Best and Cheapest Homeowners Insurance in Georgia for 2026 (10 Most Affordable Companies)

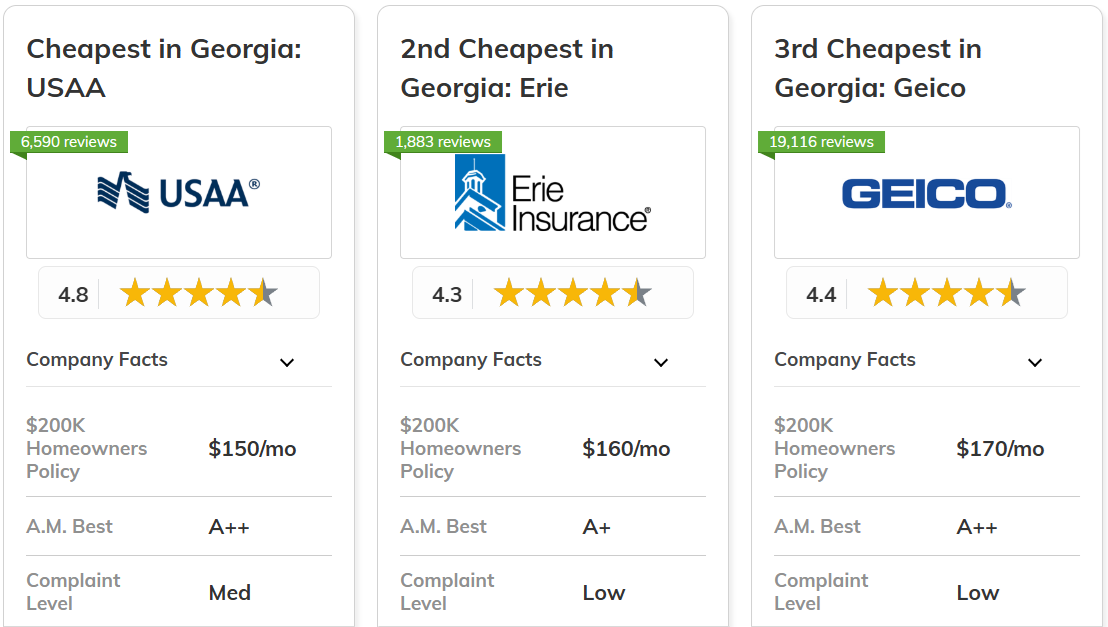

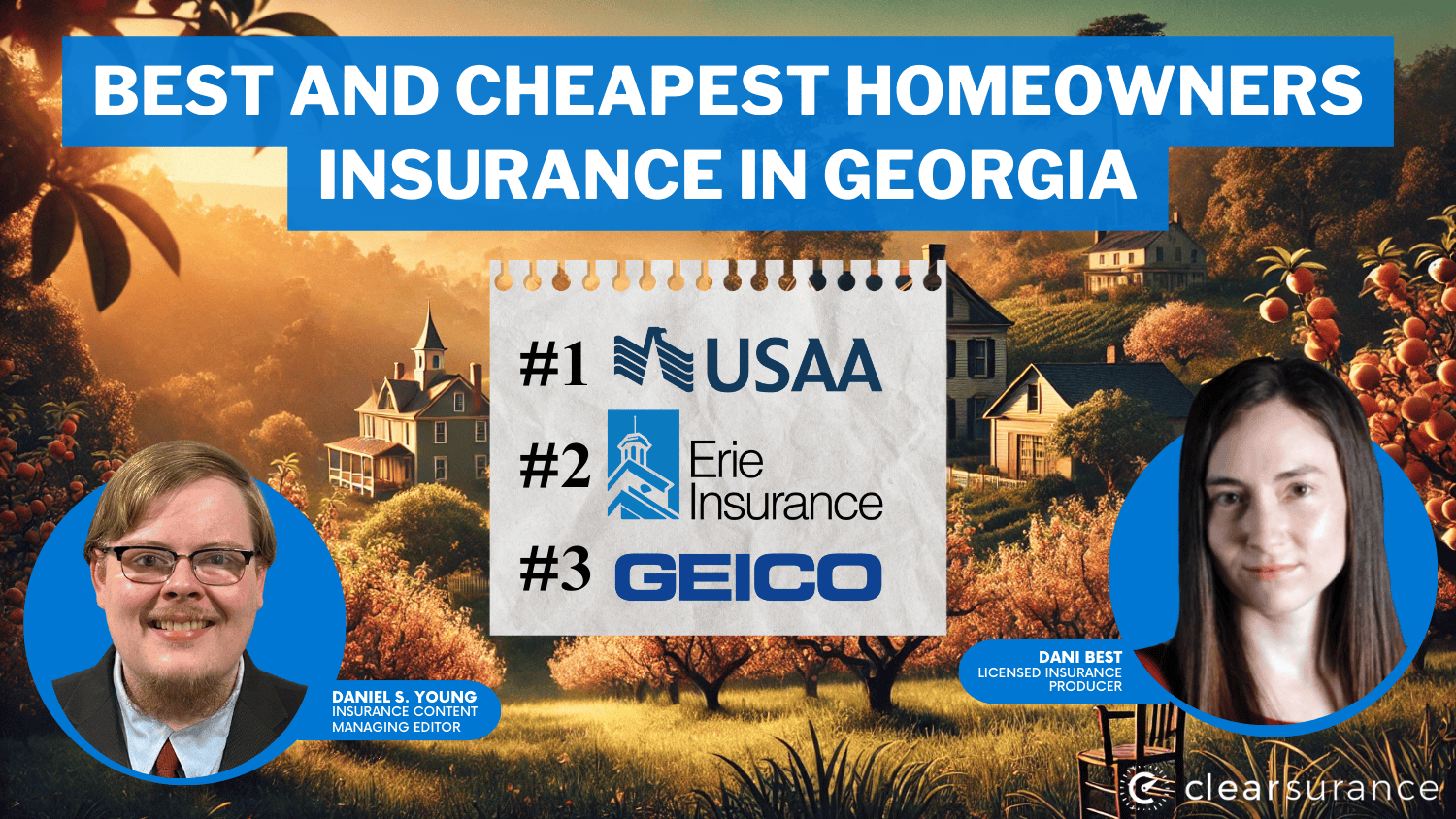

The best and cheapest homeowners insurance in Georgia includes USAA, Erie, and Geico, with Geico offering the lowest rates starting at $90/month.

USAA is the best choice for military families, while Erie excels for its comprehensive coverage, and Geico stands out for its affordability. This article compares rates and coverage options from Georgia's top providers, ensuring you find the right policy for your home.

| Company | Rank | Monthly Rates | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | 165 | A++ | Military Members | USAA | |

| #2 | 175 | A++ | Comprehensive Coverage | Erie | |

| #3 | 185 | A++ | Affordable Rates | Geico | |

| #4 | 190 | A++ | Snapshot Savings | Progressive | |

| #5 | 195 | A+ | Snapshot Savings | Travelers | |

| #6 | 200 | A++ | Hybrid Discounts | State Farm | |

| #7 | 205 | A+ | Customer Satisfaction | Nationwide | |

| #8 | 210 | A | Comprehensive Discounts | Farmers | |

| #9 | 205 | A+ | Coverage Flexibility | American Family | |

| #10 | 220 | A+ | Customer Loyalty | Allstate |

From affordable premiums to comprehensive coverage, discover the best options tailored to your needs. Looking for affordable home insurance tailored to your needs? Enter your ZIP code into our free comparison tool to get instant quotes from the top insurance providers.

What You Should Know

- Find the best and cheapest homeowners insurance in Georgia with rates starting at $90/month

- Compare top providers offering tailored coverage for Georgia’s unique weather risks

- USAA is the top pick for affordable rates and reliable military coverage

#1 – USAA: Top Overall Pick

Pros

- Military Discounts in GA: Rates for Georgia-based military families start at $90/month.

- Claims Efficiency in Georgia: Fast and reliable service tailored for military homeowners in GA.

- Exclusive Perks: Special benefits for military families stationed in or from Georgia. Delve into our USAA review.

Cons

- Membership Limits in GA Only available to Georgia military personnel and their families.

- Non-Military Costs: Georgia homeowners without military ties may face higher rates.

#2 – Erie: Best for Comprehensive Coverage

Pros

- Affordable Plans in GA: Policies start at $92/month, offering robust coverage for Georgia homeowners.

- Efficient Claims in GA: As per our Erie review, it provides high satisfaction for claims services in Georgia.

- Add-Ons for GA Risks: Flexible endorsements address unique challenges for homes in Georgia.

Cons

- Limited Discounts in GA: Georgia homeowners may find fewer opportunities for savings through bundling.

- Restricted Availability: Erie policies may not be available in all Georgia regions.

