Best Life Insurance in Minnesota for 2026 (Your Guide to the Top 10 Companies)

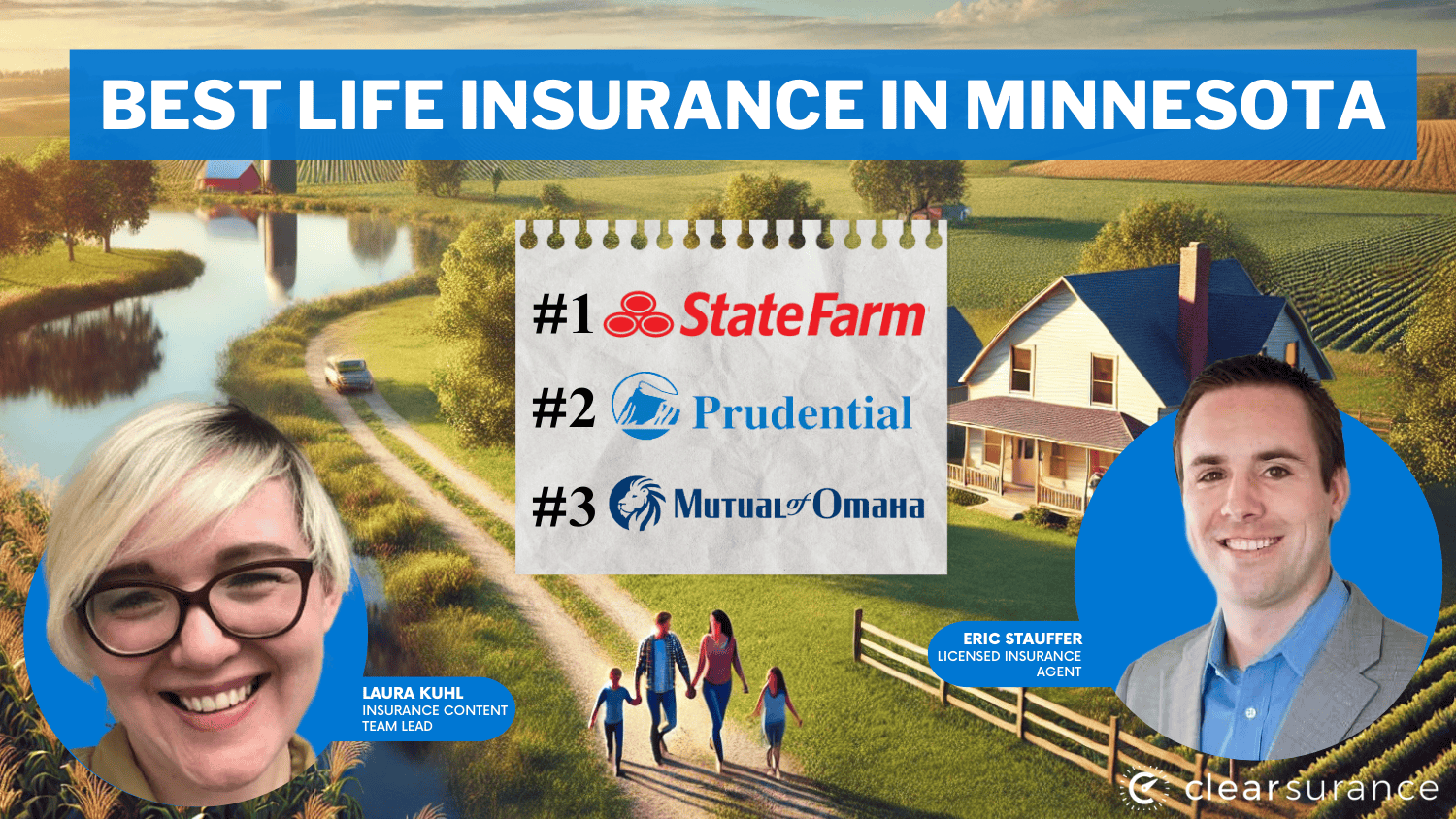

State Farm, Prudential, and Mutual of Omaha offer the best life insurance in Minnesota, standing out in affordability, coverage, and accessibility.

