Best and Cheapest Homeowners Insurance in Wisconsin for 2026 (Top 10 Low-Cost Companies)

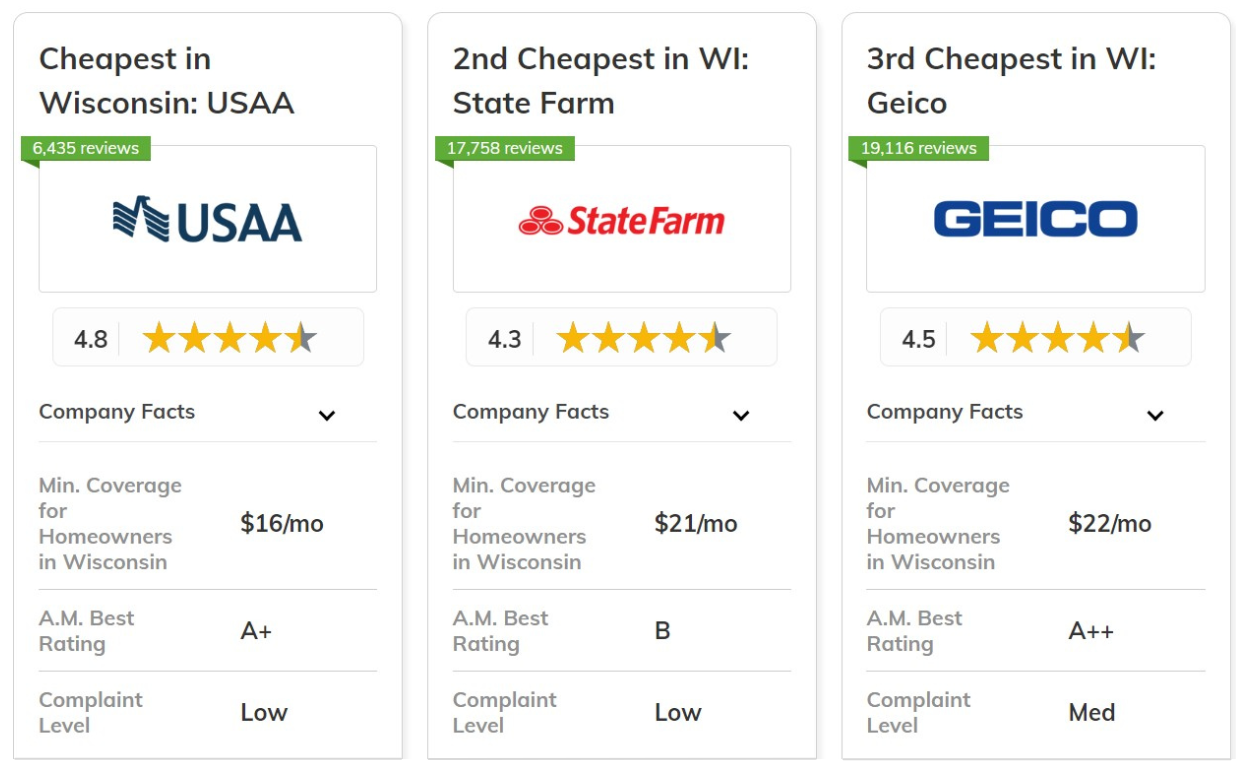

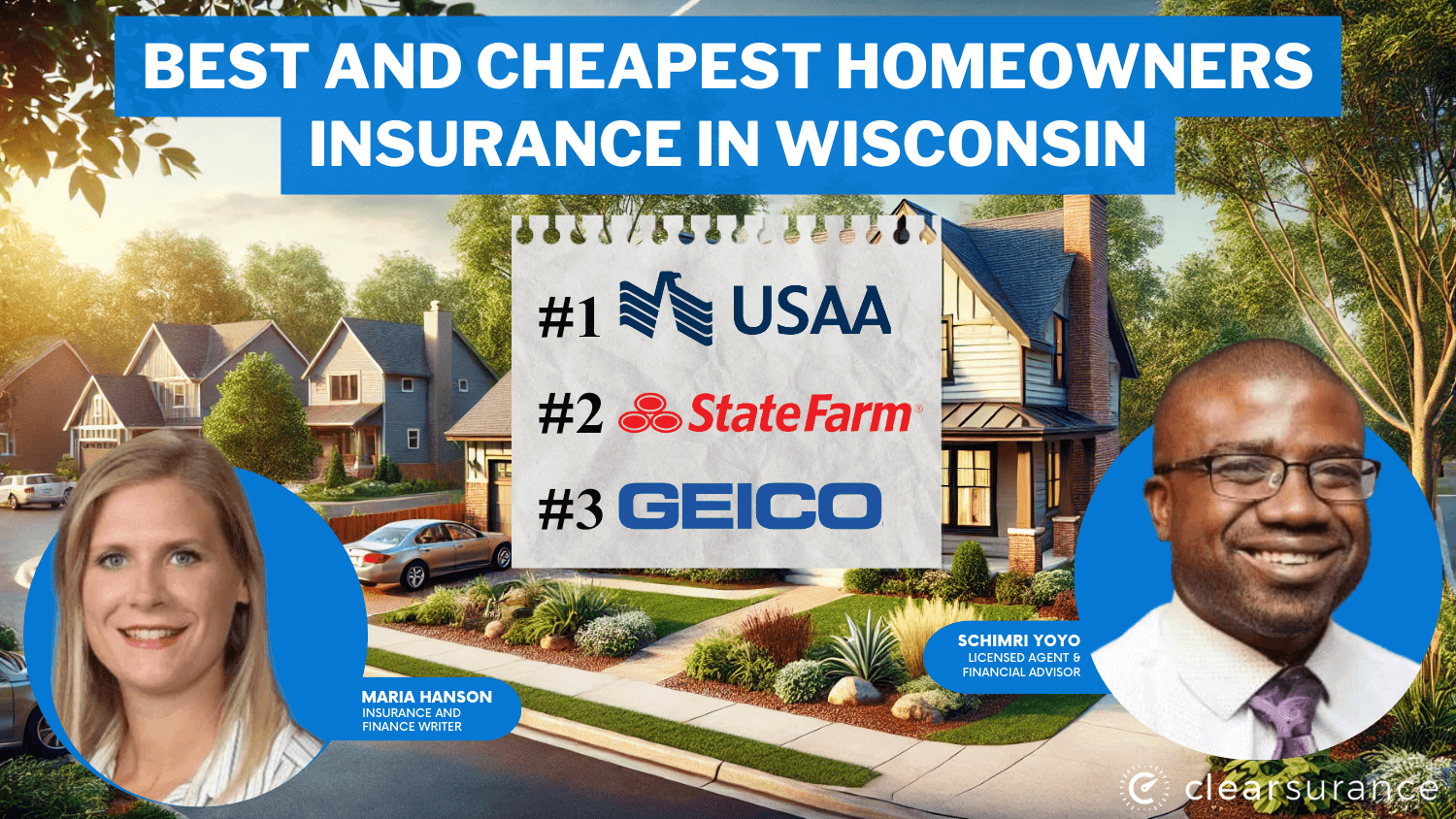

USAA, State Farm, and Geico are top choices for the best and cheapest homeowners insurance in Wisconsin. USAA leads with the lowest monthly rates, starting at $16, and offering the best military car insurance as well.

State Farm boasts Wisconsin's largest network of in-state agents with local property expertise, while Geico stands out with its AI-powered claims system for faster settlements.

| Company | Rank | Monthly Rates | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $16 | A++ | Military Focus | USAA | |

| #2 | $21 | B | Strong Reputation | State Farm | |

| #3 | $22 | A++ | Affordable Coverage | Geico | |

| #4 | $24 | A | Local Expertise | American Family | |

| #5 | $26 | A++ | Comprehensive Policies | Travelers | |

| #6 | $30 | A | Customizable Options | Liberty Mutual | |

| #7 | $33 | A+ | Competitive Rates | Progressive | |

| #8 | $38 | A | Personal Service | Farmers | |

| #9 | $43 | A+ | National Presence | Allstate | |

| #10 | $80 | A+ | Trusted Brand | Nationwide |

Wisconsin homeowners face unique challenges, from ice dams to frozen pipes, with rates varying significantly between urban areas like Milwaukee and Madison versus rural regions.

