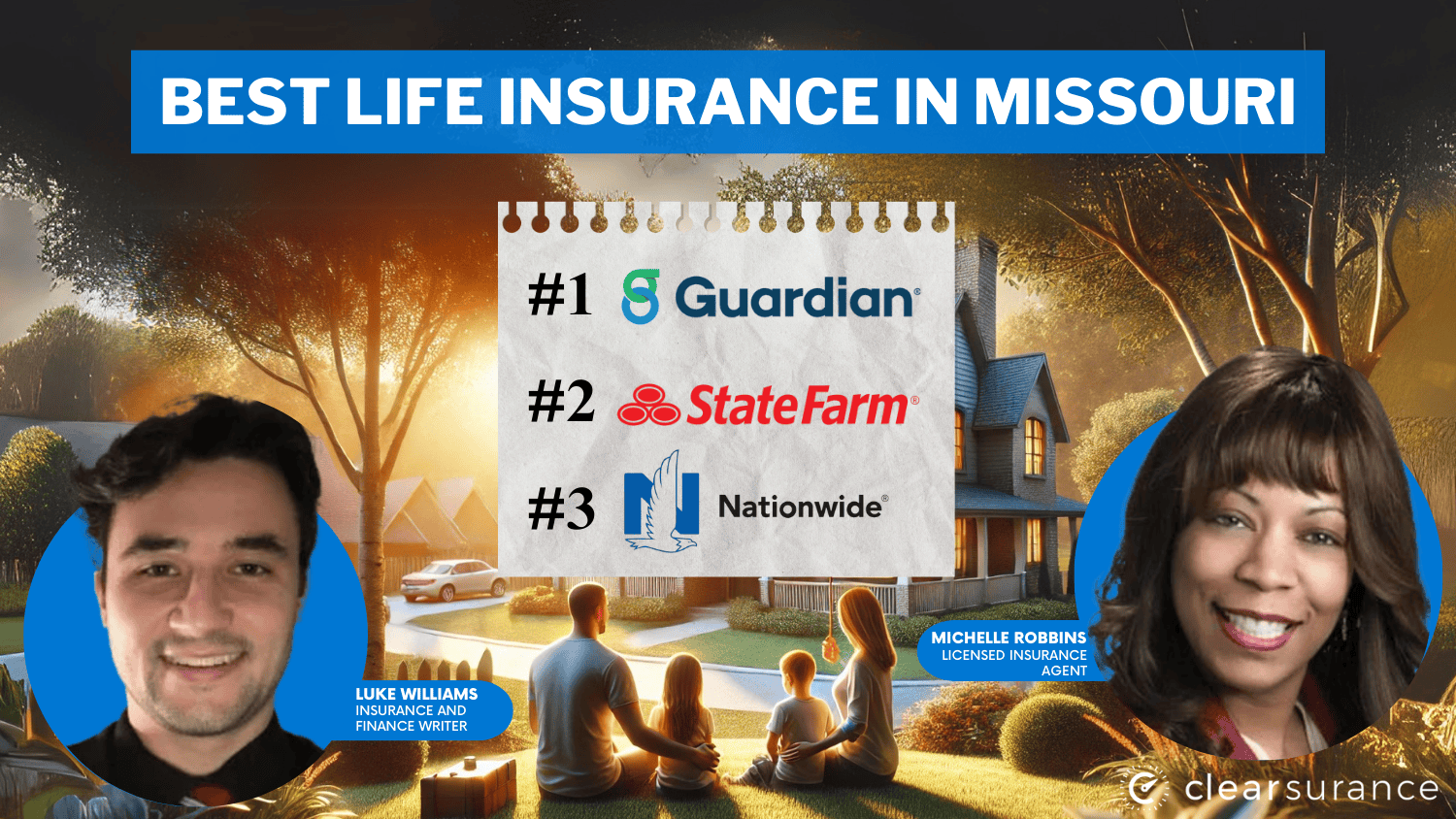

Best Life Insurance in Missouri for 2026 (Top 10 Companies Ranked)