The best life insurance companies in Minnesota balance cost, benefits, and flexibility. State Farm leads with term policy rates at $22 a month and a 17% bundling discount.

| Company | Rank | Bundling Discount | A.M. Best | Best For |

|---|---|---|---|---|

| #1 | 17% | B | Affordable Rates | |

| #2 | 10% | A+ | Strong Coverage | |

| #3 | 7% | A+ | Simplified Plans | |

| #4 | 12% | A++ | Personalized Plans | |

| #5 | 20% | A | Customizable Coverage | |

| #6 | 8% | A | Global Reach | |

| #7 | 10% | A++ | Family Protection | |

| #8 | 18% | A+ | Easy Claims | |

| #9 | 12% | A+ | Flexible Options | |

|

#10 | 5% | A+ | Comprehensive Coverage |

Prudential excels with A+ rated coverage, customizable term lengths, and a 15% healthy lifestyle discount. Mutual of Omaha simplifies underwriting with fast approvals.

Scroll down for more information on these top companies. Use our free tool to compare Minnesota life insurance rates by entering your ZIP code.

What You Should Know

- The average cost of Minnesota life insurance is $30 monthly for term life and $116 a month for whole policies

- State Farm is the top pick, offering $22 term policies and a 17% bundling discount

- Mutual of Omaha offers life insurance in Minnesota with no medical exam

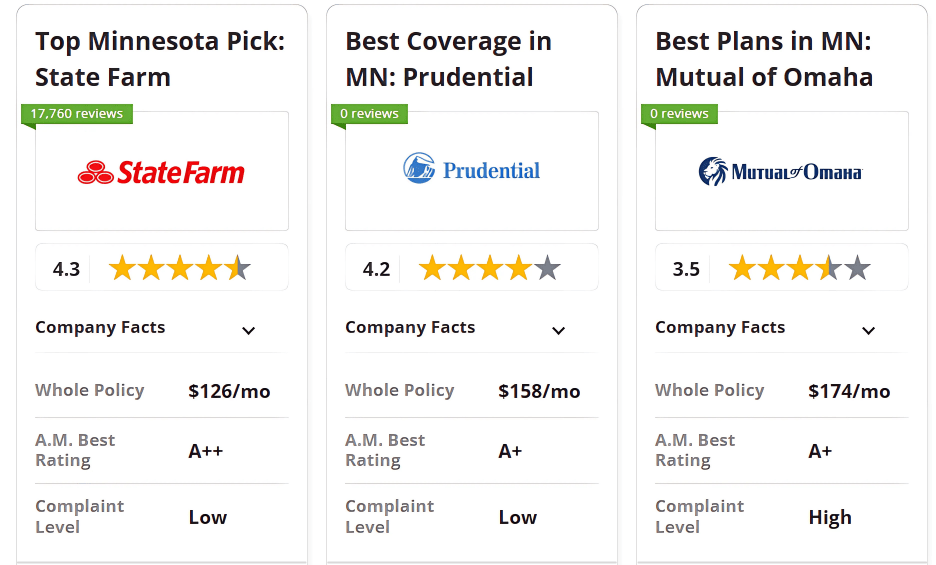

#1 – State Farm: Top Overall Pick

Pros

- Affordable Policies: State Farm offers affordable life insurance in Minnesota with term rates starting at $22 per month, 27% lower than the state average. Learn more in our State Farm review.

- Bundling Discounts: Policyholders can save up to 17% when bundling life insurance in Minnesota with home or auto insurance, reducing total costs by an average of $200 annually.

- Strong Customer Satisfaction: State Farm maintains high policyholder trust with an 88% claim payout success rate and a 4.5-star customer satisfaction rating.

Cons

- Limited Policy Customization: State Farm only offers standard term lengths (10, 20, or 30 years) with no flexible premium structures.

- Higher Whole Life Rates: Whole life insurance in Minnesota through State Farm costs $126 per month, 8% higher than the industry average of $116 monthly for similar coverage.

#2 – Prudential: Best for Strong Coverage

Pros

- Strong Financial Stability: Prudential's life insurance in Minnesota holds an A+ rating from A.M. Best, demonstrating excellent financial strength and claims reliability.