Explore our guide for detailed insights on protecting your home while saving money. Explore home insurance quotes in Wisconsin by entering your ZIP code into our free comparison tool.

What You Should Know

- USAA offers the lowest rates starting at $16/mo

- State Farm boasts Wisconsin's largest network of in-state agents

- Geico stands out with its AI-powered claims system

#1 – USAA: Top Overall Pick

Pros

- Military Member Savings: Offering unmatched value for service members and their families, consistently ranked the cheapest homeowners insurance in Wisconsin with $16 monthly rates.

- Emergency Deployment Coverage: Wisconsin's only homeowners insurance with active deployment protection, ensuring your home stays protected while serving your country overseas.

- Military Property Protection: Special coverage for uniforms and service equipment with homeowners insurance in Wisconsin, including full replacement cost for damaged military gear. Learn more about their service quality in this USAA insurance review.

Cons

- Military Membership Requirement: The best Wisconsin homeowners insurance rates are reserved for military families and not available to civilian households.

- Limited Branch Locations: Only virtual support is available for Wisconsin homeowners insurance claims, which may challenge those preferring face-to-face service.

#2 – State Farm: Best for Strong Reputation

Pros

- Wisconsin-Based Agents: Largest local network offering best homeowners insurance guidance in all 72 counties in Wisconsin, ensuring personalized service wherever you live.

- Premier Service Program: Only Wisconsin homeowners insurance with guaranteed contractor workmanship, protecting you from subpar repairs after claims.

- Education Discount Program: Special rates for Wisconsin educators and education staff, with additional savings for long-term policyholders. For detailed information, view this State Farm insurance review.

Cons

- Premium Rate Structure: Higher baseline rates than the cheapest Wisconsin homeowners insurance providers, particularly for homes with older roofs or systems.

- Limited Online Tools: Most Wisconsin policy changes require agent involvement, making quick policy adjustments more time-consuming than with digital-first providers.

#3 – Geico: Best for Affordable Coverage

Pros

- First-Time Buyer Program: Best new homeowner insurance rates in Wisconsin with specialized guidance and dedicated support teams to help you through the entire purchasing process.

- Automated Claims Process: Fastest digital claims among Wisconsin homeowners insurance providers, with most claims resolved within 48 hours through their advanced online platform.

- Federal Employee Benefits: Enhanced coverage options for Wisconsin federal workers with exclusive discounts and specialized protection plans. (Read more: Best Car Insurance Companies for Federal Employees)

Cons

- Limited Personal Service: No dedicated Wisconsin homeowners insurance agents available for face-to-face consultations or personalized claim handling processes.

- Basic Coverage Focus: Limited luxury home coverage in Wisconsin's high-value markets, with restrictions on premium property features and high-end renovations.

#4 – American Family: Best for Local Expertise

Pros

- Midwest Weather Protection: Only Wisconsin homeowners insurance with specific ice dam coverage and comprehensive winter damage protection for your entire property.

- Diminishing Deductible: Unique rewards for claim-free Wisconsin homeowners that gradually reduces your out-of-pocket expenses over time with maintained coverage.

- Farm Property Expertise: Best agricultural property insurance in Wisconsin with specialized coverage for barns, equipment, and livestock. Learn more in this review of American Family insurance.

Cons

- Urban Rate Variation: Highest Wisconsin homeowners insurance rates in Milwaukee/Madison areas due to increased property values and higher claim frequencies.

- Strict Claim Requirements: Approval of Wisconsin winter damage claims requires detailed evidence and professional assessments for the most demanding documentation.

#5 – Travelers: Best for Comprehensive Policies

Pros

- Green Home Coverage: Only Wisconsin homeowners insurance offering eco-renovation reimbursement and additional protection for sustainable home improvements and energy-efficient upgrades.

- Heritage Home Specialists: Exclusive coverage for pre-1940 Wisconsin properties with dedicated experts who understand historical building materials and preservation requirements.

- Home Business Protection: Best home-office coverage in Wisconsin with enhanced protection for business equipment and liability coverage for client visits. See details in this Travelers car insurance review.