#3 – Geico: Best for Affordable Rates

Pros

- Lowest Rates in GA: Policies start at $95/month, the cheapest homeowners insurance option in Georgia.

- Georgia Discounts: Multi-policy savings are ideal for homeowners bundling coverage in GA (Learn more: 32 Genius Ways to Save Money).

- Online Ease: Georgia residents can manage policies effortlessly with Geico’s user-friendly platform.

Cons

- Limited Flexibility for GA Homes: Customization options may not meet all specific Georgia needs.

- Add-On Costs: Some coverage options for Georgia properties might raise premiums.

#4 – Progressive: Best for Snapshot Savings

Pros

- Snapshot Savings for GA: Minimum coverage starts at $97/month, with extra discounts for Snapshot users in Georgia.

- Personalized Coverage in GA: Georgia homeowners can adjust policies to meet unique local needs.

- Bundling in GA: Combining home and auto policies offers significant savings for Georgia residents which covered in our Progressive review.

Cons

- Snapshot Participation in GA: Discounts require enrolling in a telematics program, which may not appeal to all Georgia homeowners.

- Risk Add-Ons for GA: Additional endorsements for common Georgia risks can increase costs.

#5 – Travelers: Best for Hybrid Discounts

Pros

- Budget-Friendly for GA Homes: Home insurance rates start at $98/month with bundled savings in Georgia.

- Eco-Friendly Options for GA: Discounts for sustainable upgrades appeal to Georgia homeowners.

- Reliable Disaster Coverage: Comprehensive plans cover Georgia's natural disaster risks, including floods and tornadoes. Check out our Travelers review.

Cons

- Confusing Discounts in GA: Some Georgia homeowners may struggle to understand qualification requirements.

- Limited Coverage Areas: Certain rural parts of Georgia may lack access to all policies.

#6 – State Farm: Best for Customer Satisfaction

Pros

- High Satisfaction in GA: Georgia homeowners report excellent service, with rates starting at $100/month.

- Custom Policies for GA Risks: Coverage options address Georgia-specific weather challenges, like hurricanes or tornadoes.

- Local Agents in Georgia: Strong network of agents across the state for easy in-person support. Discover our State Farm review for a full list.

Cons

- Premium Costs in GA: Comprehensive coverage for Georgia homes may come at a higher price.

- Bundling Discounts in GA: Savings for combining policies may be less competitive in Georgia.

#7 – Nationwide: Best for Comprehensive Discounts

Pros

- GA-Specific Discounts: Home insurance starts at $101/month with multi-policy savings for Georgia residents.

- Risk Coverage for GA Homes: Comprehensive plans include protection for hurricanes and flooding common in Georgia.

- Convenient App for GA Users: Georgia homeowners can manage policies and file claims with ease. For a comprehensive list, refer our Nationwide review.

Cons

- Higher Add-On Costs in GA: Endorsements for enhanced coverage can increase premiums for Georgia homeowners.

- Local Agent Gaps in GA: Nationwide has limited agent presence in some parts of Georgia.

#8 – Farmers: Best for Cheap Rates & Discounts

Pros

- Affordable Rates for GA Homes: Minimum coverage starts at $102/month with discounts tailored for Georgia.

- Telematics Savings in GA: The Signal program rewards Georgia homeowners for safe behaviors.

- Endorsements for GA Risks: Farmers offers add-ons for risks like windstorms common in Georgia, see our Farmers review for detailed insight.

Cons

- Higher Initial Costs in GA: Base rates are above the average for Georgia.

- Slower Claims Service in GA: Some Georgia homeowners report delays in resolving claims.

#9 – American Family: Best for Coverage Flexibility

Pros

- Customizable Policies for GA: Coverage tailored to Georgia-specific needs starts at $105/month.

- Bundling Discounts in GA: Georgia residents can save by combining home insurance with other policies. Browse our full details about American Family insurance company review.

- Financial Strength for GA Claims: Reliable support ensures peace of mind for Georgia homeowners.

Cons

- Higher Starting Rates in GA: Base rates are higher than some competitors in Georgia.

- Statewide Availability: Certain features may not be accessible throughout Georgia.

#10 – Allstate: Best for Customer Loyalty

Pros

- Loyalty Perks for GA Customers: Rates start at $110/month with rewards for long-term Georgia homeowners.

- Tailored Protection in GA: Custom policies address risks like theft and severe storms in Georgia.