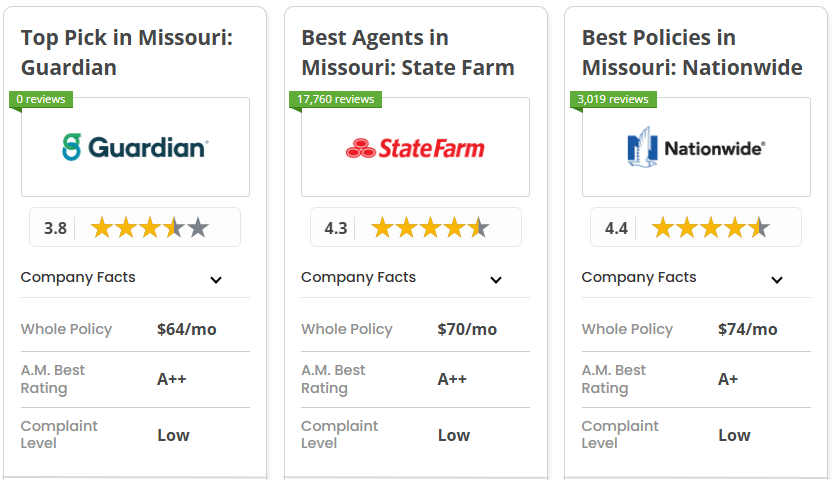

With $26 per month rates on term policies and an 11% bundling discount, Guardian offers the best life insurance in Missouri, followed by State Farm and Nationwide.

Guardian leads with an A++ rating and high customer satisfaction, making it excellent for individuals looking for financial stability. State Farm offers a 17% bundling discount, an extensive agent network providing personalized service.

| Company | Rank | Bundling Discount | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 11% | A++ | Customer Satisfaction | Guardian Life | |

| #2 | 17% | B | Agent Network | State Farm | |

| #3 | 20% | A+ | Affordable Policies | Nationwide | |

| #4 | 4% | A+ | Affordable Rates | Mutual of Omaha | |

| #5 | 13% | A+ | Wide Coverage | Prudential | |

| #6 | 6% | A++ | Customizable Policies | MassMutual | |

| #7 | 6% | A+ | Reliable Options | Transamerica | |

| #8 | 5% | A+ | Estate Planning | Pacific Life | |

| #9 | 10% | A+ | Financial Stability | Lincoln | |

| #10 | 10% | A+ | Vitality Program | John Hancock |

Nationwide stands out with A+ financial strength, affordable term policies, and flexible coverage options, making it the most budget-friendly choice. Entering your ZIP code into our tool will provide you with free quotes from the best life insurance companies.

What You Should Know

- Guardian ranks top pick with an A++ rating and strong customer satisfaction

- Get affordable life insurance in Missouri with rates starting at $24 per month

- Nationwide offers the best healthy lifestyle discount for 28%

#1 – Guardian Life: Top Overall Pick

Pros

- Exceptional Financial Strength: Guardian Life holds an A++ rating and is backed by over 160 years of industry experience, making it one of the most financially stable life insurance providers in Missouri.

- Competitive Bundling Discount: Offers a 20% discount for customers who bundle their life insurance in Missouri with other policies like disability or dental insurance.

- High Claim Payout Ratio: With a 97% claim approval rate, Guardian ensures beneficiaries receive Missouri life insurance in payouts quickly.

Cons

- Fewer No-Exam Policy Options: Guardian offers limited no-medical-exam life insurance in Missouri, requiring most applicants to undergo full underwriting compared to competitors with simplified issue policies.

- Limited Digital Access: Lacks an interactive online quote tool, requiring direct contact with an agent to buy life insurance in Missouri. Discover how much life insurance costs and find the best plan for your needs.

#2 – State Farm: Best Agent Network

Pros

- Largest Agent Network: With 18,000+ licensed agents nationwide, State Farm offers personalized service for life insurance in Missouri customers who prefer face-to-face interactions.

- Significant Bundling Savings: Provides a 17% bundling discount when combining life insurance in Missouri with home or auto policies. See a list of discounts in our State Farm review.

- Diverse Policy Selection: Offers term, whole, and universal life policies with flexible term lengths of 10, 20, and 30 years, ensuring tailored life insurance solutions in Missouri.

Cons

- Few Customization Options: State Farm life insurance in Missouri offers fewer riders than its competitors.