- Customizable Terms: Allows for flexible term lengths and extra riders, including accelerated death benefits and child term coverage.

- Healthy Lifestyle Discounts: Get a 15% discount for policyholders for meeting wellness criteria, including BMI, cholesterol, and blood pressure targets.

Cons

- Higher Term Rates: Prudential's term life insurance in Minnesota starts at $34 per month, 55% more expensive than State Farm's lowest rate. See more details on our Prudential review.

- Limited Bundling Savings: Prudential offers only a 10% discount for bundling, impacting multi-policy savings.

#3 – Mutual of Omaha: Best for Simplified Plans

Pros

- Easy Underwriting: Mutual of Omaha offers life insurance in Minnesota with no medical exam requirements, with approvals in as little as 24 hours for qualified applicants.

- Competitive Term Rates: Provides $41 term plans as a reasonable mid-range option for those wanting basic coverage. Get expert advice on how to find affordable health insurance.

- Long-Term Reliability: Mutual of Omaha has maintained an A+ rating from A.M. Best for over 20 years, ensuring strong financial stability and dependable claims processing.

Cons

- Higher Whole Life Costs: Whole life insurance in Minnesota through Mutual of Omaha costs $174 per month, 15% higher than the industry median.

- Limited Bundling Discounts: Offers only a 7% discount on bundled policies, significantly lower than Farmers and State Farm.

#4 – Northwestern Mutual: Best for Personalized Plans

Pros

- Top-Tier Financial Strength: Northwestern Mutual has earned an A++ rating from A.M. Best, showing top-tier financial security for Minnesota life insurance beneficiaries.

- Highly Customizable: Offers dividend-paying whole life policies in Minnesota, with flexible premiums and unique policy adjustments.

- Reasonable Whole Life Pricing: Whole life insurance starts at $143 per month. Find out how to choose the right policy if you need life insurance now.

Cons

- Limited Term Policy Options: Only fixed-term plans are available, and premium structures are not flexible.

- Lower Bundling Discount: Offers a 12% bundling discount, significantly lower than other Minnesota life insurance companies.

#5 – Farmers: Best for Customizable Coverage

Pros

- Flexible Policy Options: Farmers' Minnesota life insurance provides several riders, including accidental death compensation and critical sickness coverage.

- Bundling Discount: Offers the greatest bundling discount at 20%, resulting in significant long-term savings.

- Affordable Term Policies: Minnesota term life insurance rates begin at $25 per month.

Cons

- Limited Digital Tools: Shopping for Famers life insurance online is not as convenient as other companies in Minnesota. Learn more in our Farmers review.

- Higher Whole Life Costs: Whole life insurance with Farmers in Minnesota starts at $119 monthly, 8% above the state average of $110.

#6 – AIG: Best for Global Reach

Pros

- Worldwide Coverage: AIG's life insurance in Minnesota includes international coverage, which is ideal for expatriates and frequent travelers.

- Competitive Term Rates: Term life insurance in Minnesota starts at $38 per month, lower than New York Life's $47 per month.

- Well-Established Provider: AIG has maintained an A rating from A.M. Best for many years. Discover more ratings in our AIG insurance review.

Cons

- Lower Bundling Discounts: Offers only an 8% bundling discount on life insurance in Minnesota, limiting savings chances.

- Higher Whole Life Costs: Whole life insurance in Minnesota begins at $179 per month, which is among the highest premiums in the state.

#7 – New York Life: Best for Family Protection

Pros

- Top Financial Rating: Holds an A++ rating from A.M. Best, demonstrating excellent financial security and claims reliability.

- Family-Oriented Policies: Offers structured payout plans, providing financial security for dependents.

- Convertible Term Policies: Allows term life insurance in Minnesota to be converted to whole life without requiring a medical exam.

Cons

- Higher Monthly Costs: Term life insurance in Minnesota begins at $47 per month, much more expensive than State Farm's $22 monthly rate. Learn how insurance companies make money from premiums.

- Limited Bundling Discounts: Only provides a 10% discount for bundling, making it less cost-effective than Nationwide's 18% discount.