- Financial Strength for GA Claims: An A+ rating ensures reliability for claims support in Georgia. Explore more in our Allstate review.

Cons

- Higher Starting Rates in GA: Minimum coverage costs are above average in Georgia.

- Limited Discount Options for GA: Bundling and loyalty perks could offer more savings for Georgia residents.

Top Home Insurance Rates and Coverage Options for Homes in Georgia

If you own a home in Georgia, it's important to have a homeowners insurance policy to protect your assets. But if you want to find the right insurer, you need to understand who offers the best coverage. There are several factors, including the insurance costs you need to consider to find the right policy and coverage options for your needs.

Geico offers the cheapest homeowners insurance rates in Georgia for a $200K home, on average, out of the five most popular homeowners insurance companies in Georgia. The cost of homeowners insurance for a $200k properly is often the lowest due to a low replacement cost. Keep in mind, other things such as your ZIP code and natural hazards you face can change your numbers.

If you're looking for cheap homeowners insurance in GA, providers like Geico and USAA are known for offering the cheapest homeowner insurance without compromising essential coverage. Comparing rates and policies from the top homeowners insurance in GA providers ensures you get the best value for your money while securing peace of mind.

| Insurance Company | $200K | $300K | $500K |

|---|---|---|---|

| $195 | $220 | $330 | |

| $185 | $205 | $310 | |

| $160 | $175 | $275 | |

| $190 | $210 | $320 | |

| $170 | $185 | $290 | |

| $185 | $205 | $310 | |

| $175 | $190 | $295 | |

| $180 | $200 | $305 | |

| $180 | $195 | $300 | |

| $150 | $165 | $265 |

Table above is a comparison of monthly homeowners insurance rates for minimum coverage and full coverage from the largest companies in Georgia. It shows that rates increase significantly when opting for full coverage, with most providers doubling their premiums to offer more comprehensive protection. Comparing these rates can help homeowners identify the best balance of affordability and coverage for their needs.

Browse for full details in our guide "How Home Improvement Projects Affects Your Insurance."

Additionally, homeowners insurance for a $400K home in Georgia requires comparing rates and understanding available discounts. On average, Georgia Farm Bureau offers the most affordable premiums among the state’s top insurance providers for $400K homes. While rates vary by company, it’s essential to look beyond the monthly cost and consider available discounts that can further reduce premiums.

The following table highlights key discounts offered by Georgia’s top homeowners insurance providers, making it easier to identify potential savings:

| Insurance Company | Available Discounts |

|---|---|

| Multi-Policy, Safe Driver, Good Student, Accident Forgiveness, New Car, Anti-Theft, Auto-Pay | |

| Multi-Policy, Loyalty, Good Student, Early Signing, Auto-Pay, Accident-Free, Generational | |

| Multi-Policy, Safe Driver, Good Student, Anti-Theft, Vehicle Safety, Accident-Free, Paperless | |

| Multi-Policy, Good Student, Safe Driver, E-Policy Enrollment, Signal (Telematics), Affinity Discounts | |

| Multi-Policy, Military, Defensive Driving, New Vehicle, Good Student, Accident-Free, Emergency Deployment | |

| Multi-Policy, SmartRide (Telematics), Accident-Free, Defensive Driving, Good Student, Paperless | |

| Multi-Policy, Bundling, Continuous Insurance, Paperless, Snapshot (Telematics), Good Driver | |

| Multi-Policy, Good Student, Accident-Free, Safe Driver, Drive Safe & Save, Passive Restraint | |

| Multi-Policy, Hybrid/Electric Vehicle, Safe Driver, Early Quote, New Vehicle, Good Payer | |

| Military, Multi-Policy, Good Driver, Defensive Driving, Loyalty, Accident Forgiveness, New Vehicle |

For a $400,000 dwelling, typical coverage includes $200,000 for personal property, $40,000 for loss of use, $40,000 for other structures, $300,000 for liability, and $5,000 for medical payments, with a $1,000 deductible. The sample profile assumes a house built in 2004 and an individual with a good insurance score. These rates serve as general comparisons, as individual premiums in Georgia will vary based on location, claims history, and other factors. Rate data is sourced from Quadrant Information Services.