- No Instant Online Quotes: Customers must schedule an appointment with an agent to receive personalized life insurance in Missouri at the same price as competitors offering instant digital quotes.

#3 – Nationwide: Best for Healthy Lifestyles

Pros

- Wide Range of Coverage Options: Nationwide provides term, whole, and universal life insurance in Missouri, with customizable plans to meet a variety of financial needs.

- Best Healthy Living Discount Available: You can save 28% on your Missouri life insurance premiums by quitting smoking, eating healthy, and exercising regularly.

- Strong Financial Backing: Holds an A+ rating, proving its ability to pay Missouri life insurance claims reliably. Discover more about offerings in our Nationwide insurance review.

Cons

- Limited Whole Life Options: Primarily focuses on term policies, with fewer permanent life insurance plans in Missouri compared to MassMutual or Prudential.

- Lengthy Underwriting Process: Approval for life insurance in Missouri can take four to six weeks, particularly for policies requiring a medical exam.

#4 – Mutual of Omaha: Best for Affordable Rates

Pros

- Affordable Coverage: Life insurance in Missouri can be purchased for as low as $25 a month, making it a great choice for budget-conscious buyers.

- Financially Stable: With an A+ rating, the company has a long history of timely claim payment.

- No Medical Exam Option: Simplified issue life insurance in Missouri allows applicants to skip the medical exam for coverage up to $250,000. Explore affordable solutions for securing higher-risk life insurance.

Cons

- Minimal Bundling Discount: Offers only a 4% discount, significantly lower than other life insurance companies in Missouri.

- Higher Whole Life Premiums: Whole life insurance rates start at $62 per month, higher than Lincoln’s $60 per month for similar coverage.

#5 – Prudential: Best for Wide Coverage

Pros

- $10 Million in Coverage: Prudential is one of the few insurers offering life insurance policies exceeding $1 million, ideal for high-income earners in Missouri.

- Lenient Underwriting for Health Issues: More forgiving for conditions like diabetes, high blood pressure, and asthma, leading to higher approval rates for Missouri life insurance.

- Best Variable Universal Life (VUL) Selection: Policyholders can invest in over 50 mutual fund options, giving Missouri residents more control over policy growth.

Cons

- Expensive Permanent Life Policies: A $1 million universal life policy starts at $380 monthly, which is more costly than similar coverage from MassMutual or Pacific Life. Get more rates in our Prudential review.

- Stricter Requirements for Large Policies: Missouri applicants must provide full financial disclosure, including verification of net worth, for coverage over $5 million.

#6 – MassMutual: Best for Dividend Payouts

Pros

- Highest Dividend Payouts: Policyholders receive annual dividends, which can be used to lower premiums or reinvest in Missouri life insurance.

- A++ Financial Strength: One of the most financially sound organizations, providing long-term stability to Missouri policyholders.

- Flexible Universal Life Plans: Allows partial withdrawals and premium adjustments, making it highly adaptable for Missouri residents. Discover the steps involved in buying life insurance for someone else today.

Cons

- High Initial Whole Life Costs: Premiums for $250,000 whole life policies start at $380 per month, which is more expensive than Guardian or Nationwide in Missouri.

- Limited No-Medical Exam Options: Only offers simplified issues for the whole life, up to $50,000, restricting accessibility for Missouri seniors.

#7 – Transamerica: Best for Reliable Options

Pros

- Affordable Term Coverage: Offers $250,000 term policies for $27 per month, making it a budget-friendly option for Missouri life insurance.

- Best High-Risk Applicant Approval Rates: More likely to approve applicants in Missouri with pre-existing conditions like hypertension or cancer. Compare more companies that offer hybrid life insurance/long-term care policies.

- Longer Term Lengths Available: Offers 40-year term policies, uncommon among other Missouri life insurance providers.

Cons

- Minimal Agent Support: Primarily online-based, leading to fewer in-person agent consultations in Missouri.

- Higher Whole Life Costs for Seniors: A $250,000 whole life policy in Missouri costs $370 per month, exceeding Nationwide’s $350 monthly.

#8 – Pacific Life: Best for Estate Planning

Pros

- Top Choice for High-Net-Worth Individuals: Specializes in wealth transfer policies, protecting beneficiaries from Missouri estate taxes.