#8 – Nationwide: Best for Easy Claims

Pros

- Simplified Claims Procedure: Nationwide life insurance in Minnesota offers digital claims processing, with a 94% customer satisfaction rating and an average payout time of 5 days.

- Competitive Term Rates: Term life insurance in Minnesota is reasonably priced when compared to many of its rivals, with monthly rates starting at $23.

- 18% Bundling Discount: Provides a higher-than-average bundling discount, helping policyholders save up to $250 annually on multiple insurance products.

Cons

- Moderate Whole Life Rates: Whole life insurance in Minnesota starts at $132 per month, which is higher than Farmers' $119 but lower than Hartford's $138.

- A+ Financial Rating: Slightly lower than Northwestern Mutual and New York Life, though still considered strong by industry standards. Discover more ratings in our Nationwide insurance review.

#9 – Lincoln Financial: Best for Flexible Options

Pros

- Diverse Coverage: Lincoln Financial offers term, whole, and universal life insurance in Minnesota with multiple riders available, including long-term care benefits.

- Bundling Discount: Provides reasonable savings when bundling with other Lincoln Financial policies, leading to up to $180 in annual premium reductions.

- Affordable Term Rates: Term life insurance in Minnesota starts at $36 per month, making it a good mid-tier alternative. Learn how early retirement affects insurance.

Cons

- Higher Whole Life Costs: Whole life insurance in Minnesota begins at $162 per month, making it less affordable than Mutual of Omaha or Prudential.

- Fewer Customization Features: Lincoln offers solid coverage but lacks some of the advanced policy options available from competitors like Northwestern Mutual.

#10 – The Hartford: Best for Comprehensive Coverage

Pros

- Financially Secure: The Hartford has earned an A+ rating from A.M. Best for many years, ensuring consistent life insurance claim payouts.

- Comprehensive Coverage: Provides term, whole, and AD&D insurance in Minnesota, along with a variety of policy options and add-ons such as disability waivers.

- Affordable Term Rates: Term life insurance in Minnesota begins at $26 per month, making it one of the most cost-effective solutions.

Cons

- Lower Bundling Discount: Only a 5% bundling discount is available, significantly lower than State Farm's 17%.

- Higher Whole Life Costs: Whole life insurance in Minnesota starts at $138 per month, which is more expensive than Farmers' $119 rate. Access comprehensive insights into our The Hartford insurance review.

Comparing Minnesota Life Insurance Rates Across Top Providers

Life insurance rates in Minnesota vary a lot, so it's important to balance affordability with good coverage. If you're looking for the cheapest options, State Farm has the most affordable term life insurance policy at $22 per month, while Farmers offers the lowest whole life policy at $119 per month. Nationwide is another excellent option, with a $23 term policy that is only $1 higher than State Farm.

| Insurance Company | Term Policy | Whole Policy |

|---|---|---|

| $38 | $179 | |

| $25 | $119 | |

| $36 | $162 | |

| $41 | $174 | |

| $23 | $132 | |

| $47 | $211 | |

| $29 | $143 | |

| $34 | $158 | |

| $22 | $126 | |

|

$26 | $138 |

Price is not everything. The best Minnesota life insurance plan isn't just about finding the lowest price — it's about choosing a provider that offers the right mix of affordability, reliability, and policy flexibility.

State Farm, Prudential, and Mutual of Omaha stand out for their strong financial backing and extra benefits. Comparing multiple quotes online is the easiest way to find a policy that fits your budget while still giving you great coverage.

Unlocking the Best Life Insurance Discounts in Minnesota

Life insurance doesn't have to break the bank, especially if you take advantage of the correct discounts. Many insurers in Minnesota offer ways to save through bundling, healthy lifestyle perks, employer-based deals, and auto-pay enrollment. Some companies slash costs by as much as 14%, so knowing where to look can mean significant savings.

| Insurance Company | Bundling | Healthy Lifestyle | Group/Employer | Auto-Pay | Automatic Payment |

|---|---|---|---|---|---|

| 10% | 5% | 8% | 6% | 5% | |

| 20% | 5% | 7% | 5% | 10% | |

| 11% | 6% | 9% | 7% | 5% | |

| 9% | 4% | 6% | 5% | 10% | |

| 13% | 5% | 10% | 8% | 10% | |

| 8% | 7% | 9% | 6% | 5% | |

| 10% | 6% | 7% | 5% | 5% | |

| 12% | 8% | 10% | 7% | 5% | |

| 17% | 6% | 8% | 6% | 10% | |

| 11% | 7% | 9% | 7% | 10% |

Farmers and State Farm lead with the highest bundling discounts at 20% and 17%, respectively, giving multi-policyholders the most savings.