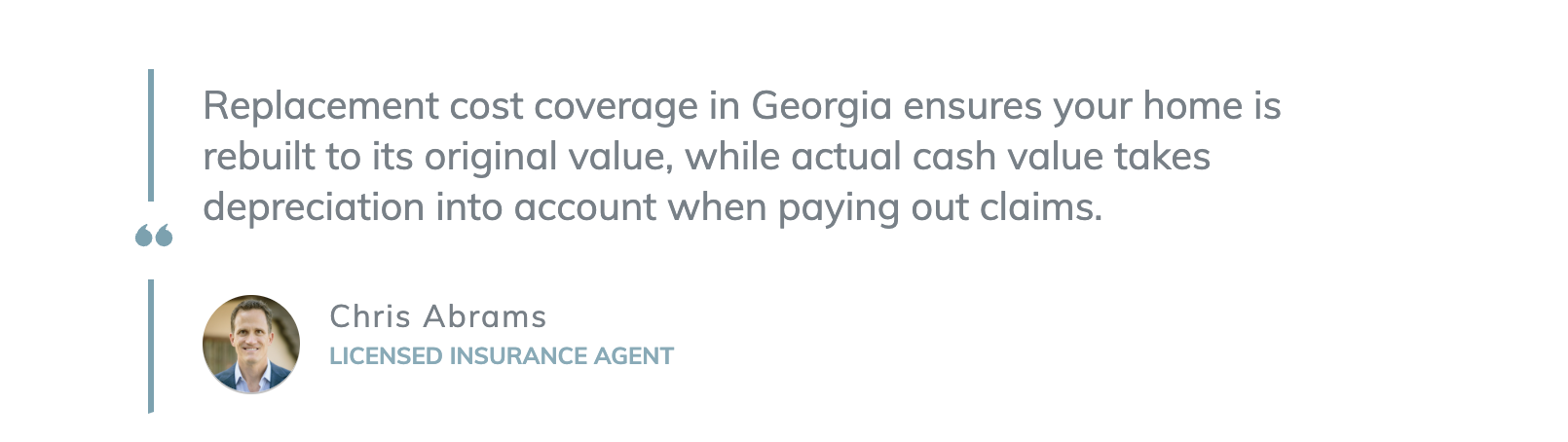

It’s crucial to note that the replacement cost of a home is often lower than its appraisal or market value. Homeowners insurance focuses on the cost to rebuild your house, not its sales price. Refer to our guide about the top 3 ways customers say they’ve saved on homeowners insurance, to learn more.

This ensures accurate coverage without overpaying. Replacement cost estimators help insurance companies calculate appropriate premiums tailored to your home’s rebuilding needs.

How Theft and Vandalism Influence Georgia Home Insurance Costs

Theft and vandalism, classified as malicious mischief, are among the 16 perils typically covered by a standard homeowners insurance policy. Gain more information through our guide about home improvement, contractor theft & homeowners insurance coverage.

These crimes can significantly influence homeowners insurance costs, especially in areas with higher crime rates. In Georgia, property crime statistics reveal a notable impact on insurance rates.

According to FBI data from 2016, Georgia reported 309,770 property crimes, including 63,344 burglaries and 219,625 larceny thefts. When compared to the national average rate per 100,000 inhabitants, all three categories rank above the national average. These elevated crime rates make it essential for Georgia homeowners to have comprehensive coverage and may lead to higher premiums in regions with increased risk of theft or vandalism.

Weather-Related Risks and Their Impact on Georgia Home Insurance Premiums

Weather-related risks play a significant role in determining homeowners insurance premiums in Georgia. The state has experienced numerous hurricanes and other natural disasters, making it prone to costly claims for property damage and physical injuries. Incidents like severe storms, tornadoes, floods, and hurricanes can destroy roofs, demolish homes, and lead to extensive rebuilding costs.

According to FEMA data, Georgia has faced 15 severe storms, 13 tornadoes, 12 fires, 10 hurricanes, 9 floods, 3 severe ice storms, and even rare incidents of freezing and snow since 1953. While basic homeowners insurance covers many perils, cheap policies often exclude coverage for hurricanes or windstorms.

Homeowners in Georgia and other storm-prone states like Florida or Hawaii may need a separate hurricane insurance policy to ensure adequate protection. Given the frequency and severity of weather-related risks, understanding these additional coverage needs is crucial for Georgia homeowners to avoid financial burdens during disaster recovery.

Key Factors That Determine Home Insurance Rates in Georgia

Several factors influence the cost of homeowners insurance in Georgia, some of which may be more apparent than others. The age, condition, and square footage of your home are critical considerations, as are your geographic location and proximity to essential services like fire stations. Insurance companies also take into account your level of coverage, the size of your mortgage, and your deductible.