- Competitive Second-to-Die Policies: This company offers survivorship life insurance that covers two people under one policy, ideal for Missouri couples.

- Strong Financial Strength Rating: With over 150 years of financial stability and an A+ rating from A.M. Best, Pacific Life guarantees dependable Missouri life insurance payouts.

Cons

- Not Ideal for Small Policies: Most coverage options start at $250,000, making it less accessible for Missouri low-income families. Discover how to find affordable health insurance that fits your budget today.

- Expensive Term Policies: A $250,000 term life insurance policy in Missouri starts at $29 per month, higher than Nationwide’s $24 monthly.

#9 – Lincoln Financial: Best for Term Life

Pros

- Highly Rated for Financial Strength: Maintains an A+ rating, proving its ability to pay large death benefits on time, with a claim approval rate of 98% within 60 days for life insurance in Missouri.

- Lowest Term Life Premiums: Offers $24 per month term life insurance in Missouri. Explore what happens if you outlive your term life insurance and what steps you can take next.

- Moderate Bundling Discounts: Offers customers a 10% discount when they combine Missouri life insurance with Lincoln's annuity or disability products.

Cons

- Limited Term Coverage Lengths: Only offers 10-, 15-, and 20-year terms, restricting options for Missouri applicants who need longer coverage.

- Higher Whole Life Premiums: Whole life policies start at $60 per month, making them more expensive than Guardian's in Missouri.

#10 – John Hancock: Best for Vitality Program

Pros

- Premium Discounts for Healthy Habits: Policyholders can earn up to 15% in premium savings through the Vitality Program in Missouri.

- Excellent Financial Strength Rating: A.M. Best awards an A+ rating, confirming long-term financial security and claim reliability for Missouri life insurance policyholders.

- Innovative Wellness Integration: Policyholders receive free Fitbits and Apple Watches, tracking health to unlock life insurance in Missouri discounts. Explore top options for the best life insurance companies that offer discounts for being healthy.

Cons

- Premiums Higher for Passive Policyholders: Those not engaging with the Vitality Program pay higher Missouri life insurance premiums.

- Whole Life Rates Start Higher Than Competitors: A $250,000 whole life policy starts at $375 per month, which is higher than Pacific Life's $360 in Missouri.

Missouri Life Insurance Rates From Top Providers

For those seeking an affordable term life insurance policy, Lincoln offers the lowest rate at $24 per month, followed by Mutual of Omaha at $25. When it comes to whole-life coverage, Lincoln again stands out at $60 per month, making it the cheapest option.

| Insurance Company | Term Policy | Whole Policy |

|---|---|---|

| $26 | $64 | |

| $32 | $76 | |

| $24 | $60 | |

| $31 | $75 | |

| $25 | $62 | |

| $30 | $74 | |

| $29 | $71 | |

| $33 | $78 | |

| $28 | $70 | |

| $27 | $67 |

However, the best life insurance companies in Missouri — Guardian, State Farm, and Nationwide — offer more than just low rates. Guardian’s A++ financial rating and 20% bundling discount provide long-term security. State Farm’s 17% bundling discount and strong agent network give policyholders access to personalized support. Nationwide combines affordability with flexibility, offering term life at $30 per month plus a 20% bundling discount.

While Lincoln and Mutual of Omaha are great for low-cost coverage, Guardian, State Farm, and Nationwide offer a solid mix of competitive pricing, strong benefits, and long-term reliability. Shopping around and comparing Missouri life insurance quotes is the best way to find a policy that fits your budget and needs.