When it comes to healthy lifestyle incentives, Prudential stands out with an 8% discount, rewarding policyholders who maintain optimal BMI, cholesterol, and blood pressure levels.

These discounts show that choosing the right insurer means maximizing savings for long-term benefits. However, understanding life insurance classifications also plays a key role in finding the best policy for your budget and needs.

Comparing Minnesota Life Insurance Coverage Options for Maximum Protection

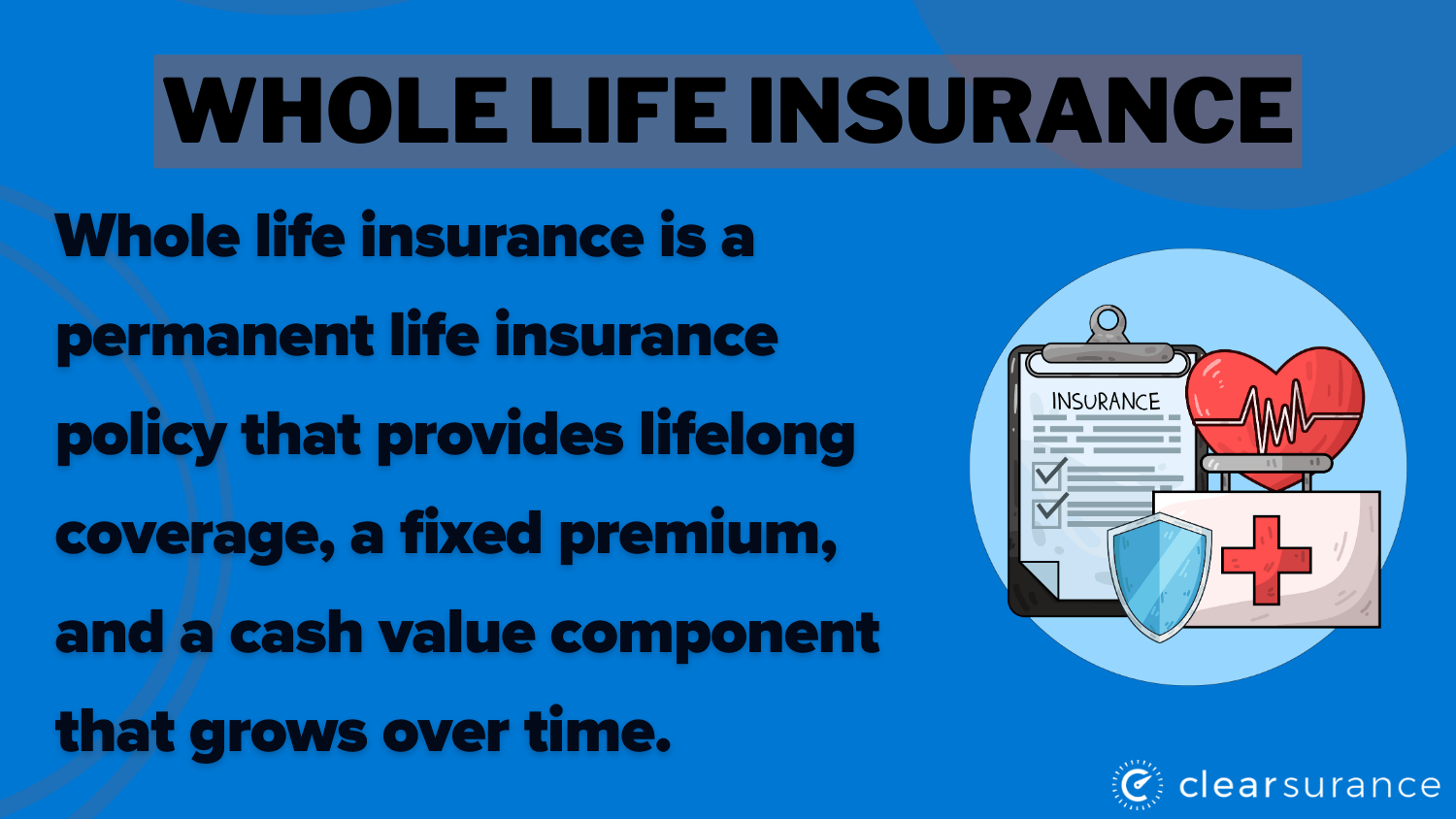

Policies for life insurance provide varying degrees of security, flexibility, and investment opportunity. Universal life insurance is a long-term choice for anyone seeking flexibility because it enables policyholders to modify coverage and premiums while accruing cash value. Indexed universal life insurance (IUL) links cash value growth to a stock market index, offering higher returns with some risk protection, while variable life insurance provides more investment options but with greater financial exposure.

| Insurance Company | Universal | Indexed Universal | Guaranteed Issue | Variable | AD&D |

|---|---|---|---|---|---|

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ❌ | ✅ | ❌ | ✅ | |

| ✅ | ✅ | ❌ | ✅ | ❌ | |

| ✅ | ✅ | ✅ | ❌ | ✅ | |

| ✅ | ✅ | ❌ | ✅ | ✅ | |

| ✅ | ✅ | ❌ | ✅ | ✅ | |

| ✅ | ✅ | ❌ | ✅ | ❌ | |

| ✅ | ✅ | ❌ | ✅ | ✅ | |

| ✅ | ❌ | ✅ | ❌ | ✅ | |

| ✅ | ❌ | ✅ | ❌ | ✅ |

For individuals who may not qualify for traditional policies, guaranteed issue life insurance offers coverage without a medical exam, though it typically comes with higher premiums and lower payout limits. Accidental death and dismemberment (AD&D) insurance adds another layer of security, paying benefits for accidental deaths or severe injuries like loss of limbs or eyesight. It's important to consider the role of an insurance deductible, especially in AD&D policies, as it determines out-of-pocket costs before benefits are paid.