Personal factors, such as your claims history and credit score can further affect your premiums. Additionally, optional add-ons like umbrella insurance or additional living expense coverage can raise costs but provide extra protection.

In Georgia, natural disasters significantly impact insurance rates. Hurricanes are a major risk, along with flooding, which affects many areas of the state. However, flood damage is not included in standard policies, requiring a separate flood insurance policy.

Tornadoes and hailstorms also pose threats, underscoring the need for adequate coverage. On average, homeowners pay about $35 per month for every $100,000 of home value, but adding coverage for natural disasters or high-value items increases annual premiums. Understanding these factors and risks helps homeowners in Georgia choose the right coverage for their needs.

Best Places to Secure Home Insurance Coverage in Georgia

Finding the right home insurance in Georgia is essential to protect your property and belongings, and with so many options, choosing the best policy can feel overwhelming. Several homeowners insurance companies in Georgia offer tailored coverage to meet the unique needs of residents, including protection against common risks like hurricanes and flooding. Learn the 5 things to know about home insurance.

Before you choose any standard or additional coverage, always get a few quotes. Whether you’re a new buyer or looking to switch providers, finding affordable homeowner insurance in GA is achievable with the right research and tools. This way, you can truly compare your insurance coverage options and see what makes sense for you.

So make sure you have a strong understanding of your homeowners insurance coverage and what it all means. Check out our homeowners insurance guide to become a smarter insurance customer. Get started today by entering your ZIP code into our free quote tool.

Frequently Asked Questions

How can I lower my homeowners insurance premiums in Georgia?

To reduce your homeowners insurance premiums in Georgia, consider raising your deductible, installing safety features like security systems or smoke detectors, and bundling home and auto insurance. Additionally, check for available discounts such as multi-policy savings or loyalty rewards. To gather more insight browse our guide that talks about a practical guide for understanding homeowners insurance.

What are the most common coverage gaps in Georgia homeowners insurance?

Many Georgia homeowners overlook the need for flood insurance or hurricane coverage, as standard policies typically do not cover these risks. Depending on where you live, you may need separate policies for flood or windstorm protection. Don’t wait until it’s too late – protect your home by using our free quote comparison tool to find affordable home insurance today.

How does my home’s age impact homeowners insurance rates in Georgia?

Older homes may face higher premiums due to increased risk of damage from wear and tear, outdated systems, or materials that may be harder to repair. Upgrading electrical, plumbing, and roofing systems can help reduce premiums.

What weather-related risks should Georgia homeowners consider when choosing insurance?

Georgia homeowners should focus on coverage for weather-related risks like hurricanes, tornadoes, and flooding. These natural disasters are common in the state and can lead to significant damage if not adequately covered by your policy (Read more: Top 10 homeowners insurance companies with the best buying process, according to customer reviews).

What factors influence home insurance costs in Georgia?

Key factors include the home’s location, age, size, replacement cost, claims history, and risks like hurricanes or flooding. Discounts and deductibles also play a role in determining rates.

Can I get discounts for safety features in my home in Georgia?

Yes, many insurers offer discounts for homes equipped with safety features such as burglar alarms, smoke detectors, fire extinguishers, and deadbolt locks. These features reduce the risk of damage and theft, lowering your premiums.

What should I look for in a homeowners insurance policy in Georgia?

In Georgia, it's important to prioritize protection against hurricanes, tornadoes, and flooding. You should also ensure that your policy provides adequate coverage for personal property, liability, and additional living expenses in case of disaster.

Is renters insurance necessary in Georgia if I have homeowners insurance?

Renters insurance is not required if you own a home, but it is highly recommended for renters in Georgia. It covers personal property and liability in case of fire, theft, or natural disasters, which are not typically covered by your landlord's insurance.

Explore our guide that tackle about smart home devices: save money on homeowners insurance & prevent claims.

How do different home insurance policies in Georgia handle replacement cost versus market value?

Replacement cost covers the expense to rebuild or repair your home based on current construction costs, not the market value. It's generally more expensive but ensures that you're adequately covered for rebuilding after a total loss. Check out our guide that answers the question, What is recoverable depreciation?.

What are the advantages of bundling home and auto insurance in Georgia?

Bundling home and auto insurance in Georgia can provide significant savings. Many insurers offer multi-policy discounts, which can lower both your homeowners and auto premiums, while simplifying your billing and policy management. Make sure your home is protected by entering your ZIP code into our home insurance comparison tool below today.