Top Life Insurance Discounts Available in Missouri

Bundling, healthy lifestyle incentives, employer-sponsored plans, and auto-pay discounts are ways for Missourians to reduce the cost of life insurance. Each insurer offers a different savings percentage, so it's critical to compare options before choosing a policy.

| Insurance Company | Bundling | Healthy Lifestyle | Group/Employer | Auto-Pay |

|---|---|---|---|---|

| 10% | 28% | 12% | 15% | |

| 20% | 30% | 12% | 16% | |

| 12% | 30% | 10% | 14% | |

| 20% | 28% | 18% | 14% | |

| 25% | 22% | 20% | 20% | |

| 18% | 27% | 22% | 19% | |

| 22% | 25% | 15% | 18% | |

| 15% | 20% | 10% | 12% | |

| 17% | 18% | 12% | 15% | |

| 10% | 29% | 14% | 12% |

MassMutual offers the greatest policy bundling discount of 25%, which considerably reduces expenses when paired with other coverage. Pacific Life is a close second with 22%, making it an excellent choice for anyone looking to save for many policies. Healthy lifestyle discounts peak at 30% with Guardian and John Hancock, rewarding policyholders for maintaining wellness through fitness tracking and medical exams.

Mutual of Omaha leads in employer-sponsored discounts at 22%, benefiting employees enrolled in group life insurance. MassMutual leads in auto-pay savings at 20%.

Comprehensive Life Insurance Coverage Options in Missouri

There are various types of life insurance available in Missouri, each intended to satisfy particular monetary requirements. Knowing your alternatives enables you to make the best decision, whether you're searching for investment-based insurance, everlasting security, or reasonably priced temporary coverage.

The most affordable type of life insurance is term, which has lower premiums and provides coverage for a predetermined amount of time. A whole life insurance policy's cash value ensures future financial security. Flexibility is increased by universal life insurance, which permits changes to death benefits and premiums.

| Insurance Company | Universal | Indexed Universal | Guaranteed Issue | Variable | AD&D |

|---|---|---|---|---|---|

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ❌ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ❌ | ✅ | ❌ | ✅ | |

| ✅ | ✅ | ❌ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ❌ | ✅ |

Indexed universal life ties cash value growth to market performance and provides a guaranteed minimum return to safeguard against losses. Variable life insurance allows policyholders to invest cash value in mutual funds, which provide greater risk and growth potential. Modified life insurance is another choice, with lower beginning premiums that rise over time, making it perfect for those expecting increased salaries.

Nationwide, John Hancock, Lincoln, MassMutual, Prudential, and Transamerica offer all five policy types for comprehensive coverage. Guardian and Pacific Life lack guaranteed issue options, which may limit access for high-risk applicants. Mutual of Omaha and State Farm doesn't offer variable life, restricting investment growth opportunities. Nationwide ensures stability with indexed universal life, while Prudential stands out with strong mutual fund investment choices. Mutual of Omaha is a top choice for easy approval without a medical exam.

Affordable Life Insurance Options in Missouri

Life insurance premiums in Missouri vary according to the provider and policy type. Understanding life insurance classifications aids in selecting the appropriate plan, whether it is term life for affordability, whole life for long-term security, or universal life for variable premiums. Final expense and guaranteed issue policies provide options for those needing simplified coverage.

| Insurance Company | Term Policy | Whole Policy | Universal Life | Final Expense | Guaranteed Issue |

|---|---|---|---|---|---|

| $26 | $64 | $50 | $45 | $40 | |

| $32 | $76 | $48 | $42 | $38 | |

| $24 | $60 | $47 | $41 | $37 | |

| $31 | $75 | $49 | $43 | $39 | |

| $25 | $62 | $46 | $39 | $36 | |

| $30 | $74 | $45 | $40 | $35 | |

| $29 | $71 | $51 | $46 | $41 | |

| $33 | $78 | $52 | $47 | $42 | |

| $28 | $70 | $53 | $48 | $43 | |

| $27 | $67 | $44 | $38 | $34 |

If you're looking for the cheapest term life insurance, Lincoln has the lowest rate at $24 per month, followed by Mutual of Omaha at $25. For whole life, Lincoln is also the most budget-friendly at $60 per month. But the best life insurance options in Missouri aren't just about cost—Guardian, State Farm, and Nationwide offer strong financial backing and added perks.

Guardian provides universal life at $50 and final expense at $45, making it a solid all-around option. State Farm has universal life at $53 per month, which is great for long-term flexibility. Nationwide offers the lowest guaranteed issue rate at $35 per month, perfect for those who need no-medical-exam coverage.

Top-Ranked Life Insurance Companies in Missouri

The companies with the best life insurance in Missouri are Guardian, State Farm, and Nationwide. With an impressive A++ rating and a 20% bundle discount, Guardian is a great option for people who are combining policies.