Choosing the right coverage depends on financial goals, risk tolerance, and future security needs. Whether focusing on investment growth, flexible premiums, or guaranteed acceptance, selecting the right policy ensures long-term financial protection.

Comparing Life Insurance Rates for Different Policy Types

Rates for life insurance can differ significantly based on the provider and the type of policy. Certain plans, such as term life insurance, are inexpensive, but whole and universal life insurance policies are more expensive but provide long-term assurance. Prices can differ even more if you're looking for final expense coverage or guaranteed issue policies, which fall under no medical exam life insurance options.

| Insurance Company | Term Life | Whole Life | Universal Life | Final Expense | Guaranteed Issue |

|---|---|---|---|---|---|

| $27 | $55 | $50 | $35 | $45 | |

| $22 | $40 | $45 | $31 | $42 | |

| $26 | $34 | $55 | $39 | $42 | |

| $20 | $35 | $40 | $30 | $50 | |

| $30 | $45 | $42 | $28 | $48 | |

| $25 | $50 | $48 | $30 | $45 | |

| $28 | $60 | $50 | $44 | $38 | |

| $25 | $28 | $55 | $42 | $44 | |

| $30 | $50 | $45 | $40 | $49 | |

| $28 | $35 | $45 | $41 | $41 |

Picking the right plan means balancing affordability with the protection you need. If you want the cheapest term life insurance, Mutual of Omaha wins with a $20 monthly rate, while State Farm and Nationwide charge $30—50% more. Farmers has the lowest whole life insurance rate at $40, but Northwestern Mutual sits at $60, making it 50% pricier. Universal life plans vary too—Lincoln Financial and Prudential charge $55, while Mutual of Omaha offers a much cheaper $40 option, saving you up to 27%.

Looking at final expense insurance, Nationwide keeps it affordable at $28 per month, while Northwestern Mutual is one of the most expensive at $44. Guaranteed issue policies also see big differences—Mutual of Omaha's $50 plan is one of the highest, while The Hartford keeps it lower at $41. With so many pricing gaps, it's clear that choosing the right insurer isn't just about monthly costs—it's about getting the best value for your money.