Cons

- Complex Policy Structure: Most detailed Wisconsin homeowners insurance terms with numerous clauses and conditions that can be challenging to navigate without expert assistance.

- Higher Coverage Minimums: More coverage is needed than Wisconsin state minimums, and basic property protection needs may be more expensive.

#6 – Liberty Mutual: Best for Customizable Options

Pros

- Inflation Protection: Coverage that automatically adjusts for Wisconsin’s changing property values to keep your home properly covered throughout the year.

- Water Backup Coverage: Specialized protection against Wisconsin's basement flooding issues, including comprehensive coverage for sump pump failures and sewage system backups.

- New Purchase Benefits: Extra coverage options for newly bought Wisconsin homes with flexible payment plans and first-time buyer discounts. Explore options in this Liberty Mutual insurance review.

Cons

- Coverage Gaps: Additional riders are necessary for some common Wisconsin perils, which raise overall costs for homeowners insurance against regional weather perils.

- Quote Consistency: Detailed home inspection in Wisconsin often results in substantial change of initial quotes and unexpected increase of premium for many Wisconsin homeowners.

#7 – Progressive: Best for Competitive Rates

Pros

- Snapshot Home Program: In Wisconsin, discounts based on smart home technology include significant savings for homes equipped with modern security and monitoring systems.

- Multi-Quote Comparison: Unique platform showing competitor rates for Wisconsin properties, helping homeowners find the most affordable coverage options in their area.

- Seasonal Home Coverage: Special protection for Wisconsin vacation and seasonal properties with flexible coverage periods and customized security requirements. Read more in this Progressive car insurance review.

Cons

- Partner Underwriting: Policies are often underwritten by third-party Wisconsin insurers, which can lead to inconsistent service experiences and claim processing times.

- Limited Legacy Support: Less established history in the Wisconsin market may lead to less stable long-term policy and customer service capabilities.

#8 – Farmers: Best for Personal Service

Pros

- Claim Forgiveness: No rate increase for first claim by long-term Wisconsin customers, protecting loyal policyholders from premium hikes after isolated incidents.

- Renovation Coverage: Specialized protection during home improvements and remodels in Wisconsin, including coverage for construction materials and temporary storage.

- Identity Shield: Enhanced identity theft protection for Wisconsin residents with comprehensive monitoring and recovery services. View details in this Farmers insurance review.

Cons

- Traditional Focus: Fewest digital tools for Wisconsin policy management, requiring more phone calls and in-person visits for routine policy adjustments.

- Standard Policy Limits: Most add-ons required for full Wisconsin coverage, making it difficult to obtain comprehensive protection without multiple policy endorsements.

#9 – Allstate: Best for National Presence

Pros

- Claim RateGuard: Only multi-year rate lock after Wisconsin claims, protecting you from premium increases for up to three years following a covered loss.

- Welcome Discount: Largest new customer discount for Wisconsin transfers, offering significant savings when switching from another insurance provider.

- Retirement Benefits: Specialized coverage options for Wisconsin's senior residents with additional protection for valuable collections and antiques. Learn more in our Allstate insurance review.

Cons

- Age-Based Pricing: Highest rates of homes 50 years old or more in Wisconsin, with strict requirements for new systems and maintenance.

- Bundle Requirements: Most discounts require multiple policies, making it expensive to maintain standalone Wisconsin homeowners insurance coverage.

#10 – Nationwide: Best for Trusted Brand

Pros

- Better Roof Replacement: Only Wisconsin coverage upgrading to impact-resistant materials after storm damage, improving long-term home protection.

- Extended Replacement Cost: Highest rebuilding coverage in the Wisconsin market, offering up to 200% of your policy limit for reconstruction.

- Ordinance Coverage: Comprehensive protection for Wisconsin building code updates during repairs, preventing unexpected out-of-pocket expenses. Explore our Nationwide insurance review.

Cons

- Coverage Eligibility: Strictest Wisconsin property condition standards, requiring recent updates to major home systems for coverage approval.

- Regional Availability: Due to the limits in most rural Wisconsin service areas, coverage outside of major metropolitan regions is challenging to come by.