State Farm provides a 17% bundling discount and whole-life policies starting at $70 monthly, ensuring solid protection with in-person agent support. Nationwide offers the lowest term life rate at $24 per month and a 20% bundling discount, making it the most affordable option.

Pricing is important when choosing life insurance in Missouri, but so are policy advantages, coverage alternatives, and financial stability. Read through our ultimate life insurance guide to explore flexible coverage options, stability, and bundling discounts before using our free comparison tool to compare quotes.

Frequently Asked Questions

What is the average monthly cost of life insurance in Missouri?

Missouri's average monthly cost of life insurance varies by provider and policy type. Still, term policies start around $24 per month, while whole-life plans typically range from $60 to $78 monthly.

How much life insurance do you need in Missouri?

Determining how much life insurance you need in Missouri depends on your annual income, outstanding debts, mortgage, dependents, and future expenses like college tuition or retirement for your spouse. Most experts recommend 10–15 times your income for adequate coverage.

How much per month is a million-dollar life insurance policy in Missouri?

Missouri's million-dollar life insurance policy typically costs between $50 and $300 per month, depending on age, health, policy duration, and term or whole life insurance. Term policies are cheaper, while whole-life plans are more expensive due to cash value accumulation.

Is life insurance more expensive in Missouri?

Yes, life insurance in Missouri can be higher than the national average due to state-specific health trends, insurance regulations, and market demand. However, rates vary based on age, lifestyle, and policy type, with term policies often being more affordable.

What are the factors that impact the cost of life insurance in Missouri?

Age, health, tobacco use, coverage type, and occupation affect costs. A 35-year-old non-smoker in Missouri may pay around $30 per month for a $250K term policy, while a smoker could pay up to 50% more.

Which company offers the best life insurance policy in Missouri?

Guardian, State Farm, and Nationwide are Missouri's top choices for life insurance. They offer strong financial ratings, competitive discounts, and flexible coverage options.

What is the best type of life insurance policy to have in Missouri?

The best type of life insurance policy in Missouri depends on your needs and the life stages that affect your insurance needs; term life is more affordable, while whole life provides lifelong coverage with cash value growth.

Which is better, term or whole life insurance?

Whole life insurance provides lifetime protection with cash value accumulation, whereas term life insurance is less expensive and best suited for short-term coverage.

If you need life insurance coverage, use our free comparison tool to save time and money.

Can you cash out a life insurance policy?

You can cash out a whole life insurance policy through loans, withdrawals, or surrendering the policy, but term life policies have no cash value.

Can I purchase life insurance in Missouri without a medical exam?

Yes, many insurers in Missouri offer no-medical-exam life insurance, including guaranteed issue and simplified issue policies for faster approval.

Which Missouri life insurance company denies the most claims?

Claim denials depend on policy exclusions and non-disclosure; insurers may deny claims due to fraud, missed payments, or undisclosed medical conditions.

What happens if you outlast your term life insurance?

Unless you renew, switch to a permanent policy, or buy a new plan, your term life insurance coverage expires if you outlive it.

Does State Farm offer cash-value life insurance in Missouri?

Yes, State Farm offers whole life insurance policies that build cash value. If the policyholders have sufficient cash value, they can borrow against or withdraw funds through the automatic premium loan provision.

What is the downside of whole life insurance?

Whole life insurance costs significantly more than term life and may provide lower returns than other investment options.

Can you cash out whole life insurance in Missouri?

Missouri policyholders can cash out whole life insurance through withdrawals, loans, or surrendering the policy for its cash value.

How long do you have life insurance before it pays out in Missouri?

Most life insurance policies in Missouri pay out immediately upon death. Still, some have a contestability period of two years, during which the insurer may investigate whether the insurance policy covers your claim or if fraud or misrepresentation occurred.

What voids life insurance payout in Missouri?

A life insurance payout in Missouri can be voided due to fraud, policy lapses, suicide within the contestability period, or material misrepresentation.

Is it better to purchase Missouri life insurance online or through an agent?

Buying life insurance online offers convenience and quick comparisons, especially with digital life insurance companies that offer online quotes while purchasing through an agent provides personalized advice and policy customization.