Top Life Insurance Providers in Minnesota for Affordable Coverage

State Farm, Prudential, and Mutual of Omaha stand out as having the best life insurance in Minnesota. State Farm offers the lowest term life insurance rate at $22 per month, which is 27% lower than the state average of $30. Prudential provides a 15% healthy lifestyle discount for policyholders who meet BMI, cholesterol, and blood pressure targets.

To find the best life insurance near you, comparing multiple quotes online can help identify the most affordable rates, top discounts, and fastest approval options. Reviewing an essential insurance checklist for millennials can help young adults understand coverage needs and secure the right policy early.

Enter your ZIP code to compare instant life insurance quotes from highly-rated insurers and begin investing in your family’s future.

Frequently Asked Questions

Which company is the best for life insurance in Minnesota?

State Farm, Prudential, and Mutual of Omaha offer the best life insurance in Minnesota. State Farm provides term policies as low as $22 per month, Prudential offers a 15% healthy lifestyle discount, and Mutual of Omaha approves policies in as little as 24 hours.

How good is Minnesota life insurance?

Minnesota life insurance is affordable and reliable. Term policies average $25–$30 per month and offer strong financial protections for policyholders.

What is the downside of life insurance?

Whole-life policies cost significantly more than term life, often 5-10 times higher, and early withdrawals can reduce the death benefit for those considered the next of kin.

Do you have to pay taxes on life insurance in Minnesota?

Life insurance death benefits are tax-free, but cash value withdrawals above the premium paid may be taxed as income.

Who has the best whole life insurance in Minnesota?

Northwestern Mutual and New York Life provide dividend-paying whole-life policies. Northwestern Mutual offers A++ financial stability and flexible premium options.

Can you cash out a life insurance policy in Minnesota?

Yes, whole and universal life insurance policies build cash value, and Mutual of Omaha offers fast access to funds within 24 hours through a non-forfeiture option.

Can you have more than one life insurance policy in Minnesota?

Yes, you can own multiple policies, as long as the total coverage doesn’t exceed 20-30 times your annual income, which is the industry guideline.

Does State Farm offer cash-value life insurance?

State Farm offers universal and whole life insurance policies that accrue cash value that can be taken out or borrowed against.

Is life insurance a good way to leave an inheritance?

Yes, life insurance provides a tax-free lump sum that avoids probate and ensures financial security for beneficiaries, highlighting the benefits of buying life insurance.

What are the two disadvantages of whole life insurance?

Whole life costs up to 10 times more than term life, and returns on cash value are lower than traditional investments, averaging 2-4% annually.

What is the difference between term and whole life insurance?

Term life covers a set period (10-30 years) and is cheaper, while whole life lasts a lifetime and builds cash value but costs significantly more.

What voids life insurance payout in Minnesota?

Payouts can be voided due to fraud, non-disclosure of medical history, suicide within the first two years, death due to criminal activity, or policy restrictions associated with modified life insurance.

What are the three main types of life insurance?

The three main types are term life (affordable, temporary), whole life (permanent, builds cash value), and universal life (flexible premiums and benefits).

What Minnesota life insurance company pays the most claims?

Companies with high payout rates include State Farm, Prudential, and Mutual of Omaha, which maintain claim approval rates above 95%.

What age is best to buy whole life insurance in Minnesota?

The best time is in your 20s or early 30s when premiums are 40-60% lower than when you purchase in your 40s or later, especially if you plan to buy life insurance for someone else.

Is life insurance tax deductible?

Premiums for life insurance cannot be written off by individuals, however premiums for plans offered to employees can be written off by corporations.

At what point is life insurance not worth it?

Life insurance may not be worth it if you have no dependents, sufficient retirement savings, and no outstanding debts requiring coverage. However, digital life insurance companies that offer online quotes make it easier to explore affordable options if your needs change.

How does life insurance work in Minnesota?

Life insurance provides financial protection, ensuring beneficiaries receive a lump sum payout, with policies averaging $25–$30 monthly for term coverage.