Wisconsin Homeowners Insurance Rates

To find quality homeowners insurance in Wisconsin, understanding market options is essential. The best homeowners insurance in Wisconsin protects against usual threats like winter storms, water damage, and structural problems.

When seeking cheap homeowners insurance in Wisconsin, comparing minimum and full coverage monthly rates reveals significant savings opportunities.

| Insurance Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $43 | $123 | |

| $24 | $63 | |

| $38 | $109 | |

| $22 | $62 | |

| $30 | $84 | |

| $80 | $226 | |

| $33 | $94 | |

| $21 | $58 | |

| $26 | $72 | |

| $16 | $47 |

Home insurance in Wisconsin varies by location, with urban areas typically commanding higher rates. Factors affecting rates include property value increase, location, and construction type, while additional coverage options like water backup protection cater to Wisconsin's specific climate needs.

Save on Homeowners Insurance in Wisconsin

Providers' wide range of discount programs helps secure affordable home insurance in Wisconsin. The best home insurance companies in Wisconsin can provide you with great savings opportunities that are unique to each insurance company.

| Insurance Company | Available Discount |

|---|---|

| Multi-Policy, Claims-Free, Home Safety, Early Signing, New Homebuyer | |

| Multi-Policy, Generational Discount, Loyalty, Smart Home, Renovation Discount | |

| Multi-Policy, Home Safety, Claims-Free, New Home, Renovation Discount | |

| Bundling, Smoke Detectors, Home Security Systems, Fire Extinguishers, Claims-Free | |

| Bundling, Claims-Free, Early Shopper, New Homebuyer, Protective Devices | |

| Multi-Policy, Protective Devices, Claims-Free, New Homebuyer, Renovations | |

| Multi-Policy, Protective Devices, Home Renovations, Claims-Free, Quote in Advance | |

| Multi-Policy, Home Security Systems, Claims-Free, Roofing Materials, Loyalty | |

| Multi-Policy, Protective Devices, Claims-Free, Green Home, Early Quote | |

| Bundling (auto + Home), Claims-Free, Home Security Systems, Loyalty, Military Service |

American Family has a generational discount program for long time customer families, and USAA has special military service discounts. State Farm’s roofing materials discount and multi policy savings are combined, for up to 25% off premiums, for those looking for the cheapest home insurance.

Native Americans serve in our armed forces at 5 times the national average. Their legacy of service, made unforgettable by the Code Talkers, continues today. #NativeAmericanHeritageMonth pic.twitter.com/7aI2Qqr0q0

— USAA (@USAA) November 13, 2024

Liberty Mutual is one that stands out as it rewards early shoppers with additional savings and Geico offers specific discounts to fire extinguishers and smoke detectors. Unique to Travelers, green home discounts reward ecofriendly property upgrades.

| Discount Name | Grade | Savings | Participating Providers |

|---|---|---|---|

| Multi-Policy | A+ | 20% | State Farm, Allstate, Liberty Mutual |

| Security System Installation | A | 15% | Progressive, American Family, Travelers |

| Claims-Free | A | 10% | Farmers, Nationwide, Geico |

| New Home Discount | B+ | 8% | USAA, Amica, State Farm |

| Loyalty | B | 5% | Liberty Mutual, Allstate, American Family |

For Wisconsin homeowners, the savings go beyond standard discounts because American Family will incentivize homeowners to perform home renovations with the company or install smart home devices through Progressive’s protective device program, and homeowners will reap savings on the premium for years to come while also increasing protection for the property.

Wisconsin Homeowners Insurance Reports

Knowing the most usual forms of insurance claims in Wisconsin allows homeowners to be prepared for threats that could be encountered and to select the correct amount of coverage. The following data displays the frequency and average cost of different claim types.

| Claim Type | Portion of Claims | Cost per Claim |

|---|---|---|

| Wind and Hail Damage | 30% | $10000 |

| Liability Claims | 25% | $20000 |

| Water Damage and Freezing | 20% | $7500 |

| Fire and Lightning Damage | 15% | $50000 |

| Theft and Burglary | 10% | $3500 |

Wisconsin's claim types are wind and hail damage, with fire claims having the highest costs. In regional differences, Wisconsin’s urban areas have different insurance incidents rates that affect local premium costs.

| City | Accidents per Year | Claims per Year |

|---|---|---|

| Green Bay | 800 | 300 |

| Kenosha | 600 | 250 |

| Madison | 1,500 | 700 |

| Milwaukee | 3,000 | 1,200 |

| Racine | 500 | 200 |

Urban residents, for example, can expect higher rates because Milwaukee, for instance, shows four times as many claims as smaller cities. Yet, Wisconsin's insurance market ranks strong across many performance measures, as shown in the report below.

| Category | Grade | Explanation | |

|---|---|---|---|

| Affordability | A+ | Wisconsin’s average premiums are below national average | |

| Customer Satisfaction | A | High satisfaction ratings from policyholders | |

| Claims Handling Efficiency | A | Timely and efficient claims handling processes | |

| Availability of Discounts | B+ | Variety of discounts available for policyholders | |

| Coverage Options | B | Standard coverage options with some customizability |

These combined statistics explain why Wisconsin maintains competitive insurance rates despite varying claim rates between urban and suburban areas, with particularly strong performance in affordability and customer satisfaction.

Read More: 5 Things to Know About Home Insurance

Wisconsin's Best Homeowners Insurance Companies

Wisconsin's homeowners insurance market is led by USAA, which offers exclusive military rates starting at just $16 monthly, followed by State Farm with the state's biggest local agent network coming in at $21 monthly, and Geico with AI powered claims processing starting at $22 monthly.

A solid home insurance in Wisconsin will also have good financial ratings and particular coverage options for the weather issues Wisconsin faces, including ice dam, winter storm protection and hail damage.

Protecting your home doesn’t have to be expensive. Enter your ZIP code into our free tool to find affordable homeowners insurance today.

Frequently Asked Questions

What is the average cost of homeowners insurance in Wisconsin?

The average cost of homeowners insurance in Wisconsin varies, with minimum coverage starting at $16 monthly through USAA and full coverage ranging from $47 to $226 monthly, depending on the provider and coverage level.

Who has the cheapest home insurance in Wisconsin?

USAA offers the cheapest rates starting at $16 monthly, followed by State Farm at $21 and Geico at $22 for minimum coverage. However, USAA is only available to military members and their families.

Compare quotes from the cheapest home insurance companies by entering your ZIP code into our free tool.

What is the best homeowners insurance company in Wisconsin?

USAA ranks #1 as the best homeowners insurance provider, while State Farm ranks #2 with the largest network of local agents, and Geico ranks #3 with fast AI-powered claims processing.

Is homeowners insurance required in Wisconsin?

While Wisconsin law doesn't require homeowners insurance, mortgage lenders typically require it as a condition of the loan to protect their investment in the property.

What type of insurance coverage is needed in Wisconsin?

Basic coverage should protect against Wisconsin's common risks, which include winter storms, ice dams, frozen pipes, and water damage. Coverage needs vary based on location, with urban areas like Milwaukee requiring protection different from that of rural properties.

Do you need proof of insurance in Wisconsin?

While proof of homeowners insurance isn't required by state law, mortgage lenders typically require proof of coverage, and insurance documentation is often needed when filing claims or applying for policy discounts.

Read More: 3 Ways to Obtain Proof of Insurance

Has homeowners insurance increased in Wisconsin?

Yes, homeowners insurance rates in Wisconsin have increased. Wisconsin homeowners saw an average increase of 8-12% in their premiums due to rising construction costs, severe weather events, and inflation.

Which homeowners insurance is the cheapest for full coverage?

For full coverage, USAA offers the lowest rates at $47 monthly, followed by State Farm at $58 and Geico at $62 monthly.

What is the most common home insurance coverage?

The most common type is HO-3 coverage, which protects against winter storms, water damage, and structural issues. This policy typically includes dwelling coverage, personal property protection, liability coverage, and additional living expenses if your home becomes uninhabitable.

Read More: What is an HO-3 Insurance Policy?

Is it illegal to not have insurance in Wisconsin?

No, it's not illegal to not have homeowners insurance in Wisconsin. However, if you have a mortgage, your lender will require you to maintain coverage.

Don’t settle for expensive home insurance premiums. Enter your ZIP code to find robust coverage for your dwelling at an affordable price.